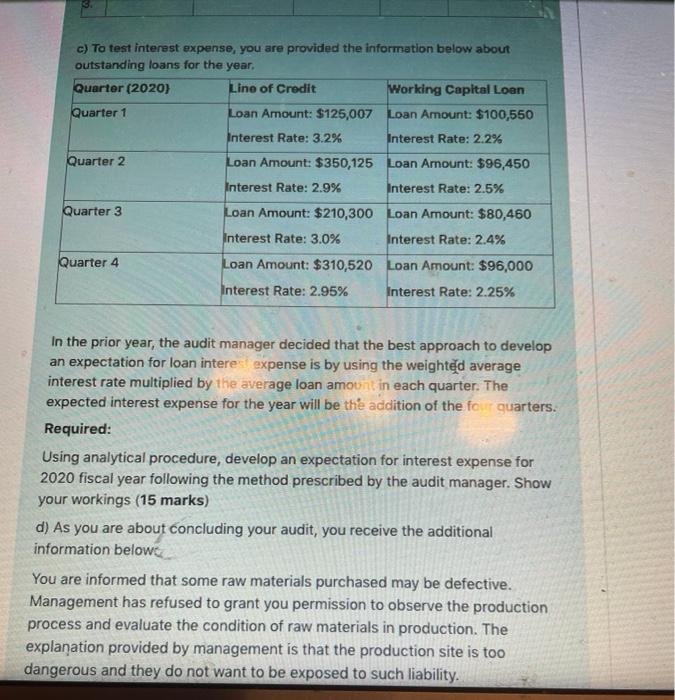

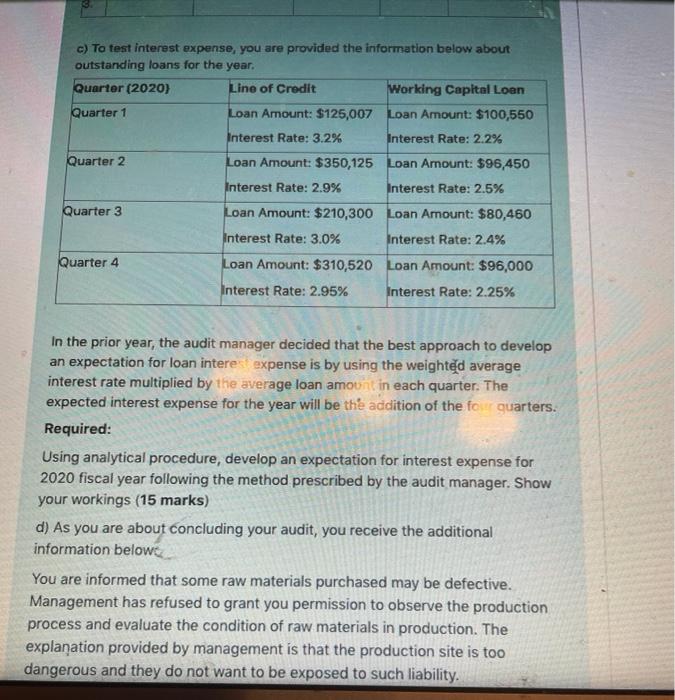

1 2 Tarked out of 5.00 Flag astian 10 11 19 JIN SEC 26 SEC 2 i Finis Integrated Solutions (IC) is an American public company established fifteen years ago. The company manufactures high end marble and granite primarily for customers in the construction industry. The CEO, Greg Baker, is a proponent of strong work ethics and has previously won the Ethics in Business Award. The company takes pride in having recorded few instances of inventory theft since inception. Although, raw material valuation can be a bit tricky, IC has been able to simplify the process of allocating indirect materials, labour, and manufacturing overhead to work in process. This method has been accepted by the auditors as adequate. By law, IC is required to have an audit of its annual financial statements by independent auditors. Your audit firm is currently conducting the audit for December 31 2020 Fiscal year end. You have been assigned the audit of inventory and interest expense. The strategy adopted by your audit firm is to determine inventory quantities by a physical count near the end of the reporting period. The quantities are then adjusted to balance sheet quantities by reference to the perpetual inventory system. You are provided with an extract from the inventory process documentation below: Physical comparison et in vantory with inventory records This function consists of an inventory count and a comparison of the actual items on hand with the inventory records. Marble and granite inverfory are stored in two warehouses. The first warehouse is used for the high-end products, these are products with rare patterns and vibrant colours. The second warehouse is for mid-range products and work-in-process inventory. There is clear separation of the finished goods and the work-in-process and movement from one unit to another requires issuance of a duly authorized inventory transfer requisition. The warehouse manager supervises the inventory count as he is very experienced with the inventory. The warehouse manager and warehouse staff are not however involved in the count. There are two teams of counters and each team will contain three members of staff, one staff from the manufacturing departments, the second from the accounts department and the third staff from the administrative department. The inventory is arranged in Tim MacBook Air Ourses nistes labelled by product typo. Due to the nature of the inventory, counting teams are not required to lift products to ascertain the physical condition of the inventory. After counting each Isle, the team will hand in the sheets to the warehouse supervisor before moving to the next aisle. The count sheets are pre-printed and pre-numbered. The quantity is entered in ink and the warehouse supervisor ensures all assigned sheets are turned in In addition to the above procedure, the team assigned to the second warehouse are required to ensure there is no mix-up between raw materials and finished goods as minimal production will still be ongoing at the time of the count and this may necessitate the movement of inventory from one section to the other. Comparison of the count to the inventory records is conducted by the staff from the accounts department. The quantity of raw material is estimated using the height and width of raw material piles. Previously, the company used the services of a specialist to provide an estimate. The warehouse manager now performs this task as he had acquired the expertise from a previous job. End. Required a) Using the audit risk model, assess the risks associated with the audit of inventory of Integrated Solutions. (10 marks) b) Identify three weaknesses in the inventory count arrangement of IC, for each weakness, state the implication of the weakness, provide a necessary control to mitigate the weakness, state how this control can be tested and the assertion(s) at risk. (15 marks) You may use the format below. Weakness Implication of Necessary Tests of Assertion(s) at weakness control control risk 11. 2. 3. Ourses msies boned by product type. Due to the nature of the inventory, counting teams are not required to lift products to ascertain the physical condition of the inventory. After counting each islo, the team will hand in the sheets to the warehouse supervisor before moving to the next aisie. The count sheets are pre-printed and pre-numbered. The quantity is entered in ink and the warehouse supervisor ensures all assigned sheets are turned in. In addition to the above procedure, the team assigned to the second warehouse are required to ensure there is no mix-up between raw materials and finished goods as minimal production will still be ongoing at the time of the count and this may necessitate the movement of inventory from one section to the other. Comparison of the count to the inventory records is conducted by the staff from the accounts department. The quantity of raw material is estimated using the height and width of raw material piles. Previously, the company used the services of a specialist to provide an estimate. The warehouse manager now performs this task as he had acquired the expertise from a previous job. End. Required a) Using the audit risk model, assess the risks associated with the audit of inventory of Integrated Solutions. (10 marks) b) Identify three weaknesses in the inventory count arrangement of IC, for each weakness, state the implication of the weakness, provide a necessary control to mitigate the weakness, state how this control can be tested and the assertion(s) at risk. (15 marks) You may use the format below. Weakness implication of Necessary Tests of Assertion(s) at weakness control control risk 1. 2. 3. c) To test interest expense, you are provided the information below about outstanding loans for the year. Quarter (2020) Lino of Credit Working Capital Loan Quarter 1 Loan Amount: $125,007 Loan Amount: $100,550 Interest Rate: 3.2% Interest Rate: 2.2% Quarter 2 Loan Amount: $350,125 Loan Amount: $96,450 Interest Rate: 2.9% Interest Rate: 2.5% Loan Amount: $210,300 Loan Amount: $80,460 Interest Rate: 3.0% Interest Rate: 2.4% Quarter 3 Quarter 4 Loan Amount: $310,520 Loan Amount: $96,000 Interest Rate: 2.95% Interest Rate: 2.25% In the prior year, the audit manager decided that the best approach to develop an expectation for loan intere expense is by using the weighted average interest rate multiplied by the average loan amount in each quarter. The expected interest expense for the year will be the addition of the four quarters. Required: Using analytical procedure, develop an expectation for interest expense for 2020 fiscal year following the method prescribed by the audit manager. Show your workings (15 marks) d) As you are about concluding your audit, you receive the additional information below You are informed that some raw materials purchased may be defective. Management has refused to grant you permission to observe the production process and evaluate the condition of raw materials in production. The explanation provided by management is that the production site is too dangerous and they do not want to be exposed to such liability. Ourses antes imbelled by product typo. Due to the nature of the inventory, counting teams are not required to lift products to ascertain the physical condition of the inventory. After counting each Isle, the team will hand in the sheets to the warehouse supervisor before moving to the next aisle. The count sheets are pre-printed and pre-numbered. The quantity is entered in ink and the warehouse supervisor ensures all assigned sheets are turned in In addition to the above procedure, the team assigned to the second warehouse are required to ensure there is no mix-up between raw materials and finished goods as minimal production will still be ongoing at the time of the count and this may necessitate the movement of inventory from one section to the other. Comparison of the count to the inventory records is conducted by the staff from the accounts department. The quantity of raw material is estimated using the height and width of raw material piles. Previously, the company used the services of a specialist to provide an estimate. The warehouse manager now performs this task as he had acquired the expertise from a previous job. End Required a) Using the audit risk model, assess the risks associated with the audit of inventory of Integrated Solutions. (10 marks) b) Identify three weaknesses in the inventory count arrangement of IC, for each weakness, state the implication of the weakness, provide a necessary control to mitigate the weakness, state how this control can be tested and the assertion(s) at risk. (15 marks) You may use the format below. Weakness - Implication of Necessary Tests of Assertion(s) at weakness control control risk 11. 2. 13. c) To test interest expense, you are provided the information below about outstanding loans for the year. Quarter (2020) Line of Credit Working Capital Loan Quarter 1 Loan Amount: $125,007 Loan Amount: $100,550 Interest Rate: 3.2% Interest Rate: 2.2% Quarter 2 Quarter 3 Loan Amount: $350,125 Loan Amount: $96,450 Interest Rate: 2.9% Interest Rate: 2.5% Loan Amount: $210,300 Loan Amount: $80,460 Interest Rate: 3.0% Interest Rate: 2.4% Loan Amount: $310,520 Loan Amount: $96,000 Interest Rate: 2.95% Interest Rate: 2.25% Quarter 4 In the prior year, the audit manager decided that the best approach to develop an expectation for loan intere expense is by using the weighted average interest rate multiplied by the average loan amount in each quarter. The expected interest expense for the year will be the addition of the fou quarters. Required: Using analytical procedure, develop an expectation for interest expense for 2020 fiscal year following the method prescribed by the audit manager. Show your workings (15 marks) d) As you are about concluding your audit, you receive the additional information below You are informed that some raw materials purchased may be defective. Management has refused to grant you permission to observe the production process and evaluate the condition of raw materials in production. The explanation provided by management is that the production site is too dangerous and they do not want to be exposed to such liability. 1 2 Tarked out of 5.00 Flag astian 10 11 19 JIN SEC 26 SEC 2 i Finis Integrated Solutions (IC) is an American public company established fifteen years ago. The company manufactures high end marble and granite primarily for customers in the construction industry. The CEO, Greg Baker, is a proponent of strong work ethics and has previously won the Ethics in Business Award. The company takes pride in having recorded few instances of inventory theft since inception. Although, raw material valuation can be a bit tricky, IC has been able to simplify the process of allocating indirect materials, labour, and manufacturing overhead to work in process. This method has been accepted by the auditors as adequate. By law, IC is required to have an audit of its annual financial statements by independent auditors. Your audit firm is currently conducting the audit for December 31 2020 Fiscal year end. You have been assigned the audit of inventory and interest expense. The strategy adopted by your audit firm is to determine inventory quantities by a physical count near the end of the reporting period. The quantities are then adjusted to balance sheet quantities by reference to the perpetual inventory system. You are provided with an extract from the inventory process documentation below: Physical comparison et in vantory with inventory records This function consists of an inventory count and a comparison of the actual items on hand with the inventory records. Marble and granite inverfory are stored in two warehouses. The first warehouse is used for the high-end products, these are products with rare patterns and vibrant colours. The second warehouse is for mid-range products and work-in-process inventory. There is clear separation of the finished goods and the work-in-process and movement from one unit to another requires issuance of a duly authorized inventory transfer requisition. The warehouse manager supervises the inventory count as he is very experienced with the inventory. The warehouse manager and warehouse staff are not however involved in the count. There are two teams of counters and each team will contain three members of staff, one staff from the manufacturing departments, the second from the accounts department and the third staff from the administrative department. The inventory is arranged in Tim MacBook Air Ourses nistes labelled by product typo. Due to the nature of the inventory, counting teams are not required to lift products to ascertain the physical condition of the inventory. After counting each Isle, the team will hand in the sheets to the warehouse supervisor before moving to the next aisle. The count sheets are pre-printed and pre-numbered. The quantity is entered in ink and the warehouse supervisor ensures all assigned sheets are turned in In addition to the above procedure, the team assigned to the second warehouse are required to ensure there is no mix-up between raw materials and finished goods as minimal production will still be ongoing at the time of the count and this may necessitate the movement of inventory from one section to the other. Comparison of the count to the inventory records is conducted by the staff from the accounts department. The quantity of raw material is estimated using the height and width of raw material piles. Previously, the company used the services of a specialist to provide an estimate. The warehouse manager now performs this task as he had acquired the expertise from a previous job. End. Required a) Using the audit risk model, assess the risks associated with the audit of inventory of Integrated Solutions. (10 marks) b) Identify three weaknesses in the inventory count arrangement of IC, for each weakness, state the implication of the weakness, provide a necessary control to mitigate the weakness, state how this control can be tested and the assertion(s) at risk. (15 marks) You may use the format below. Weakness Implication of Necessary Tests of Assertion(s) at weakness control control risk 11. 2. 3. Ourses msies boned by product type. Due to the nature of the inventory, counting teams are not required to lift products to ascertain the physical condition of the inventory. After counting each islo, the team will hand in the sheets to the warehouse supervisor before moving to the next aisie. The count sheets are pre-printed and pre-numbered. The quantity is entered in ink and the warehouse supervisor ensures all assigned sheets are turned in. In addition to the above procedure, the team assigned to the second warehouse are required to ensure there is no mix-up between raw materials and finished goods as minimal production will still be ongoing at the time of the count and this may necessitate the movement of inventory from one section to the other. Comparison of the count to the inventory records is conducted by the staff from the accounts department. The quantity of raw material is estimated using the height and width of raw material piles. Previously, the company used the services of a specialist to provide an estimate. The warehouse manager now performs this task as he had acquired the expertise from a previous job. End. Required a) Using the audit risk model, assess the risks associated with the audit of inventory of Integrated Solutions. (10 marks) b) Identify three weaknesses in the inventory count arrangement of IC, for each weakness, state the implication of the weakness, provide a necessary control to mitigate the weakness, state how this control can be tested and the assertion(s) at risk. (15 marks) You may use the format below. Weakness implication of Necessary Tests of Assertion(s) at weakness control control risk 1. 2. 3. c) To test interest expense, you are provided the information below about outstanding loans for the year. Quarter (2020) Lino of Credit Working Capital Loan Quarter 1 Loan Amount: $125,007 Loan Amount: $100,550 Interest Rate: 3.2% Interest Rate: 2.2% Quarter 2 Loan Amount: $350,125 Loan Amount: $96,450 Interest Rate: 2.9% Interest Rate: 2.5% Loan Amount: $210,300 Loan Amount: $80,460 Interest Rate: 3.0% Interest Rate: 2.4% Quarter 3 Quarter 4 Loan Amount: $310,520 Loan Amount: $96,000 Interest Rate: 2.95% Interest Rate: 2.25% In the prior year, the audit manager decided that the best approach to develop an expectation for loan intere expense is by using the weighted average interest rate multiplied by the average loan amount in each quarter. The expected interest expense for the year will be the addition of the four quarters. Required: Using analytical procedure, develop an expectation for interest expense for 2020 fiscal year following the method prescribed by the audit manager. Show your workings (15 marks) d) As you are about concluding your audit, you receive the additional information below You are informed that some raw materials purchased may be defective. Management has refused to grant you permission to observe the production process and evaluate the condition of raw materials in production. The explanation provided by management is that the production site is too dangerous and they do not want to be exposed to such liability. Ourses antes imbelled by product typo. Due to the nature of the inventory, counting teams are not required to lift products to ascertain the physical condition of the inventory. After counting each Isle, the team will hand in the sheets to the warehouse supervisor before moving to the next aisle. The count sheets are pre-printed and pre-numbered. The quantity is entered in ink and the warehouse supervisor ensures all assigned sheets are turned in In addition to the above procedure, the team assigned to the second warehouse are required to ensure there is no mix-up between raw materials and finished goods as minimal production will still be ongoing at the time of the count and this may necessitate the movement of inventory from one section to the other. Comparison of the count to the inventory records is conducted by the staff from the accounts department. The quantity of raw material is estimated using the height and width of raw material piles. Previously, the company used the services of a specialist to provide an estimate. The warehouse manager now performs this task as he had acquired the expertise from a previous job. End Required a) Using the audit risk model, assess the risks associated with the audit of inventory of Integrated Solutions. (10 marks) b) Identify three weaknesses in the inventory count arrangement of IC, for each weakness, state the implication of the weakness, provide a necessary control to mitigate the weakness, state how this control can be tested and the assertion(s) at risk. (15 marks) You may use the format below. Weakness - Implication of Necessary Tests of Assertion(s) at weakness control control risk 11. 2. 13. c) To test interest expense, you are provided the information below about outstanding loans for the year. Quarter (2020) Line of Credit Working Capital Loan Quarter 1 Loan Amount: $125,007 Loan Amount: $100,550 Interest Rate: 3.2% Interest Rate: 2.2% Quarter 2 Quarter 3 Loan Amount: $350,125 Loan Amount: $96,450 Interest Rate: 2.9% Interest Rate: 2.5% Loan Amount: $210,300 Loan Amount: $80,460 Interest Rate: 3.0% Interest Rate: 2.4% Loan Amount: $310,520 Loan Amount: $96,000 Interest Rate: 2.95% Interest Rate: 2.25% Quarter 4 In the prior year, the audit manager decided that the best approach to develop an expectation for loan intere expense is by using the weighted average interest rate multiplied by the average loan amount in each quarter. The expected interest expense for the year will be the addition of the fou quarters. Required: Using analytical procedure, develop an expectation for interest expense for 2020 fiscal year following the method prescribed by the audit manager. Show your workings (15 marks) d) As you are about concluding your audit, you receive the additional information below You are informed that some raw materials purchased may be defective. Management has refused to grant you permission to observe the production process and evaluate the condition of raw materials in production. The explanation provided by management is that the production site is too dangerous and they do not want to be exposed to such liability