Answered step by step

Verified Expert Solution

Question

1 Approved Answer

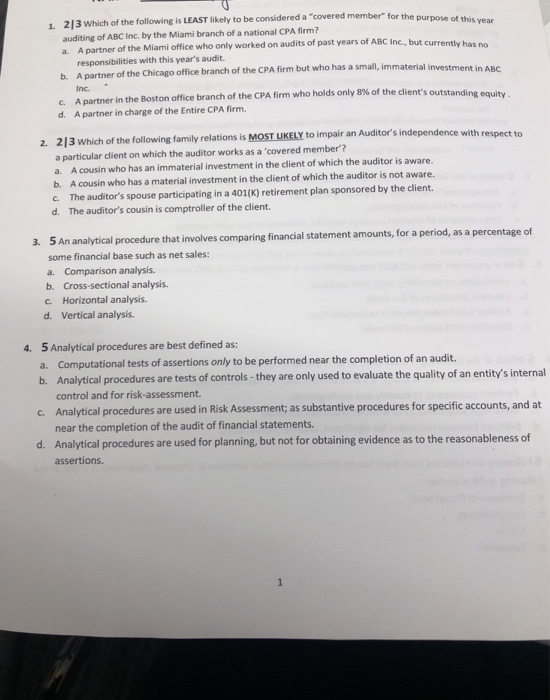

1. 213 Which of the following is LEAST likely to be considered a covered member for the purpose of this year auditing of ABC Inc.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Just In Time Accounting How To Decrease Costs And Increase Efficiency

Authors: Steven M. Bragg

3rd Edition

0470403721, 978-0470403723