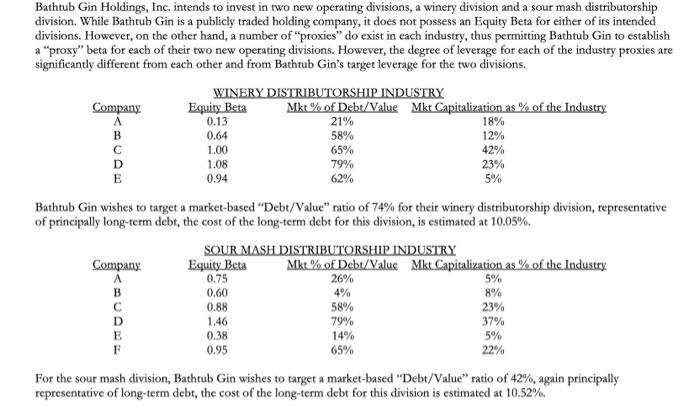

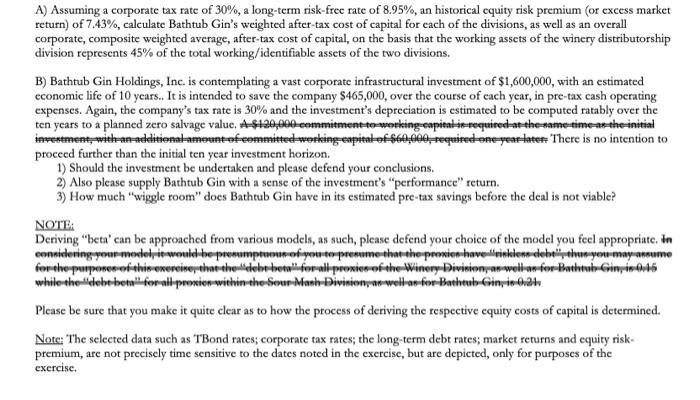

0.64 Bathtub Gin Holdings, Inc. intends to invest in two new operating divisions, a winery division and a sour mash distributorship division. While Bathtub Gin is a publicly traded holding company, it does not possess an Equity Beta for either of its intended divisions. However, on the other hand, a number of "proxies do exist in each industry, thus permitting Bathtub Gin to establish a "proxy" beta for each of their two new operating divisions. However, the degree of leverage for each of the industry proxies are significantly different from each other and from Bathtub Gin's target leverage for the two divisions. WINERY DISTRIBUTORSHIP INDUSTRY Company Equity Beta Mkt % of Debt/Value Mkt Capitalization as % of the Industry 0.13 21% 18% B 58% 12% 1.00 65% 42% D 1.08 79% 23% E 0.94 62% 5% Bathtub Gin wishes to target a market-based "Debt/Value" ratio of 74% for their winery distributorship division, representative of principally long-term debt, the cost of the long-term debt for this division, is estimated at 10.05%. SOUR MASH DISTRIBUTORSHIP INDUSTRY Company Equity Beta Mkt % of Debt/Value Mkt Capitalization as % of the Industry A 26% 5% B 0.60 4% 8% 0.88 58% 23% D 1.46 79% 37% E 0.38 14% 5% 65% 22% For the sour mash division, Bathtub Gin wishes to target a market-based "Debt/Value" ratio of 42%, again principally representative of long-term debt, the cost of the long-term debt for this division is estimated at 10.52%. 0.75 0.95 A) Assuming a corporate tax rate of 30%, a long-term risk-free rate of 8.95%, an historical equity risk premium (or excess market return) of 7.43%, calculate Bathtub Gin's weighted after-tax cost of capital for each of the divisions, as well as an overall corporate, composite weighted average, after-tax cost of capital, on the basis that the working assets of the winery distributorship division represents 45% of the total working/identifiable assets of the two divisions. B) Bathtub Gin Holdings, Inc. is contemplating a vast corporate infrastructural investment of $1,600,000, with an estimated economic life of 10 years. It is intended to save the company $465,000, over the course of each year, in pre-tax cash operating expenses. Again, the company's tax rate is 30% and the investment's depreciation is estimated to be computed ratably over the ten years to a planned zero salvage value. A$120,000.commitment to-working-capital is required-at-the-name-time as the initial investment, with an additionalamount of committed working capital of $60,000 required one year later: "There is no no intention to proceed further than the initial ten year investment horizon. 1) Should the investment be undertaken and please defend your conclusions. 2) Also please supply Bathtub Gin with a sense of the investment's "performance" return. 3) How much "wiggle room" does Bathtub Gin have in its estimated pre-tax savings before the deal is not viable? NOTE: Deriving 'beta' can be approached from various models, as such, please defend your choice of the model you feel appropriate. In considering your model te would be presumption of your te presume that the promien have trinken deh, then you may anume for the purposes of this exercise that the debt het for all proxies of the Winery Division as well as for Bathtub Grinin 046 while the debe beta'forni promien within the four Mash Divinione well as for Bathtub Gini Please be sure that you make it quite clear as to how the process of deriving the respective equity costs of capital is determined. Note: The selected data such as TBond rates; corporate tax rates; the long-term debt rates, market returns and equity risk- premium, are not precisely time sensitive to the dates noted in the exercise, but are depicted, only for purposes of the exercise. 0.64 Bathtub Gin Holdings, Inc. intends to invest in two new operating divisions, a winery division and a sour mash distributorship division. While Bathtub Gin is a publicly traded holding company, it does not possess an Equity Beta for either of its intended divisions. However, on the other hand, a number of "proxies do exist in each industry, thus permitting Bathtub Gin to establish a "proxy" beta for each of their two new operating divisions. However, the degree of leverage for each of the industry proxies are significantly different from each other and from Bathtub Gin's target leverage for the two divisions. WINERY DISTRIBUTORSHIP INDUSTRY Company Equity Beta Mkt % of Debt/Value Mkt Capitalization as % of the Industry 0.13 21% 18% B 58% 12% 1.00 65% 42% D 1.08 79% 23% E 0.94 62% 5% Bathtub Gin wishes to target a market-based "Debt/Value" ratio of 74% for their winery distributorship division, representative of principally long-term debt, the cost of the long-term debt for this division, is estimated at 10.05%. SOUR MASH DISTRIBUTORSHIP INDUSTRY Company Equity Beta Mkt % of Debt/Value Mkt Capitalization as % of the Industry A 26% 5% B 0.60 4% 8% 0.88 58% 23% D 1.46 79% 37% E 0.38 14% 5% 65% 22% For the sour mash division, Bathtub Gin wishes to target a market-based "Debt/Value" ratio of 42%, again principally representative of long-term debt, the cost of the long-term debt for this division is estimated at 10.52%. 0.75 0.95 A) Assuming a corporate tax rate of 30%, a long-term risk-free rate of 8.95%, an historical equity risk premium (or excess market return) of 7.43%, calculate Bathtub Gin's weighted after-tax cost of capital for each of the divisions, as well as an overall corporate, composite weighted average, after-tax cost of capital, on the basis that the working assets of the winery distributorship division represents 45% of the total working/identifiable assets of the two divisions. B) Bathtub Gin Holdings, Inc. is contemplating a vast corporate infrastructural investment of $1,600,000, with an estimated economic life of 10 years. It is intended to save the company $465,000, over the course of each year, in pre-tax cash operating expenses. Again, the company's tax rate is 30% and the investment's depreciation is estimated to be computed ratably over the ten years to a planned zero salvage value. A$120,000.commitment to-working-capital is required-at-the-name-time as the initial investment, with an additionalamount of committed working capital of $60,000 required one year later: "There is no no intention to proceed further than the initial ten year investment horizon. 1) Should the investment be undertaken and please defend your conclusions. 2) Also please supply Bathtub Gin with a sense of the investment's "performance" return. 3) How much "wiggle room" does Bathtub Gin have in its estimated pre-tax savings before the deal is not viable? NOTE: Deriving 'beta' can be approached from various models, as such, please defend your choice of the model you feel appropriate. In considering your model te would be presumption of your te presume that the promien have trinken deh, then you may anume for the purposes of this exercise that the debt het for all proxies of the Winery Division as well as for Bathtub Grinin 046 while the debe beta'forni promien within the four Mash Divinione well as for Bathtub Gini Please be sure that you make it quite clear as to how the process of deriving the respective equity costs of capital is determined. Note: The selected data such as TBond rates; corporate tax rates; the long-term debt rates, market returns and equity risk- premium, are not precisely time sensitive to the dates noted in the exercise, but are depicted, only for purposes of the exercise