(Portfolio selection problem) Daniel Grady is the financial advisor for a number of professional athletes. An analysis...

Question:

(Portfolio selection problem) Daniel Grady is the financial advisor for a number of professional athletes.

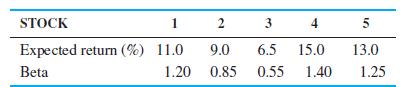

An analysis of the long-term goals for many of these athletes has resulted in a recommendation to purchase stocks with some of the income that they have set aside for investments. Five stocks have been identified as having very favorable expectations for future performance.

Although the expected return is important in these investments, the risk, as measured by the beta of the stock, is also important. (A high value of beta indicates that the stock has a relatively high risk.) The expected return and the beta for five stocks are as follows:

Daniel would like to minimize the beta of the stock portfolio (calculated using a weighted average of the amounts put into the different stocks) while maintaining an expected return of at least 11%.

Since future conditions may change, Daniel has decided that no more than 35% of the portfolio should be invested in any one stock.

(a) Formulate this as a linear program. (Hint: Define each variables as the proportion of the total investment that would be put in that stock. Include a constraint that restricts the sum of these variables to be 1.)

(b) Solve this problem. What are the expected return and beta for this portfolio?

Step by Step Answer:

Quantitative Analysis For Management

ISBN: 9781292217659

13th Global Edition

Authors: Barry Render, Ralph M. Stair, Michael Hanna, Trevor Hale