Answered step by step

Verified Expert Solution

Question

1 Approved Answer

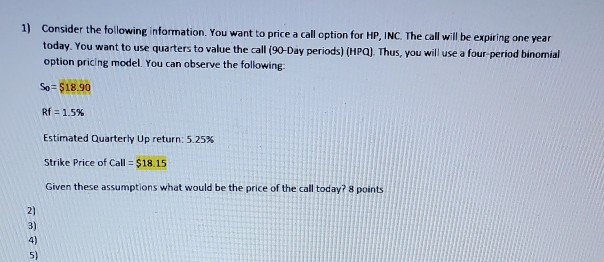

1) Consider the following information. You want to price a call option for HP, INC. The call will be expiring one year today. You want

1) Consider the following information. You want to price a call option for HP, INC. The call will be expiring one year today. You want to use quarters to value the call (90-Day periods) (HPC). Thus, you will use a four period binomial option pricing model. You can observe the following: So= $18.90 Rf = 1.5% Estimated Quarterly Up return: 5.25% Strike Price of Call = $18.15 Given these assumptions what would be the price of the call today? 8 points

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essential Retirement Planning For Solo Agers A Retirement And Aging Roadmap For Single And Childless Adults

Authors: Sara Zeff Geber

1st Edition

1633537684, 978-1633537682