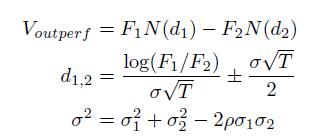

Using a change of numeraire (see Chapter 7), demonstrate that, in the case where S1 and S2

Question:

Using a change of numeraire (see Chapter 7), demonstrate that, in the case where S1 and S2 follow geometric Brownian motions with constant volatility, and zero dividends, the undiscounted risk-neutral expectation of the outperformance P = max(S1, S2) is given by:

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Michael Owens

I am a competent Software Engineer with sufficient experience in web applications development using the following programming languages:-

HTML5, CSS3, PHP, JAVASCRIPT, TYPESCRIPT AND SQL.

1+ Reviews

10+ Question Solved

Related Book For

The Value Of Uncertainty Dealing With Risk In The Equity Derivatives Market

ISBN: 9781848167728,9781908979582

1st Edition

Authors: George Kaye

Question Posted: