Answered step by step

Verified Expert Solution

Question

1 Approved Answer

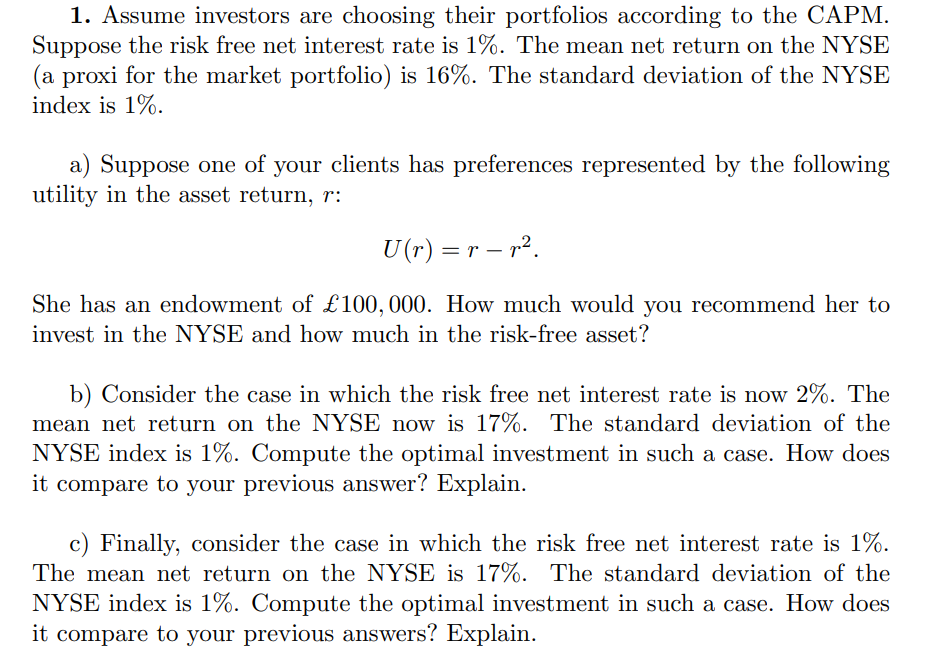

1. Assume investors are choosing their portfolios according to the CAPM. Suppose the risk free net interest rate is 1%. The mean net return on

1. Assume investors are choosing their portfolios according to the CAPM. Suppose the risk free net interest rate is 1%. The mean net return on the NYSE (a proxi for the market portfolio) is 16%. The standard deviation of the NYSE index is 1%. a) Suppose one of your clients has preferences represented by the following utility in the asset return, r: U(r) =s p2. She has an endowment of 100,000. How much would you recommend her to invest in the NYSE and how much in the risk-free asset? b) Consider the case in which the risk free net interest rate is now 2%. The mean net return on the NYSE now is 17%. The standard deviation of the NYSE index is 1%. Compute the optimal investment in such a case. How does it compare to your previous answer? Explain. c) Finally, consider the case in which the risk free net interest rate is 1%. The mean net return on the NYSE is 17%. The standard deviation of the NYSE index is 1%. Compute the optimal investment in such a case. How does it compare to your previous answers? Explain. 1. Assume investors are choosing their portfolios according to the CAPM. Suppose the risk free net interest rate is 1%. The mean net return on the NYSE (a proxi for the market portfolio) is 16%. The standard deviation of the NYSE index is 1%. a) Suppose one of your clients has preferences represented by the following utility in the asset return, r: U(r) =s p2. She has an endowment of 100,000. How much would you recommend her to invest in the NYSE and how much in the risk-free asset? b) Consider the case in which the risk free net interest rate is now 2%. The mean net return on the NYSE now is 17%. The standard deviation of the NYSE index is 1%. Compute the optimal investment in such a case. How does it compare to your previous answer? Explain. c) Finally, consider the case in which the risk free net interest rate is 1%. The mean net return on the NYSE is 17%. The standard deviation of the NYSE index is 1%. Compute the optimal investment in such a case. How does it compare to your previous answers? Explain

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding The Finance Of Welfare

Authors: Howard Glennerster

2nd Edition

1847421091, 978-1847421098