Answered step by step

Verified Expert Solution

Question

1 Approved Answer

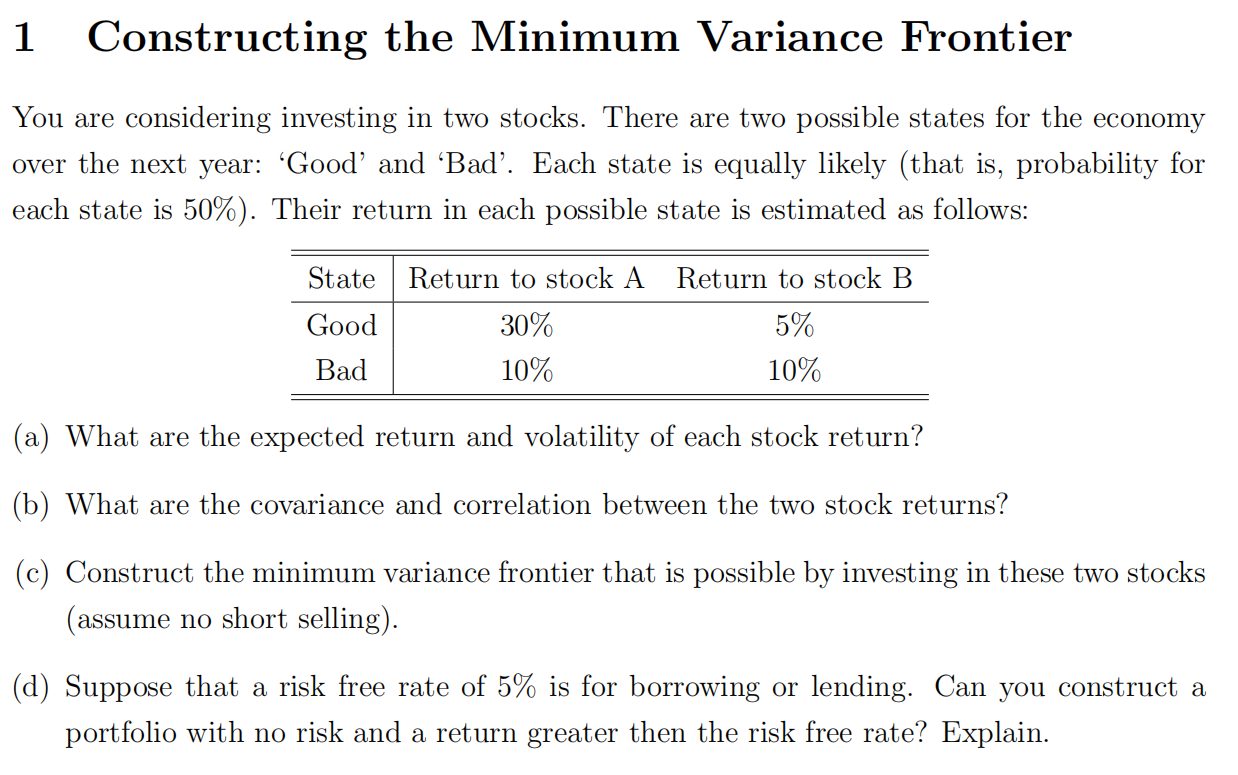

1 Constructing the Minimum Variance Frontier You are considering investing in two stocks. There are two possible states for the economy over the next year:

1 Constructing the Minimum Variance Frontier You are considering investing in two stocks. There are two possible states for the economy over the next year: 'Good' and 'Bad'. Each state is equally likely (that is, probability for each state is 50% ). Their return in each possible state is estimated as follows: (a) What are the expected return and volatility of each stock return? (b) What are the covariance and correlation between the two stock returns? (c) Construct the minimum variance frontier that is possible by investing in these two stocks (assume no short selling). (d) Suppose that a risk free rate of 5% is for borrowing or lending. Can you construct a portfolio with no risk and a return greater then the risk free rate? Explain

1 Constructing the Minimum Variance Frontier You are considering investing in two stocks. There are two possible states for the economy over the next year: 'Good' and 'Bad'. Each state is equally likely (that is, probability for each state is 50% ). Their return in each possible state is estimated as follows: (a) What are the expected return and volatility of each stock return? (b) What are the covariance and correlation between the two stock returns? (c) Construct the minimum variance frontier that is possible by investing in these two stocks (assume no short selling). (d) Suppose that a risk free rate of 5% is for borrowing or lending. Can you construct a portfolio with no risk and a return greater then the risk free rate? Explain Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Victorian Literature And Finance

Authors: Francis O'Gorman

1st Edition

0199281920, 978-0199281923