Assessing the Impact of an Incentive Plan? (LO1, 2, 3) Overview Ladbrecks is a major department store

Question:

Assessing the Impact of an Incentive Plan’? (LO1, 2, 3)

Overview Ladbrecks is a major department store with fifty retail outlets. The company’s stores compete with outlets run by companies such as Nordstrom, Macys, Marshall Fields, Bloomingdales and Saks Fifth Avenue. During the early nineties the company decided that providing excellent customer service was the key ingredient for success in the retail industry. Therefore, during the mid 1990s the company implemented an incentive plan for its sales associates in twenty of its stores. Your job is to assess the financial impact of the plan and to provide a recommendation to management to continue or discontinue the plan based on your findings.

Incentives in Retail The past decade has evidenced a concerted effort by many firms to empower and motivate employees to improve performance. A recent New York Times article reported that more and more firms are offering bonus plans to hourly workers. An Ernst and Young survey of the retail industry indicates that virtually all department stores currently offer incentive programs such as straight commissions, base salary plus commission, and quota bonus programs. Although these programs can add to payroll costs, the survey respondents indicated that they believe these plans have contributed to major improvements in customer service.

Company’s Background Ladbrecks was founded by members of the Ladbreck family in the 1880s. The first store opened under the name Ladbreck Dry Goods. Growth was fueled through acquisitions as the industry consolidated during the 1960s. Over this hundred-year period, sales associates were paid a fixed hourly wage. Raises were based on seniority. Sales associates were expected to be neat and courteous to customers. The advent of specialty stores and the stated intention of an upscale west coast retailer to begin opening stores in the Midwest concerned Ladbreck’s management. Building on its history of excellence in customer service, the company initiated its performance-based incentive plan to support its stated firm-wide strategy of

“customer emphasis” with “employee empowerment.” Management expected it to result in further enhancement of customer service and, consequently, in an increase in sales generated at its stores.

Incentive Plan The plan was implemented in stores sequentially as company managers intended to examine and evaluate the plan’s impact on sales and profitability. Initially, the firm selected one store from a group of similar stores in the same general area to begin the implementation. By the end of 1994, ten stores had implemented the plan. In 1995, ten more stores implemented the plan, bringing the total to 20 out of a total of 50.

The performance-based incentive plan is best described as a bonus program. At the time of the plan’s implementation, sales associates received little in the form of annual merit increases, and promotions were rare. The bonus payment became the only significant reward for high performance.

Each week sales associates are paid a base hourly rate times hours worked. In addition, under the plan sales associates could increase their compensation by receiving a bonus at the end of each quarter. The contract provides sales-force personnel with a cash bonus only if the actual quarterly sales generated by the employee exceed a quarterly sales goal. Individualized pre-specified sales goals were established for each employee based only on the individual’s base hourly rate, hours worked and a multiplier

(multiplier = 1/bonus rate). The bonus is computed as a fixed percentage of the excess sales (actual sales minus a pre-specified sales goal) by the employee in a quarter (see exhibit one).

@ (Employee’s actual sales for quarter —

Employee’s Bonus = 08 a employee’s targeted sales for quarter)

Where employee’s Employee’s

= : x y c i targeted sales for quarter hourly wage ee beam ee LES Senior managers regarded the incentive plan as a major change for the firm and its sales force.

Management expected that the new incentive scheme would motivate many changes in employee behavior that would enhance customer service. Sales associates were now expected to build a client base to generate repeat sales. Actions consistent with this approach include developing and updating customer address lists (including details of their needs and preferences), writing thank you notes and contacting customers about upcoming sales and new merchandise that matched their preferences.

9 Wriitttteen to Hi lluscttrraattea theP e 1u)s¢ep of - rveallaeyvsa nt cAoQsNcttse aanndd rr evenues feonr decisbiieo n makin

Chapter 4 | Relevant Costs and Benefits for Consultant’s Task Management decided to call you in to provide an independent assessment. While the company thought that sales had increased with the plan’s implementation, the human resource department did not know exactly how to quantify the plan’s impact on sales and expenses. It suspected that employee salaries, cost of goods sold, and inventory carrying costs, as well as sales, may have changed due to the plan’s implementation. You, therefore, requested information on these financial variables.

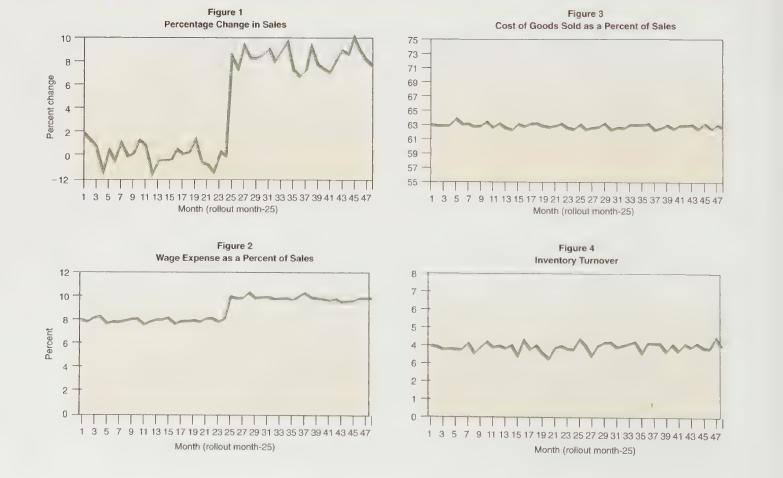

Sales Analysis: Because each of the twenty stores implemented the plan at different dates, and store sales fluctuated greatly with the seasons and the economy, you could not simply plot store sales.

Instead, for each of the twenty stores, you picked another Ladbreck store as a control and computed for 48 months the following series of monthly sales!”:

[(Plan Store Sales in Month t + Plan Store Sales in Month t-24) —

Percent Change in Sales = q ;

(Control Store Sales in Month t/ Control Store Sales in Month t-24)] * 100 The plan’s implementation was denoted as month 25, so you had 24 months prior to the plan and 24 months after the plan. Averages were then taken for the twenty stores. If the control procedure worked then you expected that the first 24 months of the series would fluctuate around zero. The actual results are reported in Figure | below. Month 25 is denoted as the rollout month, the month the incentive plan began.

Expense Analysis: You then plotted wage expense/sales, cost of goods sold/sales, and inventory turnover for the twenty stores for the 24 months preceding the plan and the first 24 months after plan implementation.

After pulling out seasonal effects these monthly series are presented in figures 2, 3 and 4. If the plan has no impact on these expenses then you would expect no dramatic change in the series around month 25.

Figure 2 plots (wage expense in month t/sales in month t)

Figure 3 plots (cost of goods sold in month t/sales in month t)

Figure 4 plots “annual” turnover computed as (12 x cost of goods sold in month t/inventory at beginning of month t)

For example, if monthly cost of sales is $100 and the annual inventory turnover ratio is 4, it suggests a monthly turnover of 0.333 with the firm holding an average inventory of $300 throughout the year. (Note that a monthly inventory turnover of .333 implies an annual turnover of 4 (from 12 x 0.333).

Financial Report for Store: A typical annual income statement for a pre-plan Ladbreck store before fixed charges, taxes and incidentals looks as follows.

Total Percent SUES once 0-8 ocnerith eee Bie eR Oe ae 10,000,000 100 GOSO MOGOOUSIS OIG ee ao een sees wr 6.8 Sacethale snare home 6,300,000 63 GOSS BIGHT ws as ora a oe 8 eRe enn eee erry 3,700,000 37 EMmploveccsalanicStarn rth oe eae acl. seedy neem oes 800,000 mee.

RrOmuberonenixed ChargeSe. + sec c sa once oo thames ae 2,900,000 29 A store also has substantial charges for rent, management salaries, insurance, etc. but they are fixed with respect to the incentive plan.

Required:

a. Suppose the goal of the firm is to now provide superior customer service by having the sales consultant identify and sell to the specific needs of the customer. What does this goal suggest about a change in managerial accounting and control systems?

Provide an estimate of the impact of the incentive plan on sales.

Did the sales impact occur all at once, or did it occur gradually?

What is the impact of the incentive plan on wage expense as a percent of sales?

What is the impact of the incentive plan on cost of good sold as a percent of sales?

What is the impact of incentive plan on inventory turnover (turnover = cost of goods sold +

inventory)? [If sales go up then stores are selling more goods; therefore, more goods need to be on the floor or those goods on floor need to turn over faster].

g. What is the additional dollar amount of inventory that must be held?

s SSeSeo

\0 For instance, assume sales for plan store were $2,200 this January and $2,000 two Januarys ago. Also assume that sales in the control store were $4,400 this January and $4,000 two Januarys ago. Percent change = 2,200/2,000 — 4,400/4,000 = 0.

Decision Making 129 130 Chapter 4 | Relevant Casts and Benefits for Decision Making h. Using the information on sales and expenses for a typical store, provide an analysis of the additional store profit contributed by the plan. Assume that it costs 12% a year to carry the added inventory.

i. Look at Exhibit One which provides a partial listing of employee pay for one small department within a store. Which “type” of employee is receiving the bonus.

j. Should the company keep the plan? Explain your estimate of the financial impact of the plan and also incorporate any nonfinancial information you feel is relevant in justifying your decision.

Wages by subset of employees in Ladbreck’s fashion department.

Hours Actual Years. Hourly Worked Sales Total of Wage in Regular for Pay Name Service Rate Quarter Pay Quarter Bonus Quarter BOBIMARINEYaietite cs sass once 2 4.00 400 1,600 25,000 400 2,000 SIMMBENDRIXKSSae eciace eee ae 16 7.50 440 3,300 41,000 0 3,300 MIEEIEDSMALUB FRG Mel isred cats 6 24 9.99 440 4,396 40,000 0 4,396 AIS GRE EIN Geeetye yeauni tn das 11 6.00 400 2,400 36,000 480 2,880 BOBIDYWANER iet sticatc.cy eettense c,os e 4 5.00 400 2,000 30,000 400 2,400 WARTS UORIUIN) oats eee pos Bde ean 10 6.00 400 2,400 30,000 0 2,400 WHESONNIGIMENE $2 5-50 0neuo0n 16 7.50 440 3,300 50,000 700 4,000 BRUCE SERINGSTIEEN Meas: 23 9.99 440 4,396 30,000 0 4,396 MICHIGAN & SMILEY........... ie} 7.00 400 2,800 38,000 240 3,040 RIC RIEU UIRIANA. Scheceoalls asore n 22 9.90 400 3,960 30,000 0 3,960 UO mINEENINIOIN Gogabaec coeoets 3 5.00 400 2,000 34,000 720 2,720 w WIE] OLGRESIAS setae er ss: 4 5.00 480 2,400 46,000 1,280 3,680 TRO MAM NCIPIEN PING tesiOocce cieere acrsore s 11 6.00 400 2,400 36,000 480 2,880 J@ANIBAEZA irs fevcresiesyet ea s 21 9.90 400 3,960 40,000 0 3,960 BEEING MereterinGaitas sor:at e 8 6.00 400 2,400 38,000 640 3,040 GEADISIKNIGHI eeeee a e 14 8.00 480 3,840 46,000 0 3,840 NENEVOUNGHRtaist poenes o e 15 8.00 480 3,840 36,000 0 3,840 B@IDIDDEEN Sree eee crs oe 4 5.00 400 2,000 30,000 400 2,400

Step by Step Answer:

This question has not been answered yet.

You can Ask your question!