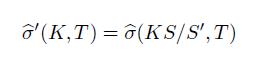

Demonstrate, that for a volatility surface b(K, T ) which is nonarbitrageable everywhere according to a proportional

Question:

Demonstrate, that for a volatility surface bσ(K, T ) which is nonarbitrageable everywhere according to a proportional dividend model, that the ‘sticky delta’ transformation:

under spot shock S = S′−S will preserve the no arbitrage conditions for arbitrary spot shock. (Hint: consider the Dupire local vol formula.)

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Diksha Bhasin

I have been taking online teaching classes from past 5 years, i.e.2013-2019 for students from classes 1st-10th. I also take online and home tuitions for classes 11th and 12th for subjects – Business Studies and Economics from past 3 years, i.e. from 2016-2019. I am eligible for tutoring Commerce graduates and post graduates. I am a responsible for staying in contact with my students and maintaining a high passing rate.

1+ Reviews

10+ Question Solved

Related Book For

The Value Of Uncertainty Dealing With Risk In The Equity Derivatives Market

ISBN: 9781848167728,9781908979582

1st Edition

Authors: George Kaye

Question Posted: