Use an (F)-test to jointly test the relevance of the two variables (X T R A _X

Question:

Use an \(F\)-test to jointly test the relevance of the two variables \(X T R A \_X 5\) and \(X T R A \_X 6\) for the family income equation in Example 6.12 and Table 6.1.

Data From Example 6.12:-

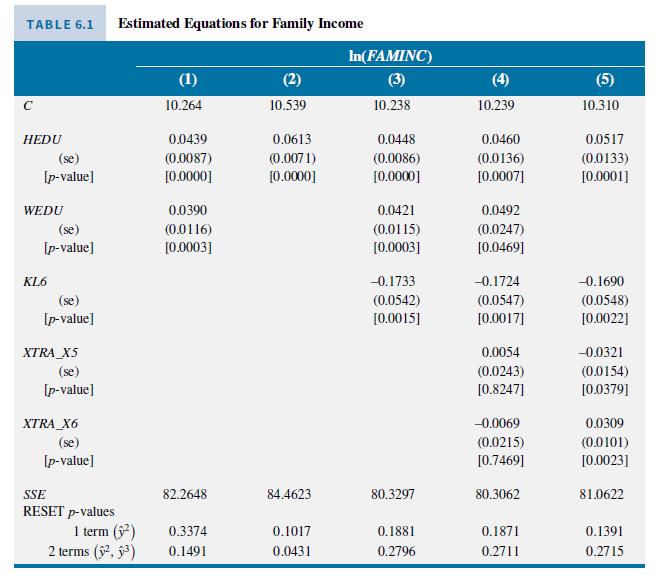

To see the effect of irrelevant variables, we add two artificially generated variables XTRA_X5 and XTRA_X6 to the family income equation. These variables were constructed so that they are correlated with HEDU and WEDU but have no influence on family income. The results from including these two variables are given in column (4) of Table 6.1. What can we observe from these estimates? First, as expected, the coefficients of XTRA_X5 and XTRA_X6 have p-values greater than 0.05. They do indeed appear to be irrelevant variables. Also, the standard errors of the coefficients estimated for all other variables have increased, with p-values increasing correspondingly. The inclusion of irrelevant variables that are correlated with the other variables in the equation has reduced the precision of the estimated coefficients of the other variables. This result follows because, by the Gauss–Markov theorem, the least squares estimator of the correct model is the minimum variance linear unbiased estimator.

Finally, let us check what happens if we retain XTRA_X5 and XTRA_X6, but omit WEDU, leading to the results in column (5). The coefficients for XTRA_X5 and XTRA_X6 have become significantly different from zero at a 5% level of significance. The irrelevant variables have picked up the effect of the relevant omitted variable. While this may not matter if prediction is the main objective of the exercise, it can lead to very erroneous conclusions if we are trying to identify the causal effects of the included variables.

Data From Table 6.1:-

Step by Step Answer:

Principles Of Econometrics

ISBN: 9781118452271

5th Edition

Authors: R Carter Hill, William E Griffiths, Guay C Lim