Answered step by step

Verified Expert Solution

Question

1 Approved Answer

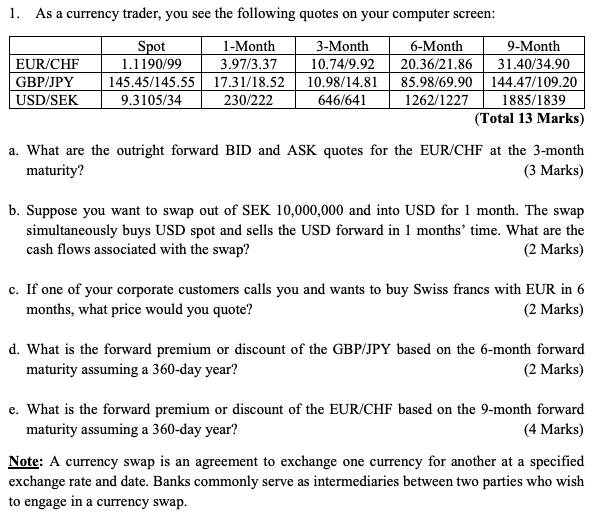

1. As a currency trader, you see the following quotes on your computer screen 1-Month 3.97/3.37 9-Month 6-Month 3-Month 0.74/9.92 20.36/21.86 31.40/34.90 1.1190/99 145.45/145.5517.31/18.52 10.98/14.8185.98/69.90

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Jeff Madura

5th edition

132994348, 978-0132994347