Advan ced : Planning and operat ing variances The management team of Thorpe Ltd feel that standard

Question:

Advan ced : Planning and operat ing variances The management team of Thorpe Ltd feel that standard costing and variance analysis have little to offer 1n the reporting of some of the activities of their firm.

'Although we produce a range of fairly standardized products'

states the accountant of Thorpe Ltd, 'prices of many of our raw materials are apt to change suddenly and comparison of actual prices with a predetermined. and often unrealistic, standard price is of little use. For some of our products we can utilize one of several equally suitable raw materials and we always plan to utilize the raw material which will, in our opinion, lead to the cheapest total production costs. However, we are frequently caught out by price changes and the material actually used often proves, after the event, to have been more expensive than the alternative which was orginally rejected.

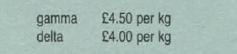

'For example, consider the experience over the last accounting period of two of our products, alpha and beta. To produce a unit of alpha we can use either 5 kg of gamma or 5 kg of delta. We planned to use gamma as it appeared it would be the cheaper of the two and our plans were based on a cost of gamma of £3 per kg. Due to market movements the actual prices changed and if we had purchased efficiently the costs would have been

'Production of alpha was 2000 units and usage of gamma amounted to 10800kg at a total cost of £51840.

'Product beta uses only one raw material, epsilon, but again the price of this can change rapidly . lt was thought that epsilon would cost £30 per tonne but in fact we only paid £25 per tonne and if we had purchased correctly the cost would have been less as it was freely available at only £23 per tonne. It usually takes 1.5 tonnes of epsilon to produce 1 tonne of beta but our production of 500 tonnes of beta used only 700 tonnes of epsilon.

'So you can see that with our particular circumstances the traditional approach to variance analysis is of little use and we don't use it for materials although we do use it for reporting on labour and variable overhead costs.'

Required:

(a) Analyse the material variances for both alpha and beta utiliz1ng:

(i) traditional variance analysis; and (ii) an approach which distinguishes between planning and operational variances.

(c. 12 marks)

(b) Write brief notes which (i) explain the approach to variance analysis which distinguishes between planmng and operational variances, and (ii) Indicate the extent to which th1s approach is useful for firms in general and for Thorpe Ltd in particular: and (fii) highlight the main difficulty in the application of this approach.

Step by Step Answer: