Answered step by step

Verified Expert Solution

Question

1 Approved Answer

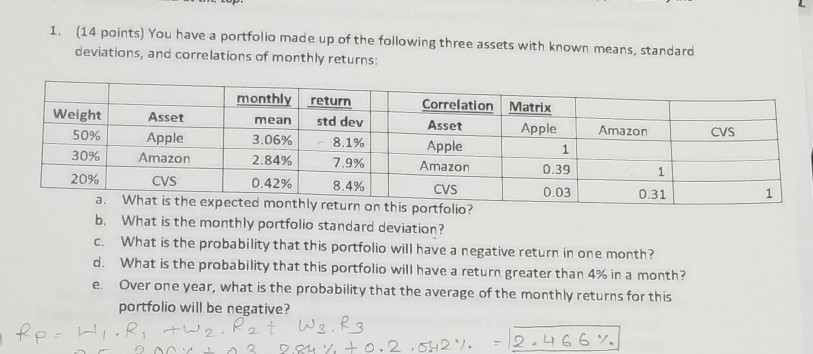

1. (14 points) You have a portfolio made up of the following three assets with known means, standard deviations, and correlations of monthly returns: CVS

1. (14 points) You have a portfolio made up of the following three assets with known means, standard deviations, and correlations of monthly returns: CVS 1 monthly return Correlation Matrix Weight Asset mean std dev Asset Apple Amazon 50% Apple 3.06% 8.1% Apple 1 30% Amazon 2.84% 7.9% Amazon 0.39 1 20% CVS 0.42% 8.4% CVS 0.03 0.31 a. What is the expected monthly return on this portfolio? b. What is the monthly portfolio standard deviation? c. What is the probability that this portfolio will have a negative return in one month? d. What is the probability that this portfolio will have a return greater than 4% in a month? Over one year, what is the probability that the average of the monthly returns for this portfolio will be negative? fp = WIOR, TW2. . Rat Wz. R3 2 8.847 +0.2.0422. = 2.4664 e

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Developments In Entrepreneurial Finance And Technology

Authors: David B. Audretsch, Maksim Belitski, Nada Rejeb, Rosa Caiazza

1st Edition

1800884338,1800884346