Llewellyn Limited paid 68,000 for its interest in Roberts Limited on 1 July 2017, The following is

Question:

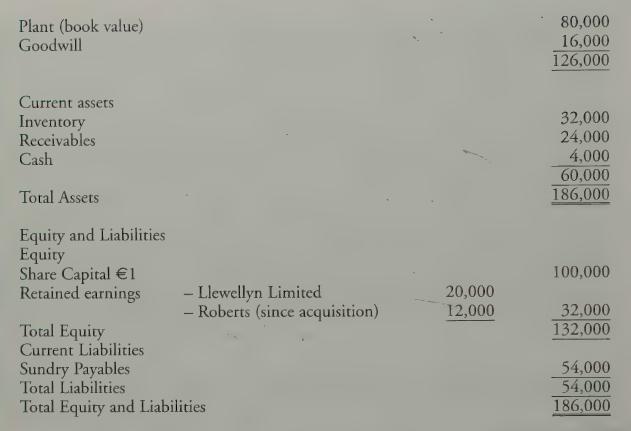

Llewellyn Limited paid €68,000 for its interest in Roberts Limited on 1 July 2017, The following is the draft consolidated statement of financial position of Llewellyn Limited and its subsidiary Roberts Limited at 30 June 2018.

Additional Information:

1. Llewellyn Limited acquired only 80% of the ordinary share capital of Roberts Limited, whereas it was assumed by the Assistant Accountant who drew up the draft consolidated statement of financial position that the whole of it had been acquired.

2. Inventory shown in the statement of financial position of Roberts Limited was undervalued by €1,000 at 30 June 2017 and by €1,600 at 30 June 2018.

3. Plant shown in the statement of financial position of Roberts Limited at 30 June 2017 was overvalued by €2,000 (rate of depreciation — 10% per annum).

4. Inventory held by Roberts Limited at 30 June 2018 includes €800 transferred from -

Llewellyn Limited which cost the latter €600.

5. Roberts Limited has no preference capital, no reserves other than retained earnings and had paid no dividends since the acquisition of the shares by Llewellyn Limited.

6. With respect to the measurement of non-controlling interests at the date of acquisition, the proportionate share method equates to the fair value method. The directors of Llewellyn Limited are confident that any goodwill arising on the acquisition of Roberts Limited has not suffered any impairment.

Requirement

(a) Present working papers in the form of ledger accounts showing the adjustments necessary to correct the Consolidated Statement of Financial Position.

(b) Present the revised Consolidated Statement of Financial Position as at 30 June 2018.

Step by Step Answer:

International Financial Accounting And Reporting

ISBN: 9781912350025

6th Edition

Authors: Ciaran Connolly