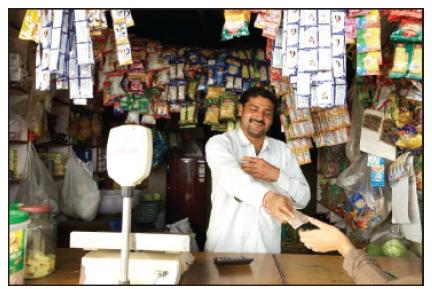

Historically, the structure of retailing in India was very fragmented, with a large number of very small

Question:

In practice, small-store owners in India have a long history of using their political power to lobby the government to impose restrictions on direct investment by foreigners in the retail space. Like incumbents everywhere, their goal has been to limit competition and protect their businesses and jobs. Until 2011, foreign multi-brand retailers such as Costco, Tesco, and Walmart were forbidden from owning retail outlets in the country. Even single-brand retailers such as IKEA and Nike had to partner with a local retailer, were limited to a 51 percent ownership stake, and had to go through a lengthy bureaucratic approval process.

By 2011, the Indian federal government had come to the conclusion that foreign investment in retailing was needed to improve India’s supply chain, increase consumer choice, and help farmers bring their products to market. This view was supported by much of Indian industry, which saw the modernization of the retailing sector as an important condition for continued economic development. Clearly, the government believed that greater foreign capital and technology would help India grow its economy. In late 2011, the Indian government announced a plan to reform foreign direct investment regulations. The plan was to allow foreign multi-brand retailers such as Walmart and Tesco to open retail stores, although they would be limited to a 51 percent ownership stake. At the same time, the government stated its intention to allow single-brand retailers to set up wholly owned stores, although anything over a 49 percent foreign ownership stake would still require formal government approval. These plans were greeted with strong opposition from small retailers and rival political parties, and the government was forced to temporarily shelve them.

In early 2012, the Indian government managed to secure approval for plans to allow foreign single-brand retailers to open wholly owned stores, but imposed the requirement that a single-brand retailer had to source 30 percent of its inventory from India. One of the first retailers to respond to these changes was IKEA, which announced it would invest $1.9 billion and set up 25 stores in the country. More generally though, many analysts viewed the 30 percent sourcing requirement as a major impediment to entering India. Both Apple and Nike, for example, would have to establish significant production facilities in the country in order to meet that requirement and set up their own brand stores.

In early 2018, the government modified the 30 percent requirement, giving single-brand retailers five years after their initial entry to reach the 30 percent figure. The government also allowed single-brand retailers to establish wholly owned subsidiaries without having to go through the cumbersome government approval process.

In late 2012, the federal Indian government allowed foreign investors to open multi-brand retail stores in India, but limited ownership to 51 percent. Moreover, in a nod to the strength of the political opposition, the federal government made this requirement subject to approval by individual states within the country, allowing some to opt out. Several states have done so, which reduces the attractiveness of India as a market for foreign retailers.

At the same time, India has allowed 100 percent ownership of online retail marketplaces in India. Amazon took advantage of this to enter the country in 2014 and has committed to invest $5 billion in India. Unlike in the United States, however, Amazon does not sell goods it has taken ownership of because that would classify the company as a multi-brand retailer, limit its ownership stake in Indian operation to 51 percent, and require it to take an Indian partner.

Instead, Amazon only sells goods offered through its marketplace platform by third parties. However, Amazon is investing heavily in fulfillment centers and logistics infrastructure to enable it to deliver goods efficiently to Indian customers. Its investment may help to boost the efficiency of supply chains in the country.

Questions

1. What explains the fragmented nature of India’s retail sector? What are the benefits of this system? What are the costs?

2. How might investment by foreign retailers change retailing in India? What are the potential benefits of such FDI?

3. Who stands to lose from FDI into India’s retail sector? Who stands to gain?

4. Why has India been so slow to change its laws regarding foreign ownership of retailers? What, if anything, can foreign retailers do to influence the laws in a way that benefits entry?

5. Given the political and economic realities in India, what is the best entry strategy for a foreign retailer?

Step by Step Answer:

1 Explanation of Fragmentation Historical Context Indias retail sector historically had numerous small independent stores a structure that persisted due to traditional business practices Supply Chain ...View the full answer

ISE International Business Competing In The Global Marketplace

ISBN: 9781260575866

13th International Edition

Authors: Charles Hill