Answered step by step

Verified Expert Solution

Question

1 Approved Answer

1. Assume the following investment opportunities on the market shown in Table 1. They gen- erate a certain cash flow in t = 1,

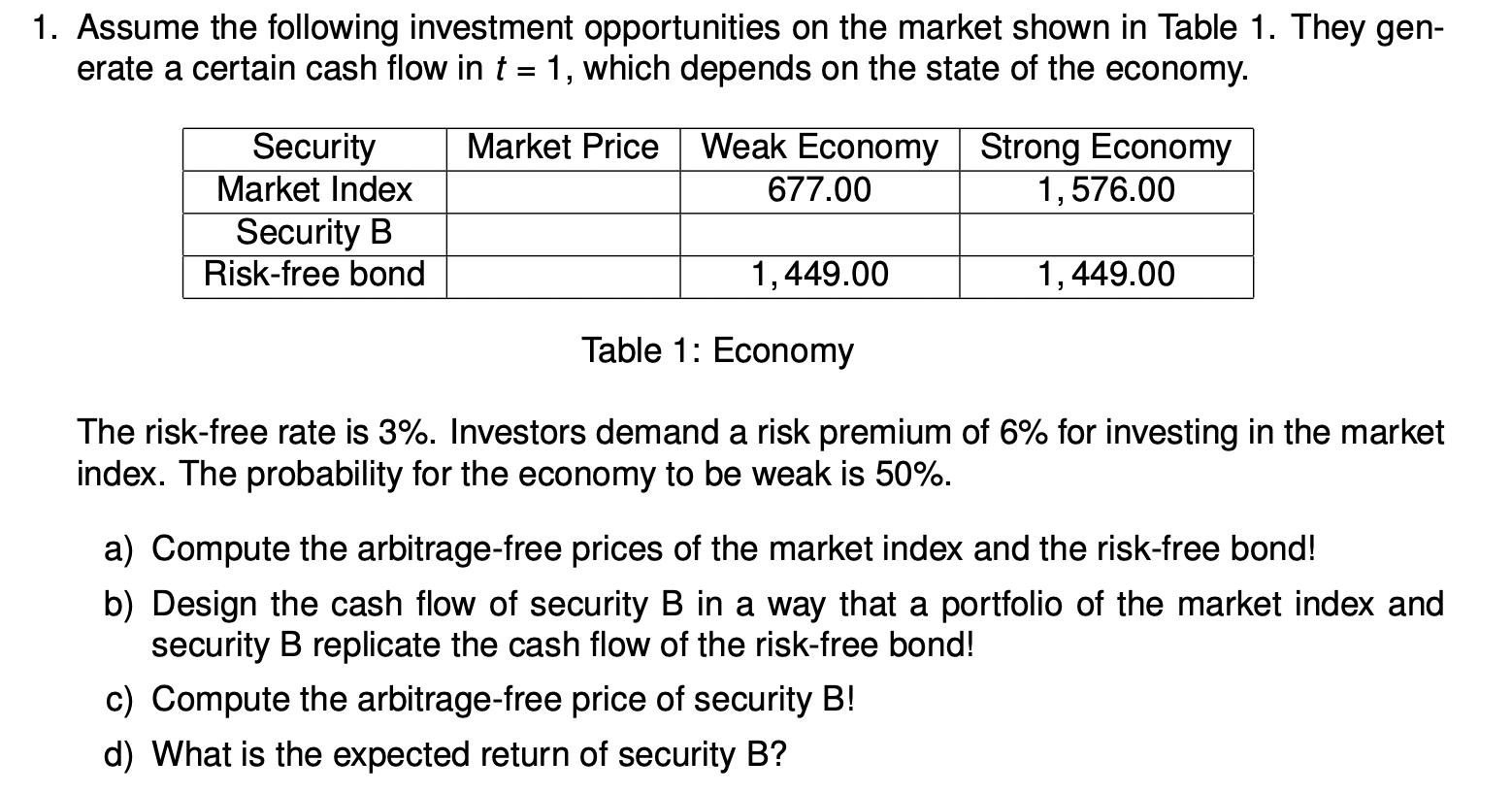

1. Assume the following investment opportunities on the market shown in Table 1. They gen- erate a certain cash flow in t = 1, which depends on the state of the economy. Market Price Weak Economy Strong Economy Security Market Index Security B Risk-free bond 677.00 1,449.00 Table 1: Economy 1,576.00 1,449.00 The risk-free rate is 3%. Investors demand a risk premium of 6% for investing in the market index. The probability for the economy to be weak is 50%. a) Compute the arbitrage-free prices of the market index and the risk-free bond! b) Design the cash flow of security B in a way that a portfolio of the market index and security B replicate the cash flow of the risk-free bond! c) Compute the arbitrage-free price of security B! d) What is the expected return of security B?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516