Golf ball manufacturer Trevino is generally regarded as the industry leader. It commands a 40 percent market

Question:

Golf ball manufacturer Trevino is generally regarded as the industry leader. It commands a 40 percent market share in its targeted channels of distribution and reported net profits of $31.5 million on sales of $171 million in the last fiscal year.

A recent trend in the golf ball industry is the movement toward a 15-ball dozen (a so-called value pack). This value-oriented offering provides the consumer with 15 golf balls for the price of a standard (12-ball) dozen. Using one of its less popular, lower-quality golf ball brands, Trevino entered this market in a temporary, special promotion context. The entry was primarily in response to competitive pressures from smaller, lower-quality ball manufacturers who were flooding the market with value packs.

Initially, Trevino encountered several start-up problems relating to the unorthodox 15-ball packaging.

Since the packaging machinery had been tooled to accommodate 12-ball dozens, it could not be converted to run packaging for 15-ball dozens. These 15-ball value packs had to be packed by hand. Nonetheless, as the market developed, the value pack became a permanent product offering.

Trevino continued to offer its higher-quality, more popular brands exclusively in a 12-ball dozen configuration.

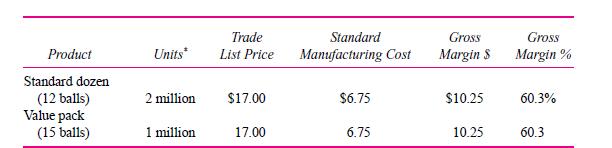

Trevino uses a standard cost system based on cost per 12-ball unit. When the value pack was introduced, it was costed at the 12-ball standard. As a result, the standard cost for the value pack includes only the costs associated with the manufacturing of 12 balls. The cost of the remaining three balls is written off to a value-pack sales promotion account when the balls are manufactured and is treated as a marketing expense for that period. Trevino calculates this written-off amount by taking the standard cost per golf ball (12-ball standard divided by 12) and multiplying it by three.

The table below, drawn from Trevino’s most recent business plan, displays how the standard cost of the value pack did not increase to account for the additional three balls.

The senior product manager, defending the use of sales incentives to increase market share in the value-pack market, commented that increasing value-pack sales was appropriate for a number of reasons, including the fact that “we’re still making a 60 percent margin on that line, as reflected in the business plan.” When asked about the value-pack standard cost, a senior financial officer commented, “Look, we’re still accounting for the cost, but just doing it somewhere else, so the bottom line isn’t affected. Since we’ve given marketing a bigger budget to account for the balls, everyone is happy.”

Trevino uses standard units as a means for allocating certain categories of overhead in a FIFO inventory system and uses standard gross margin as a component of the manufacturing group’s compensation package. Marketing is treated as a cost center and marketing costs are not traced to the product.

Required:

a. What effect is the accounting treatment of the value pack having on Trevino?

b. Why do you think the company implemented such an accounting treatment?

c. Should the accounting treatment of the value pack be changed?

Step by Step Answer:

a What effect is the accounting treatment of the value pack having on Trevino The accounting treatment that Trevino is using for the value pack has several effects on the company 1 Understated Product ...View the full answer

Accounting For Decision Making And Control

ISBN: 9780078136726

7th Edition

Authors: Jerold Zimmerman