Answered step by step

Verified Expert Solution

Question

1 Approved Answer

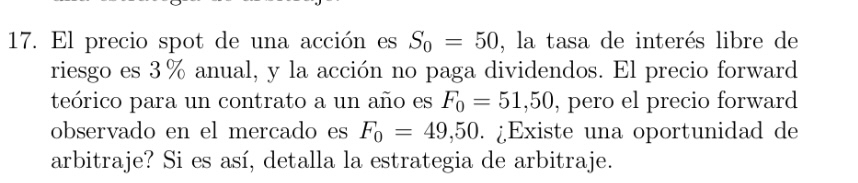

1 7 . The spot price of a stock is S 0 = 5 0 , the risk - free interest rate is 3 %

The spot price of a stock is S the riskfree interest rate is per year, and the stock pays no dividends. The theoretical forward price for a oneyear contract is F but the observed forward price in the market is F Is there an arbitrage opportunity? If so describe the arbitrage strategy.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Economics Discussion Series Bank Risk Rating Of Business Loans

Authors: United States Federal Reserve Board, William B. English, William R. Nelson

1st Edition

1288718810, 9781288718818