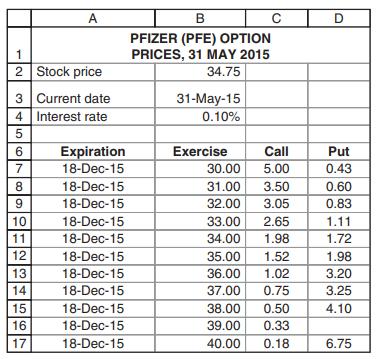

(Implied volatility) The table below gives June option prices for Pfizer (PFE) on 31 May 2015. On...

Question:

(Implied volatility) The table below gives June option prices for Pfizer (PFE)

on 31 May 2015. On this date, Pfizer’s stock price was $34.75 and the interest rate was 0.10% annually. Compute the implied volatility for all traded puts and calls using the functions CallVolatility and PutVolatility. (If no price is given, the option was not traded.)

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

PALASH JHANWAR

I am a Chartered Accountant with AIR 45 in CA - IPCC. I am a Merit Holder ( B.Com ). The following is my educational details.

PLEASE ACCESS MY RESUME FROM THE FOLLOWING LINK: https://drive.google.com/file/d/1hYR1uch-ff6MRC_cDB07K6VqY9kQ3SFL/view?usp=sharing

3+ Reviews

10+ Question Solved

Related Book For

Principles Of Finance Wtih Excel

ISBN: 9780190296384

3rd Edition

Authors: Simon Benninga, Tal Mofkadi

Question Posted: