On 31 December 19X6 Breeze Ltd acquired all the assets, except the investments, of Blow Ltd. The

Question:

On 31 December 19X6 Breeze Ltd acquired all the assets, except the investments, of Blow Ltd.

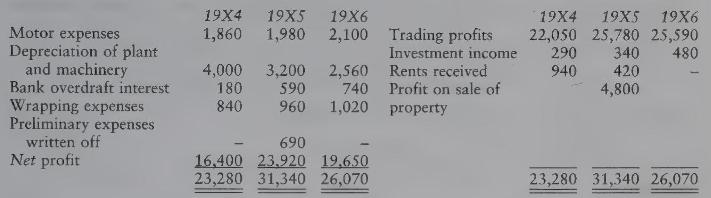

The following are the summaries of the profit and loss account of Blow Ltd for the years 19X4, \(19 \times 5\) and \(19 \times 6\) :

The purchase price is to be the amount on which an estimated maintainable profit would represent a return of 25 per cent per annum.

The maintainable profit is to be taken as the average of the profits of the three years 19X4, 19X5 and \(19 \times 6\), after making any necessary adjustments.

You are given the following information:

(a) The cost of the plant and machinery was \(£ 20,000\). It is agreed that depreciation should have been written off at the rate of \(12 \frac{1}{2}\) per cent per annum using the straight line method.

(b) A form of new plastic wrapping material introduced on to the market means that wrapping expenses will be halved in future.

(c) By a form of long-term rental of motor vehicles, it is estimated that motor expenses will be cut by one-third in future.

(d) Stock treated as valueless at 31 December \(19 \mathrm{X} 3\) was sold for \(£ 1,900\) in \(19 \mathrm{X} 5\).

(e) The working capital of the new company is such that an overdraft is not contemplated.

(f) Management remuneration has been inadequate and will have to be increased by \(£ 1,500\) a year in future.

You are required to set out your calculation of the purchase price. All workings must be shown. In fact, your managing director, who is not an accountant, should be able to decipher how the price was calculated.

Step by Step Answer: