All Things Greek Inc. has three sales divisions. One of the key evaluation inputs for each division

Question:

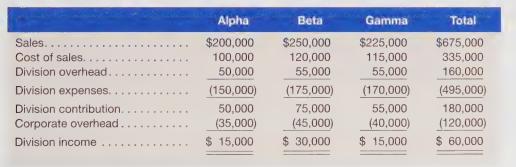

All Things Greek Inc. has three sales divisions. One of the key evaluation inputs for each division manager is the performance of his or her division based on division income. The division statements for August are as follows:

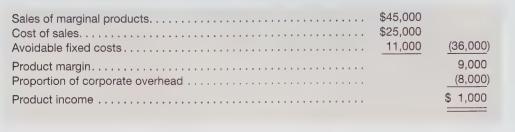

The Gamma manager is unhappy that his profitability is the same as that of the Alpha Division and one-half that of the Beta Division when his sales are halfway between these two divisions. The manager knows that his division must carry more product lines because of customer demands, and many of these additional product lines are not very profitable. He has not dropped these marginal product lines because of idle capacity; all of the products cover their own variable costs. After analyzing the product lines with the lowest profit margins, the divisional controller for Gamma provided the following to the manager:

Although these products were 20 percent of Gamma’s total sales, they contributed only about 7 percent of the division’s profits. The controller also noted that the corporate overhead allocation was based on a formula of sales and divisional contribution margin.

Required

a. Prepare a set of segment statements for August assuming that all facts remain the same except that Gamma’s weak product lines are dropped and corporate overhead is allocated as follows: Alpha, $40,000; Beta, $47,500; and Gamma, \($32,500\). Does the Gamma Division appear better after this action? What will be the responses of the other two division managers?

b. Suggest improvements for All Things Greek’s reporting process that will better reflect the actual operations of the divisions. Keep in mind the utilization of the reporting process to assist in the evaluation of the managers. What other changes could be made to improve the manager evaluation process?

Step by Step Answer: