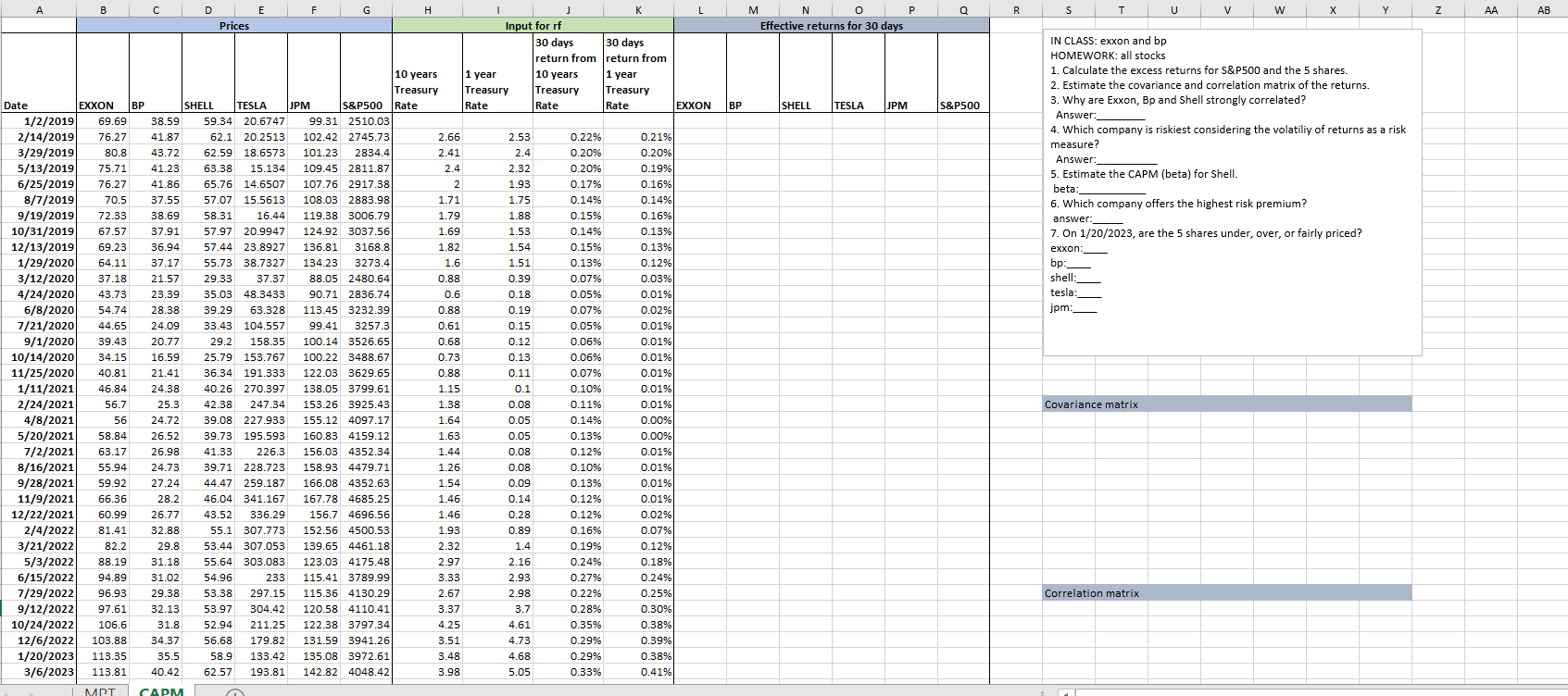

Question

1. Calculate the excess returns for S&P500 and the 5 shares. 2. Estimate the covariance and correlation matrix of the returns. 3. Why are Exxon,

1. Calculate the excess returns for S&P500 and the 5 shares.

2. Estimate the covariance and correlation matrix of the returns.

3. Why are Exxon, Bp and Shell strongly correlated?

Answer:________

4. Which company is riskiest considering the volatiliy of returns as a risk measure?

Answer:__________

5. Estimate the CAPM (beta) for Shell.

beta:___________

6. Which company offers the highest risk premium?

answer:_____

7. On 1/20/2023, are the 5 shares under, over, or fairly priced?

exxon:____

bp:____

shell:____

tesla:____

jpm:____

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Terrorist Finance

Authors: T. Wittig

2011th Edition

0230291848, 978-0230291843