Marfrank Corporation is a manufac turing company with six functional departments-Finance, Marketing, Personnel, Production, Research and Development

Question:

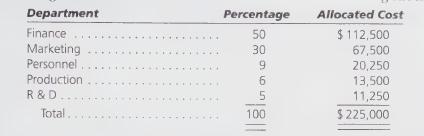

Marfrank Corporation is a manufac turing company with six functional departments-Finance, Marketing, Personnel, Production, Research and Development (R&D), and Information Systems-each administered by a vice-president. The Information Systems Department (ISD) was established in 1996 when Marfrank decided to acquire a new mainframe computer and develop a new information system. While systems development and implementation is an ongoing process at Marfrank, many of the basic systems needed by each of the functional departments were operational at the end of 1997. Thus, calendar year 1998 is considered the first year for which the ISD costs can be estimated with accuracy. Marfrank's presi dent wants the other five functional departments to be aware of the magnitude of the ISD costs by reflecting the allocation of ISD costs in the reports and statements prepared at the end of the first quarter of 1998. The allocation of ISD costs to each of the departments was based on their actual use of ISD services. Jon Werner, vice-president of ISD, suggested that the actual costs of ISD be allocated on the basis of the number of pages of actual computer output. This basis was suggested because the departments use reports in evaluating their operations and in making decisions. The use of this basis resulted in the following allocations:

After the quarterly reports were distributed, the Finance and Marketing De- partments objected to this allocation method. Both departments recognized that they were responsible for most of the output in terms of reports, but they believed that these output costs might be the smallest of ISD costs and requested that a more equitable allocation basis be developed.

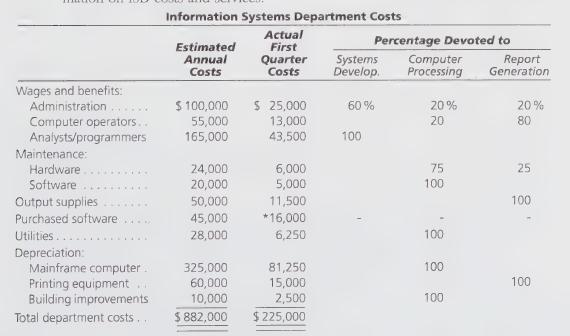

After meeting with Werner, Elaine Jergens, Marfrank's controller, concluded that ISD provided three distinct services-systems development, computer pro- cessing represented by central processing unit (CPU) time, and report generation. She recommended that a predetermined rate be developed for each of these services from budgeted annual activity and costs. The ISD costs would then be assigned to the other functional departments using the predetermined rate times the actual activity used. Any difference between actual costs incurred and costs allocated to the other departments would be absorbed by ISD.

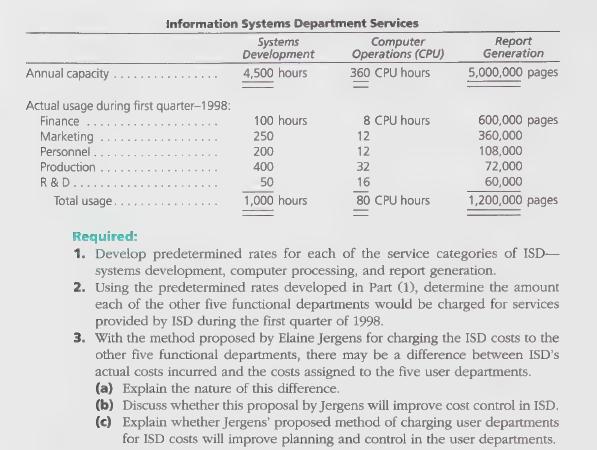

Jergens and Werner concluded that systems development costs could be charged on the basis of hours devoted to systems development and programming, that computer processing charges be based on CPU time used for operations (exclusive of database development and maintenance), and that report generation charges be based on pages of output. The only cost that should not be included in any of the predetermined rates would be purchased software; these packages were usually acquired for a specific department's use. Thus, Jergens concluded that purchased software would be charged at cost to the department for which it was purchased. In order to revise the first quarter allocation, Jergens gathered the following infor- mation on ISD costs and services:

Step by Step Answer:

Managerial Accounting

ISBN: 9780538842822

9th Edition

Authors: Harold M. Sollenberger, Arnold Schneider, Lane K. Anderson