Question

1. Atreides International has operations in Arrakis. The balance sheet for this division in Arrakeen solaris shows assets of 17,000 solaris, debt in the amount

1. Atreides International has operations in Arrakis. The balance sheet for this division in Arrakeen solaris shows assets of 17,000 solaris, debt in the amount of 7,500 solaris, and equity of 9,500 solaris.

If the current exchange ratio is 2.1 solaris per dollar, what does the balance sheet look like in dollars?

Balance sheet:

- Assets = $8,095.24; Debt = $3,571.43; Equity = $4,523.81

- Assets = $35,700.00; Debt = $15,750.00; Equity = $19,950.00

- Assets = $8,500.00; Debt = $3,750.00; Equity = $4,750.00

- Assets = $7,690.48; Debt = $3,392.86; Equity = $4,297.62

- Assets = $8,419.05; Debt = $3,714.29; Equity = $4,704.76

Assume that one year from now the balance sheet in solaris is exactly the same as at the beginning of the year. If the exchange rate is 2.3 solaris per dollar, what does the balance sheet look like in dollars now?

Balance sheet:

- Assets = $7,391.30; Debt = $3,260.87; Equity = $4,130.43

- Assets = $39,100.00; Debt = $17,250.00; Equity = $21,850.00

- Assets = $7,760.87; Debt = $3,423.91; Equity = $4,336.96

- Assets = $7,021.74; Debt = $3,097.83; Equity = $3,923.91

- Assets = $7,686.96; Debt = $3,391.30; Equity = $4,295.65

2

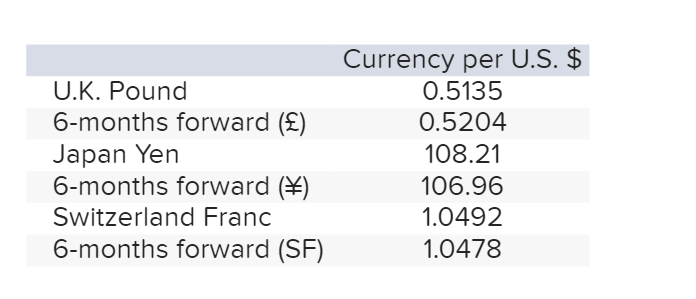

| Suppose interest rate parity holds, and the current six-month risk-free rate in the United States is 4.6 percent. |

| What must the six-month risk-free rate be in Great Britain? |

Great Britain risk-free rate:

- 5.94%

- 6.03%

- 3.27%

- 7.18%

- 5.71%

| What must the six-month risk-free rate be in Japan? Japanese risk-free rate:

|

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Managers

Authors: Harvard Business School Press

1st Edition

1578518768, 978-1578518760