Answered step by step

Verified Expert Solution

Question

1 Approved Answer

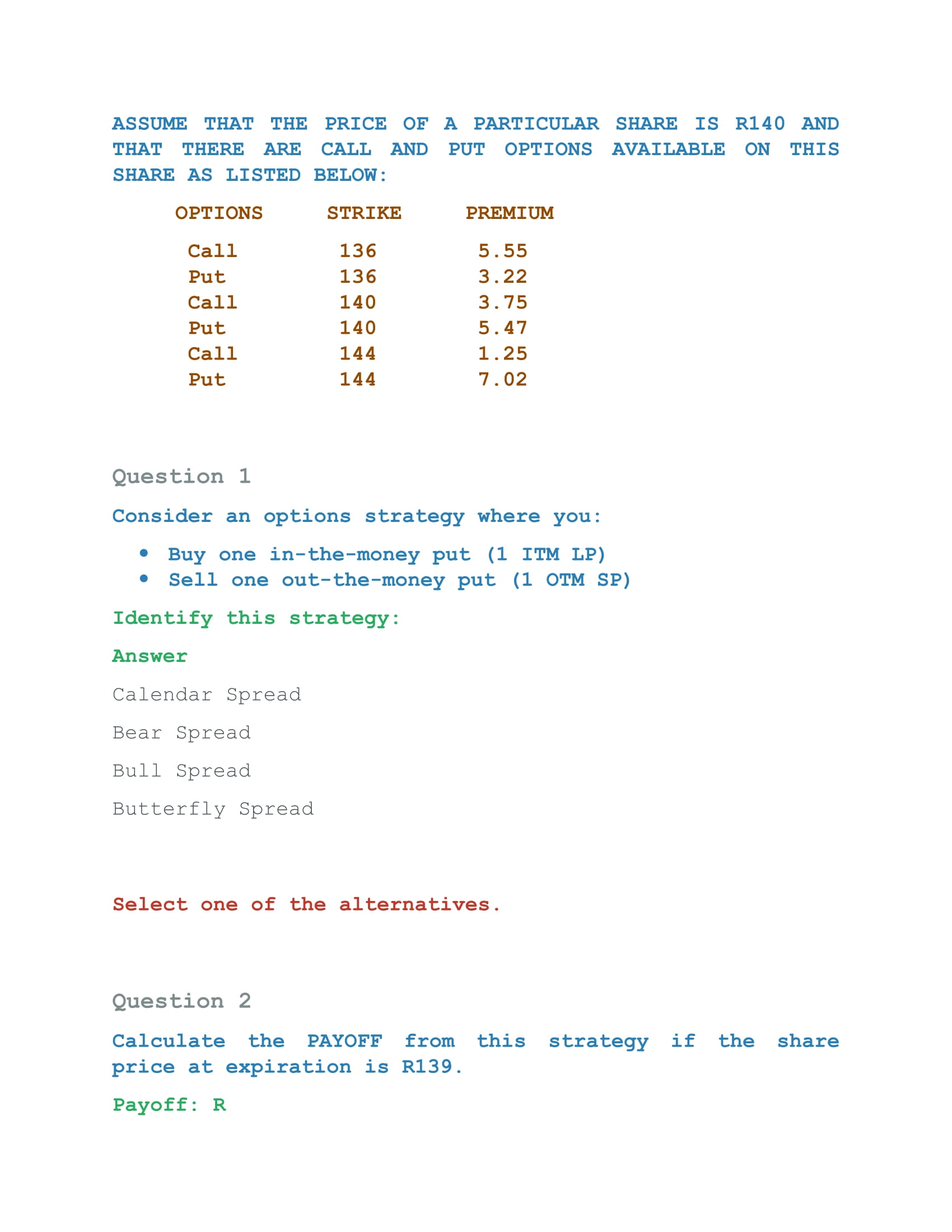

ASSUME THAT THE PRICE OF A PARTICULAR SHARE IS R140 AND THAT THERE ARE CALL AND PUT OPTIONS AVAILABLE ON THIS SHARE AS LISTED BELOW:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysis for Financial Management

Authors: Robert C. Higgins

10th edition

007803468X, 978-0078034688