ASSIGNMENT BRIER: THE COST OF CAPITAL This is an analysis in 'retrospect'. You have the opportunity to see how the cost of capital analysis works

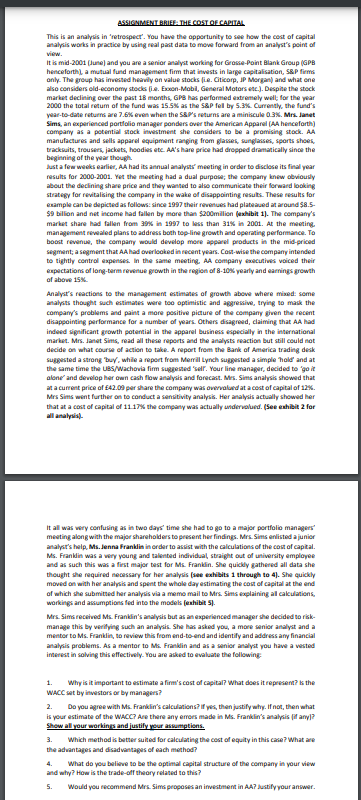

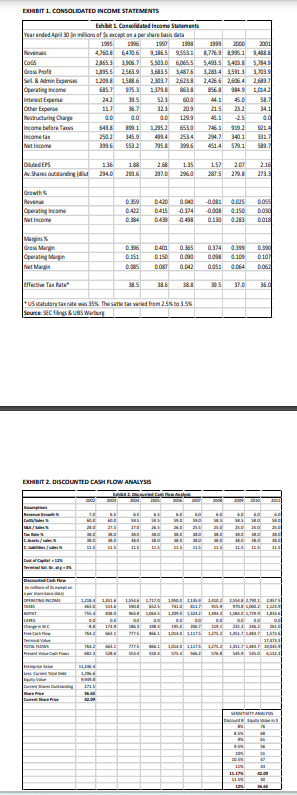

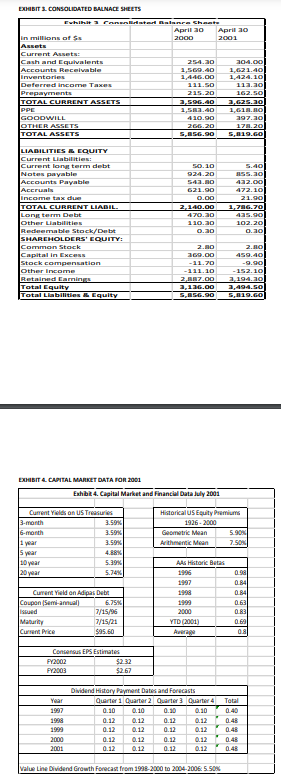

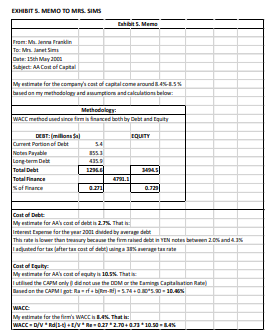

ASSIGNMENT BRIER: THE COST OF CAPITAL This is an analysis in 'retrospect'. You have the opportunity to see how the cost of capital analysis works in praction by using meal past data to move forward from an analyst's point of view. it is mid-2001 [June] and you are a senior analyst working for Grosse-Point Blank Group (GPB henceforthy, a mutual fund management firm that invests in large capitalisation, SAP firms only The group has invested heavily on value stocks (La. Citicorp, JP Morgan) and what one also considers old-economy stocks (is. Exxon Mobil, General Motors etc.]. Despite the stock market declining over the past 18 months, GPS has performed extremely well; for the pear 2000 the total relum of the fund wins 15.5% as the SAP fell by 5.3%. Currently, the fund's war-to-date returns are 7.6% even when the SP's returns are a miniscule 03%. Mrs. Janet Sims, an experienced portfolio manager ponders over the American Apparel [AA henceforth] company as a potential stock investment she considers to be a promising stock. AA manufactures and sells apparel aquipmant ranging from places, sunglasses, sports shoes, tracksuits, trousers, jackets, hoodies ate. AA's hare price had dropped dramatically since the beginning of the your though. Just a few weeks earlier, AA had its annual analysts' meeting in order to disclose its final year results for 2000-2001. Yet the mosting had a dual purpose; the company know obviousdy about the declining share price and they wanted to also communicate their forward looking strategy for revitalising the company in the wake of disappointing results. These results for example can be depicted as follows: since 1997 their revenues had plateaued at around $8.5- $9 billion and net income had fallan by more than $200million (exhibit i). The company's market share had fallen from 39% in 1997 to less than 31% in 2001. At the meeting. management revealed plans to address both top-line growth and operating performance. To boot revenue, the company would develop more apparel products in the mid-priced singmant; a segment that AA had overlooked in recent years. Cost-wise the company intended to tightly control expenses In the same meeting, AA company executives voiced their expectations of long-term revenue growth in the region of 8-10% yearly and earnings growth of above 15%. Analyst's reactions to the management estimates of growth above where mixed: some analysts thought such estimates ware too optimistic and aggressive, trying to mark the company's problems and paint a more positive picture of the company given the recent disappointing parformance for a number of years. Others disagreed, claiming that AA had indeed significant growth potential in the apparel business especially in the international market. Mrs. Jamat Sims, read all these reports and the analysts meaction but still could not decide on what course of action to take. A report from the Bank of America trading desk supported a strong "buy, while a report from Memill Lynch supported a simple hold' and at the same time the UBS/Wachovia firm supported 'sell. Your line manager, decided to 'quit along" and develop her own cash flow analysis and forecast. Mrs. Sims analysis showed that at a current price of $42.01 par share the company was overvalued at mcost of capital of 12%. Mrs Sims went further on to conduct a sensitivity analysis. Her analysis actually showed her that at a cost of capital of 11 17% the company was actually undervalued. (See exhibit 2 for all analysisl- it all was wry confusing as in two days' time she had to go to a major portfolio managers' meeting along with the major shareholders to present her findings. Mrs. Sims enlisted a junior analyst's help, Mis. Jenna Franklin in order to assist with the calculations of the cost of capital. Ms. Franklin was a worry young and talented individual, straight out of university employee and as such this was a first major bast for Me. Franklin. She quickly gathered all data she thought she required necessary for her analysis [pen exhibits i through to 4). She quickly moved on with her analysis and spent the whole day estimating the cost of capital at the and of which she submitted her analysis via a momo mail to Mrs. Sims explaining all calculations. workings and assumptions fed into the models [exhibit 5). Mrs. Simareceived Me. Franklin's analysis but as an experienced manager the decided to risk- manage this by verifying such an analysis. She has asked you, a more sanior analyst and a mentor to Ms. Franklin, to review this from end-to-and and identify and address any financial analysis problems. As a mentor to Ma Franklin and as a senior analyst you have a wasted interest in solving this effectively. You are asked to evaluate the following: 1. Why is it important to estimate a firm's cost of capital? What does it represent? is the WACC sat by investors or by managers? 2. Do you agree with Me. Franklin's calculations? if you, than justify why. If not, then what is your estimate of the WACO? Are than any emers made in Ms. Franklin's analysis (if any|7 Show all your workings and justily your assumptions. 3. Which method is better suited for calculating the cost of equity in this cine ? What are the advantages and disadvantages of each method? 4. What do you believe to be the optimal capital structure of the company in your view and why? How is the trade-off theory related to this ? 5. Would you recommend Mrs. Simi proposes an investment in AA7 Justify your answer.EXHIBIT 1. CONSOLIDATED INCOME STATEMENTS Echithe 1. Consolidated Income Sutimants 43518 64X16 1965 95681 28659 5 5030 608545 1805.5 25630 Sil & Admin Expanin 12ME 15836 856.8 4.1 Cther Egainit 16.7 EZE 1.5 1304 45.1 Income badami Took 421 3401 TEE THE 553 451.4 571 188 1 35 157 2 16 308 6 287.5 Growth 1415 0.150 Not incoma Grass Margin 6.906 0.365 Operating Margin D.151 1 150 07051 Effecton Tan kate" EXHIBIT T. DISCOUNTED CASH FLOW ANALYSE MO 31 NEXHIBIT S. CONSOLIDATED BALMACE SHEETS April 30 April 10 In millions of Ss 2000 2001 Assets Current Assets: Cash and Equivalents 354.30 704.00 Accounts Receivable 1,569.40 1,62 1.40 Inventories 1/446.00 1,424. 10 Deferred income Taxes 111.50 113.10 Prepayments 215.20 162.50 TOTAL CURRENT ASSETS 1.596.40 1,625. 10 PPC 1,501.40 GOODWILL 410.90 397.30 OTHER ASSETS 266.20 171.20 TOTAL ASSETS LIABILITIES & EQUITY Current Liabilities: Current long term debt 50.10 5.40 Notes payable 924.20 155.10 Accounts Payable 432.00 Accruals 621.90 472. 10 Income tax dun 21.80 TOTAL CURRENT LIABIL 3,140.00 Long term Debt 170.30 135.90 Other Liabilities 110.30 102.20 Redeemable Stock/ Debt 0.30 SHAREHOLDERS' EQUITY: Common Stock 2.10 Capital in Excess 160.00 458.40 Stock compensation -11.70 -8.90 Other Income -141.10 -152. 10 Retained Camings 317.00 1.194.10 Total Equity 3,136.00 1,494.50 Total Liabilities & Equity EXHIBIT &. CAPITAL MARKET DATA FOR 2001 Exhibit 4. Capital Market and Financial Data July 2001 Current Yokes on US Timemaurice Historical US Equity Premiums 3-month 3.50% 1926- 2000 6-month 3.50% Gaomatric Mean 5.90. 1 your Arithmantic Moan 7.50. 10 yaar 5.30% AAs Historic Brian 20 year 1906 Current Yield on Adipas Dab: 0.84 Coupon (Semi annual) 6.75% 0. 63 7/15/96 2000 Maturity 7/15/21 YID POOL Current Price $95.60 Concansus EPS Estimatea PY2003 52 67 Dividand History Payment Dates and Forecasts Quarter 1 Quarter 2 Quarter 3 Quarter 4 0.10 0. 10 0.10 0.10 0.40 0.12 0.12 0.13 0.12 0.48 0.13 0.12 0.12 0.12 2007 0.13 D.12 0.12 0.12 2001 0.12 0. 12 0.12 0.12 D.4E Value Line Dividend Growth Forecast from 1908-2000 to 2004-2006: 5.50%INHIBIT'S. MEMO TO MRS. SING ThatS. Moms Cute: 15th May 3001 My catimats for the company's cait of capital come around 4-15% based on my methodsbag and sumption and calculation tebow: WACC method used ning: firm is financed both by Doit and Equity OCT: millions $| EQUITY Current Portion of Debt Notan Payable Total Finance Cantod Dibe My Intimate for A'send of debth 272. That he The rate hlower than toumary became the firm mind debt in TEN notes between 20 and 4.15 I ucjented for tax jofter tan cost of debt) wings ] % muragy taxcuts Myclimate for Awood of equityh 105%. Truitinc Butlined the CAM only Ididnot in the OOM or the Doing Captaination Ribs My climate for the him's WACCh LAK Truth

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance