Answered step by step

Verified Expert Solution

Question

1 Approved Answer

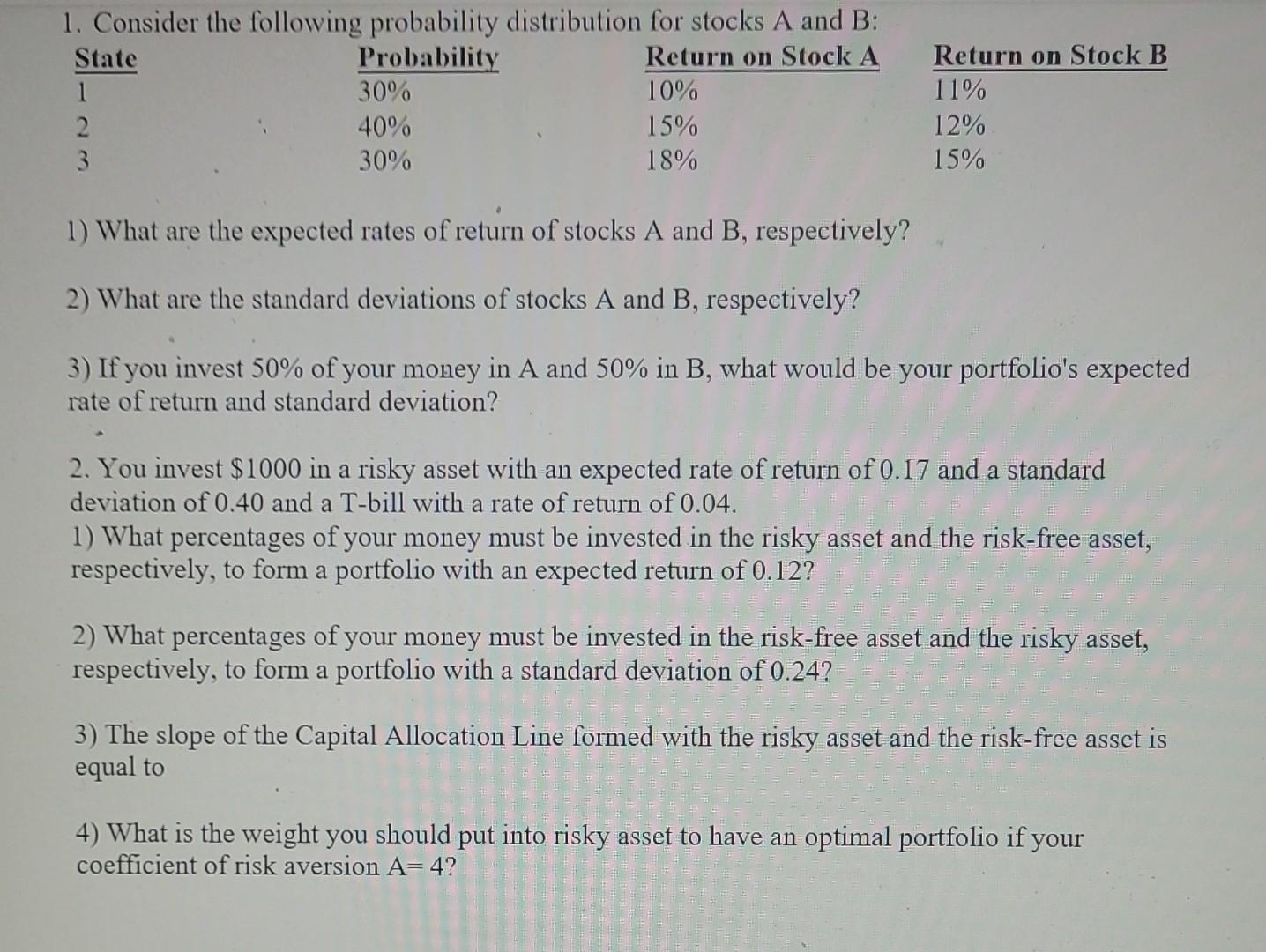

1. Consider the following probability distribution for stocks A and B: 1) What are the expected rates of return of stocks A and B, respectively?

1. Consider the following probability distribution for stocks A and B: 1) What are the expected rates of return of stocks A and B, respectively? 2) What are the standard deviations of stocks A and B, respectively? 3) If you invest 50% of your money in A and 50% in B, what would be your portfolio's expected rate of return and standard deviation? 2. You invest $1000 in a risky asset with an expected rate of return of 0.17 and a standard deviation of 0.40 and a T-bill with a rate of return of 0.04. 1) What percentages of your money must be invested in the risky asset and the risk-free asset, respectively, to form a portfolio with an expected return of 0.12 ? 2) What percentages of your money must be invested in the risk-free asset and the risky asset, respectively, to form a portfolio with a standard deviation of 0.24 ? 3) The slope of the Capital Allocation Line formed with the risky asset and the risk-free asset is equal to 4) What is the weight you should put into risky asset to have an optimal portfolio if your coefficient of risk aversion A=4

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Venture capital and the finance of innovation

Authors: Andrew Metrick

2nd Edition

9781118137888, 470454709, 1118137884, 978-0470454701