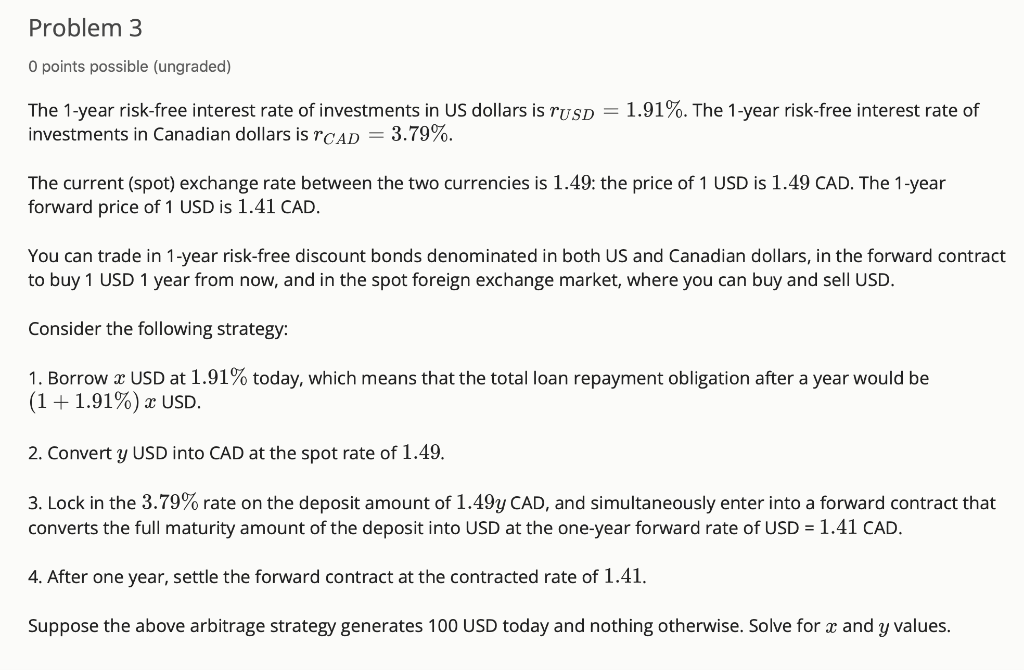

0 points possible (ungraded) The 1-year risk-free interest rate of investments in US dollars is rUSD=1.91%. The 1-year risk-free interest rate of investments in Canadian dollars is rCAD=3.79%. The current (spot) exchange rate between the two currencies is 1.49: the price of 1 USD is 1.49 CAD. The 1-year forward price of 1 USD is 1.41 CAD. You can trade in 1-year risk-free discount bonds denominated in both US and Canadian dollars, in the forward contract to buy 1 USD 1 year from now, and in the spot foreign exchange market, where you can buy and sell USD. Consider the following strategy: 1. Borrow x USD at 1.91% today, which means that the total loan repayment obligation after a year would be (1+1.91%)x USD. 2. Convert y USD into CAD at the spot rate of 1.49. 3. Lock in the 3.79% rate on the deposit amount of 1.49y CAD, and simultaneously enter into a forward contract that converts the full maturity amount of the deposit into USD at the one-year forward rate of USD =1.41 CAD. 4. After one year, settle the forward contract at the contracted rate of 1.41. Suppose the above arbitrage strategy generates 100 USD today and nothing otherwise. Solve for x and y values. (a) 0.0/2.0 points (graded) (a) x= US dollars Save You have used 0 of 2 attempts (b) 0.0/2.0 points (graded) (b) y= US dollars 0 points possible (ungraded) The 1-year risk-free interest rate of investments in US dollars is rUSD=1.91%. The 1-year risk-free interest rate of investments in Canadian dollars is rCAD=3.79%. The current (spot) exchange rate between the two currencies is 1.49: the price of 1 USD is 1.49 CAD. The 1-year forward price of 1 USD is 1.41 CAD. You can trade in 1-year risk-free discount bonds denominated in both US and Canadian dollars, in the forward contract to buy 1 USD 1 year from now, and in the spot foreign exchange market, where you can buy and sell USD. Consider the following strategy: 1. Borrow x USD at 1.91% today, which means that the total loan repayment obligation after a year would be (1+1.91%)x USD. 2. Convert y USD into CAD at the spot rate of 1.49. 3. Lock in the 3.79% rate on the deposit amount of 1.49y CAD, and simultaneously enter into a forward contract that converts the full maturity amount of the deposit into USD at the one-year forward rate of USD =1.41 CAD. 4. After one year, settle the forward contract at the contracted rate of 1.41. Suppose the above arbitrage strategy generates 100 USD today and nothing otherwise. Solve for x and y values. (a) 0.0/2.0 points (graded) (a) x= US dollars Save You have used 0 of 2 attempts (b) 0.0/2.0 points (graded) (b) y= US dollars