P815 Correlation, risk, and return Matt Peters wishes to evaluate the risk and return behaviors associated with

Question:

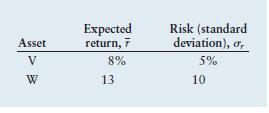

P8–15 Correlation, risk, and return Matt Peters wishes to evaluate the risk and return behaviors associated with various combinations of assets V and W under three assumed degrees of correlation: perfectly positive, uncorrelated, and perfectly negative.

The expected returns and standard deviations calculated for each of the assets are shown in the following table.

a. If the returns of assets V and W are perfectly positively correlated (correlation coefficient = +1), describe the range of (1) expected return and (2) risk associated with all possible portfolio combinations.

b. If the returns of assets V and W are uncorrelated (correlation coefficient = 0), describe the approximate range of (1) expected return and (2) risk associated with all possible portfolio combinations.

c. If the returns of assets V and W are perfectly negatively correlated (correlation coefficient = -1), describe the range of (1) expected return and (2) risk associated with all possible portfolio combinations.

Step by Step Answer:

Principles Of Managerial Finance

ISBN: 9780133546408

7th Edition

Authors: Lawrence J Gitman, Chad J Zutter