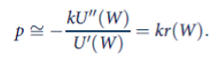

In Equation 7.30 we showed that the amount an individual is willing to pay to avoid a fair gamble (h) is given by p =

In Equation 7.30 we showed that the amount an individual is willing to pay to avoid a fair gamble (h) is given by p = 0.5E(h 2 ) r(W), where r(W) is the measure of absolute risk aversion at this person's initial level of wealth. In this problem we look at the size of this payment as a function of the size of the risk faced and this person's level of wealth.

a. Consider a fair gamble (v) of winning or losing $1, For this gamble, what is E (v 2 )?

b. Now consider varying the gamble in part (a) by multiplying each prize by a positive constant k. Let h = kv. What is the value of E (h 2 )?

c. Suppose this person has a logarithmic utility function U (W) = In W. What is a general expression for r (W)?

p=- KU" (W) U'(W) = kr(W).

Step by Step Solution

3.47 Rating (144 Votes )

There are 3 Steps involved in it

Step: 1

a A fair gamble is a specified set of prizes and asso...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Document Format ( 2 attachments)

6091e6429a47d_22645.pdf

180 KBs PDF File

6091e6429a47d_22645.docx

120 KBs Word File

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: James Stewart

7th edition

538497904, 978-0538497909