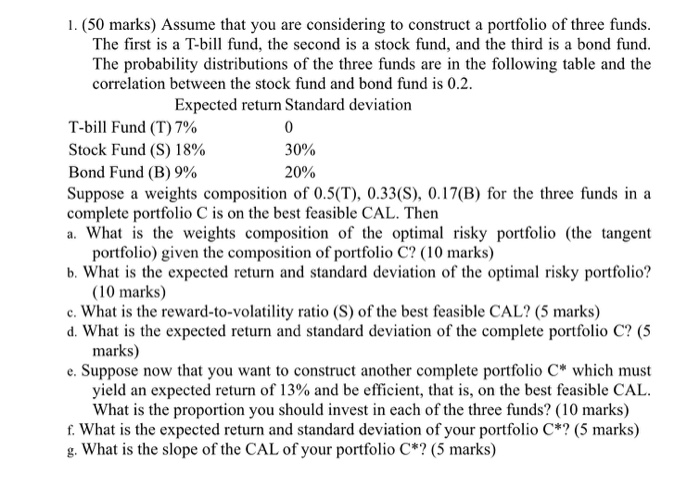

1. (50 marks) Assume that you are considering to construct a portfolio of three funds. The first is a T-bill fund, the second is a stock fund, and the third is a bond fund. The probability distributions of the three funds are in the following table and the correlation between the stock fund and bond fund is 0.2. Expected return Standard deviation T-bill Fund (T) 7% Stock Fund (S) 18% 30% Bond Fund (B) 9% 20% Suppose a weights composition of 0.5(T), 0.33(S), 0.17(B) for the three funds in a complete portfolio C is on the best feasible CAL. Then a. What is the weights composition of the optimal risky portfolio (the tangent portfolio) given the composition of portfolio C? (10 marks) b. What is the expected return and standard deviation of the optimal risky portfolio? (10 marks) c. What is the reward-to-volatility ratio (S) of the best feasible CAL? (5 marks) d. What is the expected return and standard deviation of the complete portfolio C? (5 marks) e. Suppose now that you want to construct another complete portfolio Cwhich must yield an expected return of 13% and be efficient, that is, on the best feasible CAL. What is the proportion you should invest in each of the three funds? (10 marks) f. What is the expected return and standard deviation of your portfolio C*? (5 marks) g. What is the slope of the CAL of your portfolio C*? (5 marks) 1. (50 marks) Assume that you are considering to construct a portfolio of three funds. The first is a T-bill fund, the second is a stock fund, and the third is a bond fund. The probability distributions of the three funds are in the following table and the correlation between the stock fund and bond fund is 0.2. Expected return Standard deviation T-bill Fund (T) 7% Stock Fund (S) 18% 30% Bond Fund (B) 9% 20% Suppose a weights composition of 0.5(T), 0.33(S), 0.17(B) for the three funds in a complete portfolio C is on the best feasible CAL. Then a. What is the weights composition of the optimal risky portfolio (the tangent portfolio) given the composition of portfolio C? (10 marks) b. What is the expected return and standard deviation of the optimal risky portfolio? (10 marks) c. What is the reward-to-volatility ratio (S) of the best feasible CAL? (5 marks) d. What is the expected return and standard deviation of the complete portfolio C? (5 marks) e. Suppose now that you want to construct another complete portfolio Cwhich must yield an expected return of 13% and be efficient, that is, on the best feasible CAL. What is the proportion you should invest in each of the three funds? (10 marks) f. What is the expected return and standard deviation of your portfolio C*? (5 marks) g. What is the slope of the CAL of your portfolio C*