Answered step by step

Verified Expert Solution

Question

1 Approved Answer

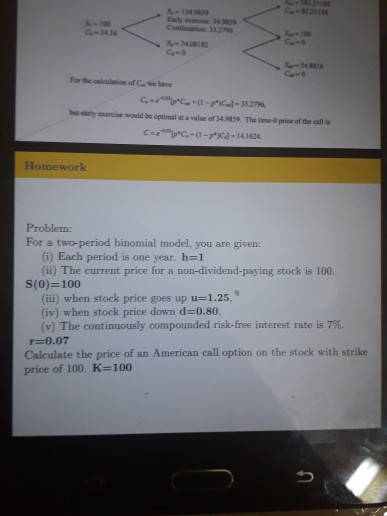

0 100 C-(--33.27% htly we would be optimal value of 3459. The timepithe alli C.C. -(1-C-141604 Homework Problem: For a two-period binomial model, you are

0

100 C-(-"-33.27% htly we would be optimal value of 3459. The timepithe alli C.C. -(1-C-141604 Homework Problem: For a two-period binomial model, you are given: (i) Each period is one year. h=1 (ii) The current price for a non-dividend-paying stock is 100. S(0)=100 (iii) when stock price goes up u=1.25, (iv) when stock price down d=0.80 (v) The continuously compounded risk-free interest rate is 7%. r=0.07 Calculate the price of an American call option on the stock with strike price of 100 K=100

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Ultra High Net Worth Bankers Handbook

Authors: Heinrich Weber, Stephan Meier

1st Edition

1905641753, 978-1905641758