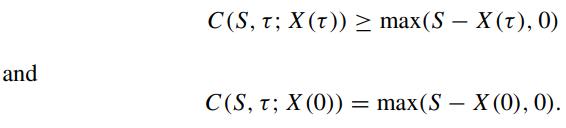

Consider an American call option with a continuously changing strike price X() where dX()/d Define the following

Question:

Consider an American call option with a continuously changing strike price X(τ) where dX(τ)/dτ

Define the following new set of variables:

Define the following new set of variables:

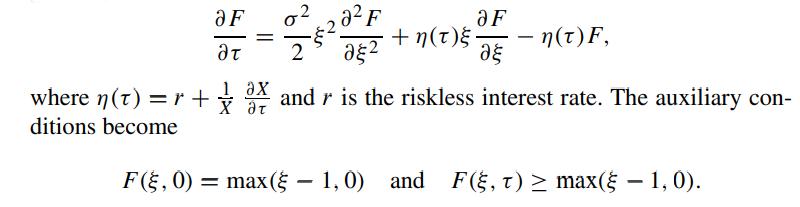

Show that the governing equation for the price of the above American call is given by

Show that if X(τ) ≥ X(0)e−rτ , then it is never optimal to exercise the American call prematurely. In such a case, show that the value of the above American call is the same as that of a European call with a fixed strike price X(0) (Merton, 1973, Chap. 1).

Show that when the time dependent function η(τ) satisfies the condition ∫τ0 η(s) ds ≥ 0, it is then never optimal to exercise the American call prematurely.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

To derive the governing equation for the price of the American call option lets start with the given ...View the full answer

Answered By

Muqadas Javed

I am a mentor by profession since seven years. I have been teaching on online forums and in universities. Teaching is my passion therefore i always try to find simple solution for complicated problems or task grasp them so that students can easily grasp them.I will provide you very detailed and self explanatory answers and that will help you to get good grade. I have two slogans: quality solution and on time delivery.

24+ Reviews

144+ Question Solved

Related Book For

Question Posted: