(Coupon stripping, arbitrage) You are given the following information on three traded bonds making annual coupon payments:...

Question:

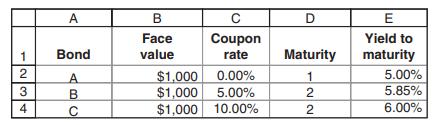

(Coupon stripping, arbitrage) You are given the following information on three traded bonds making annual coupon payments:

a. What are the prices of the above three bonds?

b. What is the zero-coupon bond yield for a 1-year bond?

c. What is the zero-coupon bond yield for a 2-year bond based on the price of bond B?

d. What is the zero-coupon bond yield for a 2-year bond based on the price of bond C?

e. Challenge question: Create an arbitrage strategy from buying and/

or selling a combination of the three bonds.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

HILLARY KIYAYI

I am a multi-skilled, reliable & talented Market analysis & Research Writer with a proven ability to produce Scholarly Papers, Reports, Research and Article Writing and much more. My ultimate quality is my English writing/verbal skill. That skill has proven to be the most valuable asset for project writing, Academic & Research writing, Proofreading, HR Management Writing, business, sales, and a variety of other opportunities.

24+ Reviews

60+ Question Solved

Related Book For

Principles Of Finance Wtih Excel

ISBN: 9780190296384

3rd Edition

Authors: Simon Benninga, Tal Mofkadi

Question Posted: