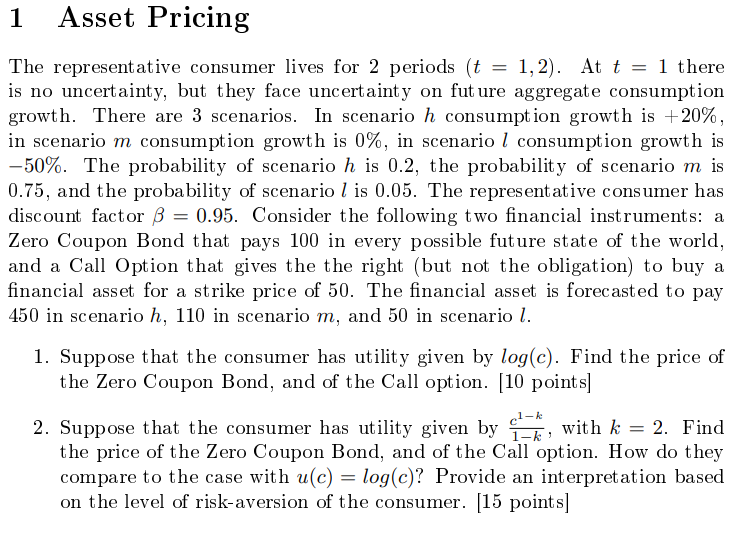

1 Asset Pricing . The representative consumer lives for 2 periods (t 1,2). At t = 1 there is no uncertainty, but they face uncertainty on future aggregate consumption growth. There are 3 scenarios. In scenario h consumption growth is +20%, in scenario m consumption growth is 0%, in scenario l consumption growth is -50%. The probability of scenario h is 0.2, the probability of scenario m is 0.75, and the probability of scenario l is 0.05. The representative consumer has discount factor B = 0.95. Consider the following two financial instruments: a Zero Coupon Bond that pays 100 in every possible future state of the world, and a Call Option that gives the the right (but not the obligation) to buy a financial asset for a strike price of 50. The financial asset is forecasted to pay 450 in scenario h, 110 in scenario m, and 50 in scenario l. 1. Suppose that the consumer has utility given by log(C). Find the price of the Zero Coupon Bond, and of the Call option. [10 points] 2. Suppose that the consumer has utility given by Ln, with k = 2. Find ci-k k = 1-k: the price of the Zero Coupon Bond, and of the Call option. How do they compare to the case with u(c) = log(c)? Provide an interpretation based on the level of risk-aversion of the consumer. [15 points] 1 Asset Pricing . The representative consumer lives for 2 periods (t 1,2). At t = 1 there is no uncertainty, but they face uncertainty on future aggregate consumption growth. There are 3 scenarios. In scenario h consumption growth is +20%, in scenario m consumption growth is 0%, in scenario l consumption growth is -50%. The probability of scenario h is 0.2, the probability of scenario m is 0.75, and the probability of scenario l is 0.05. The representative consumer has discount factor B = 0.95. Consider the following two financial instruments: a Zero Coupon Bond that pays 100 in every possible future state of the world, and a Call Option that gives the the right (but not the obligation) to buy a financial asset for a strike price of 50. The financial asset is forecasted to pay 450 in scenario h, 110 in scenario m, and 50 in scenario l. 1. Suppose that the consumer has utility given by log(C). Find the price of the Zero Coupon Bond, and of the Call option. [10 points] 2. Suppose that the consumer has utility given by Ln, with k = 2. Find ci-k k = 1-k: the price of the Zero Coupon Bond, and of the Call option. How do they compare to the case with u(c) = log(c)? Provide an interpretation based on the level of risk-aversion of the consumer. [15 points]