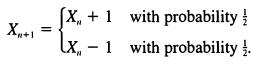

5.5. Consider a stochastic process that evolves according to the following laws: If X,, = 0, then...

Question:

5.5. Consider a stochastic process that evolves according to the following laws: If X,, = 0, then X,,+, = 0, whereas if X,, > 0, then

(a) Show that X,, is a nonnegative martingale.

(b) Suppose that X0 = i > 0. Use the maximal inequality to bound Pr{X ? N for some n ? OIXO = i}.

Note: X,, represents the fortune of a player of a fair game who wagers $1 at each bet and who is forced to quit if all money is lost (X,, = 0). This gambler's ruin problem is discussed fully in III, Section 5.3.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Sarah Khan

My core expertise are:

-_ Finance

-_ Business

-_ Management

-_ Marketing Management

-_ Financial Management

-_ Corporate Finance

-_ HRM etc...

I have 7+ years of experience as an online tutor. I have hands-on experience in handling:

-_ Academic Papers

-_ Research Paper

-_ Dissertation Paper

-_ Case study analysis

-_ Research Proposals

-_ Business Plan

-_ Complexed financial calculations in excel

-_ Home Work Assistance

-_ PPT

-_ Thesis Paper

-_ Capstone Papers

-_ Essay Writing etc...

91+ Reviews

92+ Question Solved

Related Book For

An Introduction To Stochastic Modeling

ISBN: 9780126848878

3rd Edition

Authors: Samuel Karlin, Howard M. Taylor

Question Posted: