Question

1. Compute the Sharpe ratios of the SB fund and gold. Based only on these ratios, how desirable does investment in the SB fund by

1. Compute the Sharpe ratios of the SB fund and gold. Based only on these ratios, how desirable does investment in the SB fund by itself compared to investment in Gold by itself?

2. What new portfolio consisting of the SB fund along with gold would maximize the Sharpe ratio?

3. What portfolio would minimize risk (volatility) for a target return of 11%?

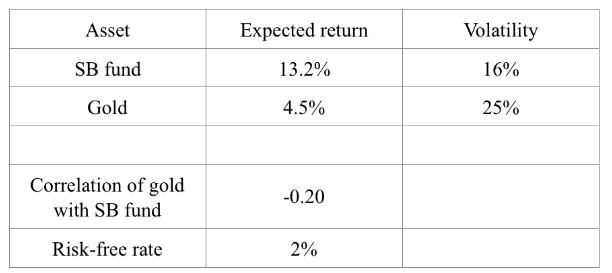

Asset SB fund Gold Correlation of gold with SB fund Risk-free rate Expected return 13.2% 4.5% -0.20 2% Volatility 16% 25%

Step by Step Solution

3.37 Rating (169 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Investments, Valuation and Management

Authors: Bradford Jordan, Thomas Miller, Steve Dolvin

8th edition

1259720697, 1259720691, 1260109437, 9781260109436, 978-1259720697