Answered step by step

Verified Expert Solution

Question

1 Approved Answer

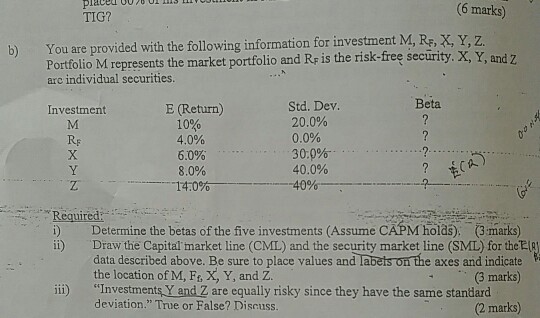

0UP8 ULs placed TIG? (6 marks) b) You are provided with the following information for investment M, RE, X, Y, z. Portfolio M represents the

0UP8 ULs placed TIG? (6 marks) b) You are provided with the following information for investment M, RE, X, Y, z. Portfolio M represents the market portfolio and Re is the risk-free security. X, Y, and 7 arc individual securities Beta E (Return) 10% 4.0% 60% 8.0% Std. Dev 20.0% 0.0% 30:0%.. 40.0% 40% Investment RF Required: ) Determine the betas of the five investments (Assume CPM holds) (3 marks) Draw the Capital' market line (CML) and the security market line (SML) for the data described above. Be sure to place values and labets on the axes and indicate the location of M, F, X, Y, and Z. "Investments Y and Z are equally risky since they have the same standard deviation." True or False? Discuss (3 marks) iii) (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Climate Finance Theory And Practice

Authors: Anil Markandya, Ibon Galarraga, Dirk Rübbelke

1st Edition

9814641804, 978-9814641807