We consider the discrete-time Cox-Ross-Rubinstein model with (N+1) time instants (t=0,1, ldots, N), with a riskless asset

Question:

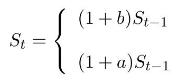

We consider the discrete-time Cox-Ross-Rubinstein model with \(N+1\) time instants \(t=0,1, \ldots, N\), with a riskless asset whose price \(A_{t}\) evolves as \(A_{t}=A_{0}(1+r)^{t}\), \(t=0,1, \ldots, N\). The evolution of \(S_{t-1}\) to \(S_{t}\) is given by

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a The possible values of Re are a and b b We have E Rt1 Ft ...View the full answer

Answered By

Milan Mondal

I am milan mondal have done my Msc in physics (special astrophysics and relativity) from the University of burdwan and Bed in physical science from the same University.

From 2018 I am working as pgt physics teacher in kendriya vidyalaya no2 kharagpur ,west bengal. And also I am doing advanced physics expert in chegg.com .also I teach Bsc physics .

I love to teach physics and acience.

If you give me a chance I will give my best to you.

4+ Reviews

10+ Question Solved

Related Book For

Introduction To Stochastic Finance With Market Examples

ISBN: 9781032288277

2nd Edition

Authors: Nicolas Privault

Question Posted: