Advanced: Impact of various transactions on ROCE and a discussion whether ROCE leads to goal congruence G

Question:

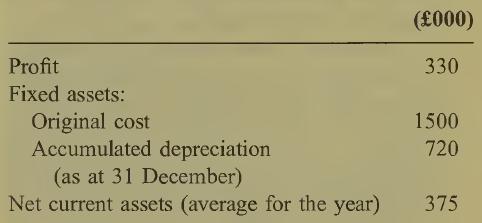

Advanced: Impact of various transactions on ROCE and a discussion whether ROCE leads to goal congruence G Limited, one of the subsidiaries of GAP Group p.l.c., produces the following condensed data in respect of its budgeted performance for the year to 31 December:

In addition, it is considering carrying out the following separate non-routine transactions:

A. It would offer its customers cash discounts that would cost £8000 per annum.

This would reduce the level of its debtors by an average of £30 000 over the year. This sum would be used to increase the dividend to GAP Group p.l.c. payable at the end of the year.

B. It would increase its average stocks by £40000 throughout the year and reduce by that amount the dividend payable to GAP Group p.l.c. at the end of the year.

This is expected to yield an increased contribution of £15 000 per annum resulting from larger sales.

C. At the start of the year it would sell for £35 000 a fixed asset that originally cost £300000 and which has been depreciated by 4/5ths of its expected life.

If not sold, this asset would be expected to earn a profit contribution of £45 000 during the year.

D. At the start of the year it would buy for £180 000 plant that would achieve reductions of £52 500 per annum in revenue costs. This plant would have a life of five years, after which it would have no resale value.

The chief accountant of GAP Group p.l.c. has the task of recommending to the Group management committee whether the non-routine transactions should go ahead. The Group’s investment criterion is to earn 15% DCF and where no time period is specified, four years is the period assumed.

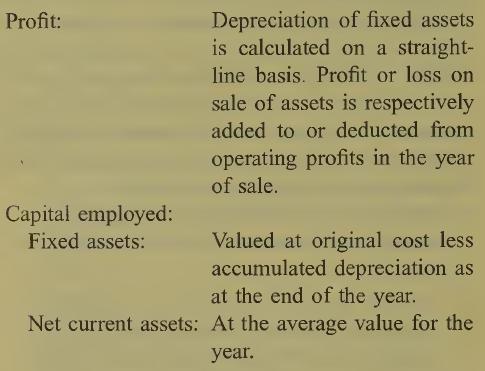

In measuring the comparative performance of its subsidiaries, GAP Group p.l.c. uses return on capital employed (ROCE) calculated on the follow¬ ing basis:

You are required

(a) as managing director of G Ltd, to recommend whether each of the four non-routine transac¬ tions (A to D) should independently go ahead;

(8 marks)

(b) as chief accountant of GAP Group p.l.c., (i) to state whether you expect there to be goal congruence between G Limited and GAP Group p.l.c. in respect of each of the four non-routine transactions consid¬ ered separately; (8 marks)

(ii) to state whether you would support a proposal to substitute a Group ROCE investment criterion in place of the exist¬ ing DCF investment criterion.

(4 marks)

Note: You should give supporting calculations and/or explanations in each part of your answer. Ignore taxation.

(Total 20 marks) CIMA Stage 4 Management Accounting—

Decision Making

Step by Step Answer: