On January 1, 2022, Monica Company acquired 70 percent of Young Companys outstanding common stock for $665,000.

Question:

On January 1, 2022, Monica Company acquired 70 percent of Young Company’s outstanding common stock for $665,000. The fair value of the noncontrolling interest at the acquisition date was $285,000. Young reported stockholders’ equity accounts on that date as follows:

In establishing the acquisition value, Monica appraised Young’s assets and ascertained that the accounting records undervalued a building (with a 5-year remaining life) by $50,000. Any remaining excess acquisition-date fair value was allocated to a franchise agreement to be amortized over 10 years. During the subsequent years, Young sold Monica inventory at a 30 percent gross profit rate. Monica consistently resold this merchandise in the year of acquisition or in the period immediately following.

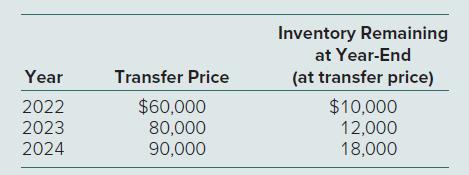

Transfers for the three years after this business combination was created amounted to the following:

In addition, Monica sold Young several pieces of fully depreciated equipment on January 1, 2023, for $36,000. The equipment had originally cost Monica $50,000. Young plans to depreciate these assets over a six-year period.

In 2024, Young earns a net income of $160,000 and declares and pays $50,000 in cash dividends. These figures increase the subsidiary’s Retained Earnings to a $740,000 balance at the end of 2024. During this same year, Monica reported dividend income of $35,000 and an investment account containing the initial value balance of $665,000. No changes in Young’s common stock accounts have occurred since Monica’s acquisition.

Prepare the 2024 consolidation worksheet entries for Monica and Young. In addition, compute the net income attributable to the noncontrolling interest for 2024.

Step by Step Answer:

Consideration transferred Noncontrolling interest fair value Subsidiary fair value at acquisitiondate Book value Fair value in excess of book value Excess fair value assignments to building to franchi...View the full answer

Advanced Accounting

ISBN: 9781264798483

15th Edition

Authors: Joe Ben Hoyle, Thomas Schaefer And Timothy Doupnik