(Portfolio statistics, efficient frontier, and minimum variance portfolio) ABC and XYZ are two stocks with the following...

Question:

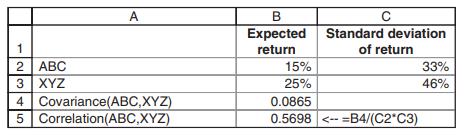

(Portfolio statistics, efficient frontier, and minimum variance portfolio) ABC and XYZ are two stocks with the following return statistics:

a. Compute the expected return and standard deviation of a portfolio composed of 25% ABC and 75% XYZ.

b. Compute the returns of all portfolios that are combinations of ABC and XYZ with the proportion of ABC being 0%, 10%, . . . , 90%, 100%. Graph these returns.

c. Compute the minimum variance portfolio.

Step by Step Answer:

This question has not been answered yet.

You can Ask your question!

Related Book For

Principles Of Finance Wtih Excel

ISBN: 9780190296384

3rd Edition

Authors: Simon Benninga, Tal Mofkadi

Question Posted: