1. Describe the financial issue 2. What are the Development of assumptions

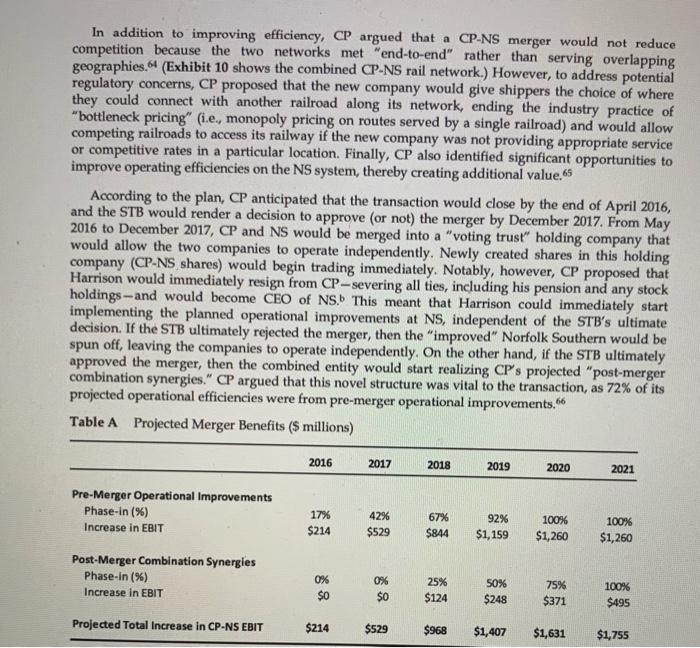

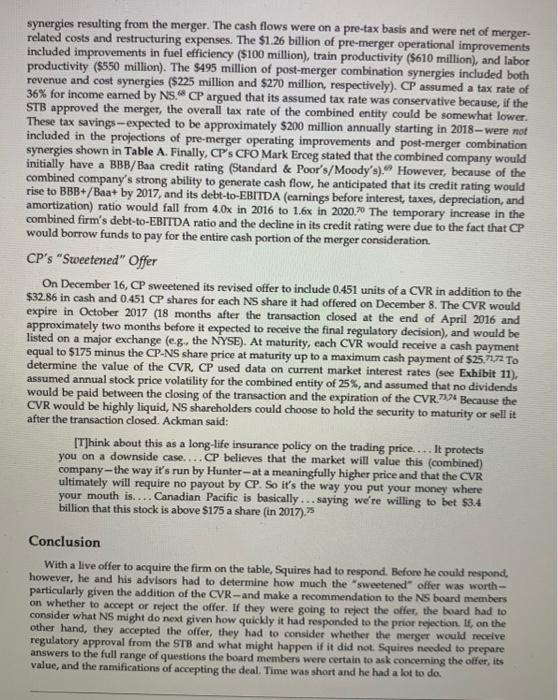

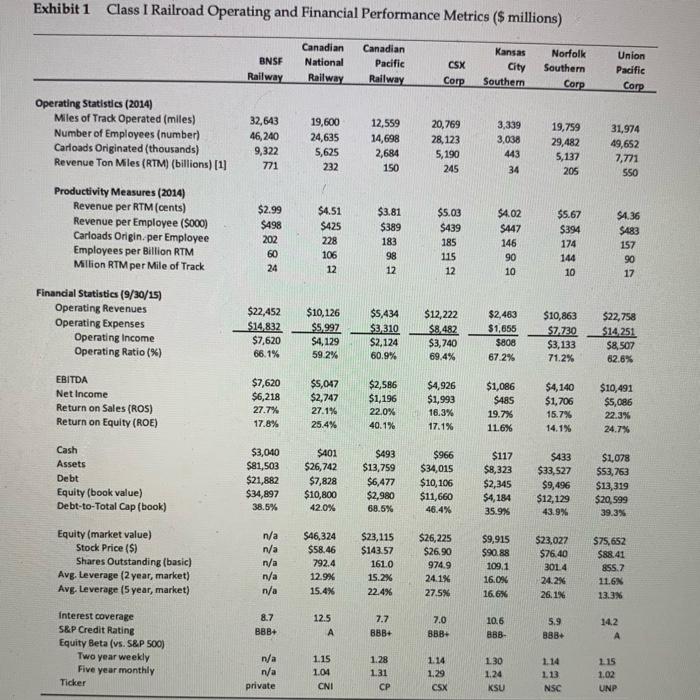

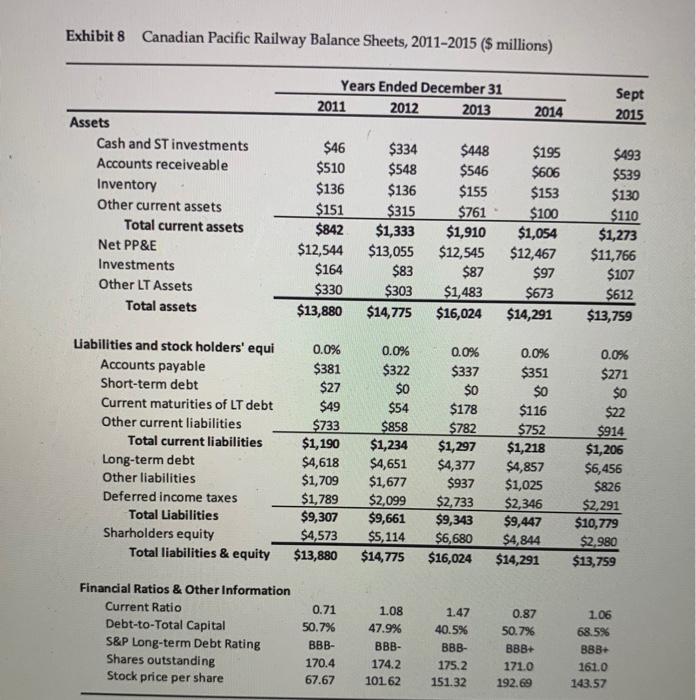

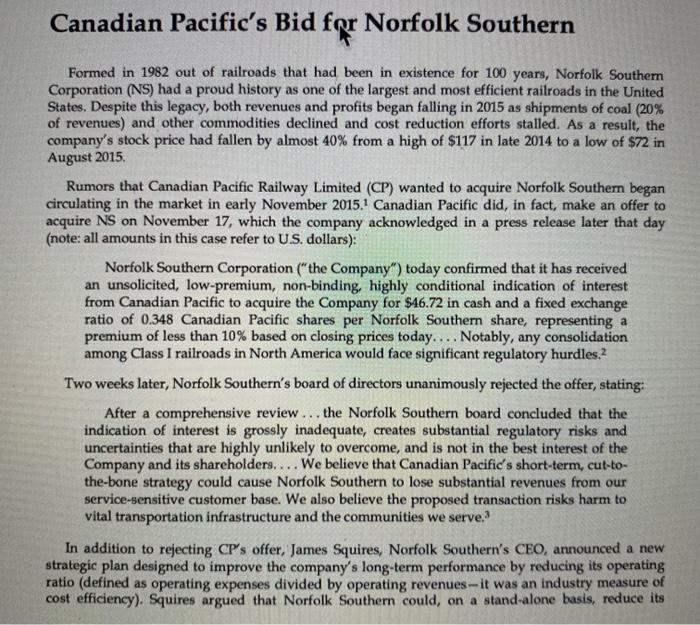

Canadian Pacific's Bid for Norfolk Southern Formed in 1982 out of railroads that had been in existence for 100 years, Norfolk Southern Corporation (NS) had a proud history as one of the largest and most efficient railroads in the United States. Despite this legacy, both revenues and profits began falling in 2015 as shipments of coal (20% of revenues) and other commodities declined and cost reduction efforts stalled. As a result, the company's stock price had fallen by almost 40% from a high of $117 in late 2014 to a low of $72 in August 2015 Rumors that Canadian Pacific Railway Limited (CP) wanted to acquire Norfolk Southern began circulating in the market in early November 2015.1 Canadian Pacific did, in fact, make an offer to acquire NS on November 17, which the company acknowledged in a press release later that day (note: all amounts in this case refer to U.S. dollars): Norfolk Southern Corporation ("the Company") today confirmed that it has received an unsolicited, low-premium, non-binding, highly conditional indication of interest from Canadian Pacific to acquire the Company for $46.72 in cash and a fixed exchange ratio of 0.348 Canadian Pacific shares per Norfolk Southern share, representing a premium of less than 10% based on closing prices today.... Notably, any consolidation among Class I railroads in North America would face significant regulatory hurdles. Two weeks later, Norfolk Southern's board of directors unanimously rejected the offer, stating: After a comprehensive review ... the Norfolk Southern board concluded that the indication of interest is grossly inadequate, creates substantial regulatory risks and uncertainties that are highly unlikely to overcome, and is not in the best interest of the Company and its shareholders.... We believe that Canadian Pacific's short-term, cut-to- the-bone strategy could cause Norfolk Southern to lose substantial revenues from our service-sensitive customer base. We also believe the proposed transaction risks harm to vital transportation infrastructure and the communities we serve. In addition to rejecting CP's offer, James Squires, Norfolk Southern's CEO, announced a new strategic plan designed to improve the company's long-term performance by reducing its operating ratio (defined as operating expenses divided by operating revenues-- it was an industry measure of cost efficiency). Squires argued that Norfolk Southern could, on a stand-alone basis, reduce its operating ratio from over 70% to below 65% by 2020 through aggressive cost reduction and, in doing so, generate double-digit earnings per share (EPS) growth Within days of the rejection, Canadian Pacific announced a revised offer and proposed a novel deal structure that would allow operational improvements at Norfolk Southern to be implemented even before the merger received regulatory approval. To further sweeten the deal, CP added a new security known as a Contingent Value Right (CVR) several days later. This security, which CP described as a "long-term insurance policy," was designed to protect investors if the share price of the combined entity fell below a certain level for any reason before the regulators approved the merger. By including the CVR in the deal, CP was demonstrating confidence in its ability to achieve the projected merger benefits. Before Squires and the NS board could respond to CP's "sweetened" offer, however, they had to review the offer with their financial and legal advisors, understand how the merger would affect the firm's operations and impact its shareholders, and prepare a response justifying their decision. That response would not only determine the firm's prospects for many years to come, but could affect Squires's professional reputation and career prospects, as well. The U.S. Railroad Industry The U.S. railroad industry had a long history of regulation starting with the establishment of the Interstate Commerce Commission (ICC) in 1887. ICC mandates and other federal regulation limited what railroads could charge on interstate routes, where they could construct new infrastructure, and whether they could divest rail lines. After growing for years, total rail mileage peaked in 1916 as the federal government began subsidizing highway construction? As trucking became an increasingly important form of competition, the share of intercity freight carried by trains fell steadily through the 1950s and 1960s. The 1970s was an especially difficult decade for railroads as inflation caused costs to rise (eg, fuel, labor, and equipment), yet regulations prevented railroads from raising rates commensurately. The end result was falling returns--the average return on investment (ROI) during the 1970s was 2%-and bankruptcies: Penn Central, a Class I railroad, declared bankruptcy in 1970, the largest U.S. corporate bankruptcy at that time. 10 The Staggers Rail Act of 1980 provided much needed relief to U.S. railroads, giving them the flexibility to set their own rates, abandon low-density routes, and make acquisitions with limited scrutiny. In the following years, a flurry of mergers intended to improve service, efficiency, and safety reduced the number of Class I railroads from 56 to 7.12 In this new consolidated environment, railroads regained financial stability as they streamlined operations and cut costs. For example, employment at Class 1 railroads fell from 458,000 people in 1980 to 178,000 people in 1998; and the industry's average operating ratio fell from 93% to 85%.1 With higher profitability, the average ROI grew to 7% in the 1990s and then to 9.4% by mid-2015.** (Exhibit 1 provides operating and financial statistics for the major railroads operating in the US and Canada as of 2015) Two important changes occurred in the 1990s. First, the Surface Transportation Board (STB) replaced the ICC as the primary regulator in 1996, and gained the ability to regulate all mergers and acquisitions. Second, the rapid consolidation of Class I railroads continued: Burlington Northern acquired Santa Fe Pacific in 1995 after an intense bidding war with Union Pacific, Union Pacific then acquired Southern Pacific in 1995;" CSX acquired Conrail in 1996 and agreed to split the railroad with Norfolk Southern as a solution to an escalating bidding war;" and finally, Canadian National acquired Illinois Central in 1998." (Exhibit 2 shows data on railroad acquisitions from 1995-2014.) Rather than enhancing service and improving efficiency as promised, these mergers often disrupted service, increased costs and prices), and reduced safety, at least in the short term, which prompted heightened regulatory scrutiny 2 For example, after BNSF and Canadian National agreed to merge in December 1999, the STB blocked the merger and froze all major rail mergers for 16 months, beginning in March 2000. According to the STB,"the shipping public has not yet fully recovered from the service interruptions associated with the previous round of mergers (from 1995 to 1998). "2 The next year, the STB established rules forbidding all railroad mergers unless they were in the public interest, as it tried to create a stable, balanced, and reliable rail transportation system."23 Under the new rules, companies had to demonstrate that merging with another railroad would boost competition and maintain service quality. 2 An STB spokesman said, "Although our new rules and policy statement do not, as the Class I railroads argue, reflect an anti-merger bias, we do plan to take a more skeptical 'show me' attitude toward claims of merger benefits and toward claims that no transitional problems would occur." At the time, the prevailing view was that another round of consolidation could leave the continent with just two Class I railroads.* Norfolk Southern Corporation Norfolk Southern Corporation (NS or NSC) was formed in 1982 by the merger of two railways: Norfolk & Westem and Southern Railway. As the fourth-largest Class I railroad operating in North America, NS had 30,456 employees, controlled 20,000 miles of track in 22 eastern states, and served all of the major East Coast ports. The company generated $20 billion of income on operating revenues of $11.6 billion in 2014. (Exhibits 3 and 4 show NS's income statements and balance sheets, respectively.) By early 2015, revenues and profits were falling and the firm's relative cost position was deteriorating. After being in the middle of the pack of Class I railroads in terms of its operating ratio, NS was at the high end of the group as of 2015. (Exhibit 5 shows operating ratios over time for Class I railroads). Analysts, however, expected the firm's performance would improve in the coming years. (Exhibit 6 shows financial projections for NS on a stand-alone basis according to equity analysts at UBS in October 2015.) Squires became CEO of NS on June 1, 2015, at the age of 53. When former CEO Charles "Wick Moorman announced his successor, he said, "I am confident that the company is poised for continued growth, success, and shareholder value creation." Squires had joined the company in 1992, as a newly minted graduate of the University of Chicago Law School. He rose through the ranks of the legal division before being named senior vice president of financial planning in 2006, CFO in 2007 and then president in 2013, Canadian Pacific Railway Limited Canadian Pacific Railway Ltd. was founded in the late 19 century to connect the major cities in eastern Canada with the less populous western territories. By 1986, CP had become Canada's second- largest company. Headquartered in Calgary, Alberta, CP had 13.700 employees and operated 12,500 miles of track in Canada as well as the midwestern and northeastern parts of the United States CP's main competitors were Canadian National Railway Company (Canadian National) in Canada and BNSF Railway in the U.S. Midwest. With revenues of $5.7 billion and net income of $1.3 billion in 2014, CP was considerably smaller than NS.3 (Exhibits 7 and 8 show CP's income statements and balance sheets, respectively.) In 2011, hedge-fund manager and activist investor William Bill" Ackman (HBS 1992) acquired a 12% stake in CP through his firm Pershing Square Capital Management. Ackman was known in the financial world for his overwhelming confidence and his willingness to place enormous bets based on his convictions. For example, he told one author: "I don't care what other people think. I invest based on what I believe the opportunity for profit is compared with my estimate of the potential for loss. ** Ackman subsequently forced CP's CEO to resign, ousted the company's board of directors, and installed Hunter Harrison as chief executive after a proxy fight.1 Harrison, a long-term railroad executive, had retired as the CEO of Canadian National (CN) in 2009.2 During his time at CN, Harrison had won various awards, including Canadian CEO of the Year and Railroader of the Year 44 Harrison believed consolidation was a good way to add critical rail capacity and simultaneously improve efficiency. Toward that end, he had unsuccessfully approached CSX Corp, another Class I railroad located in the eastern United States, in 2014 about a possible merger, arguing, "A pro- competition, customer-friendly, safety-focused railway combination is one such solution that could not be ignored on its merits by regulators." Yet NS's then CEO Moorman said in 2014 that major railroad mergers would be "highly problematic" from both a regulatory and a service perspective Absent mergers, careful cost control could also improve efficiency. In fact, under Harrison's leadership, CP's operating ratio had fallen from 81% in 2011 to close to 60% in 2015. In response, the firm's share price during his tenure had soared from less than $68 at the end of 2011 to almost $215 in October 2014, yet had fallen back down to 5135 as of early November 2015." (CP was traded on both the Toronto and New York stock exchanges.) Bidding for Norfolk Southern Despite market rumors of a possible bid for NS by CP, CP denied the rumors in a press release on November 9, claiming: "[There is no material news pending at this time. CP does not comment on market rumor and speculation."" Nevertheless, NS's stock price increased 11.0% (from $79.87 to $88.62) and CP's price increased 5.9% (from $134.31 to $142.18) on a day the market was down 10%. Eight days later, after the market closed on November 17, 2015, CP did, in fact, make an offer for NS: Canadian Pacific (CP)... has sent an offer letter to Norfolk Southern Corp. (NS) proposing a business combination ... The proposal, which includes a sizable premium in cash and stock offered to NS shareholders, would result in a company with the potential for faster earnings growth than either CP or NS could achieve on their own, all the while maintaining a strong investment grade credit rating.So NS confirmed that it had received an offer from CP to acquire the firm's shares for $46.72 in cash and a fixed exchange ratio of 0.348 CP shares for each NS share. Based on closing stock prices that day, reporters estimated the offer was worth $94.95 per NS share (-$46.72 in cash +0.348 * $138.58), which represented an acquisition premium of 9% over NS's closing price of $86.97. The next day, after the market incorporated the news of the proposed acquisition, NS's share price increased 6.3% to $92.49, while CP's price increased 5.4% to $146.65.9 NS responded by saying that in addition to facing significant regulatory hurdles," the offer was deficient, with a premium of less than 10% over the previous day's closing share price of $86.97 CP responded by noting that there had been a significant run-up in NS's share price due to market rumors of the impending bid, and that its offer should be compared to an "unaffected" share price that did not include the effect of the potential merger. In addition, CP argued that the merger would result in significant improvements in operating performance and synergies that should explicitly be recognized when valuing the offer 55 On December 4, 2015, the NS board of directors rejected the CP offer, stating that it was "grossly inadequate."** CEO Squires said: There is a high probability that, after years of disruption and expense, the proposed combination would be rejected by the Surface Transportation Board.... Even if the proposed combination were ultimately to be cleared, it would be subject to a wide range of onerous conditions that would reduce the value of the stock consideration that has been proposed. Canadian Pacific quickly revised its offer to $32.86 in cash and 0.451 CP shares for each NS share (ie, less cash and more stock) on December 8.5* During a conference call that day, Harrison and Ackman gave formal presentations about the proposed merger and took questions from analysts regarding the merits of the proposed combination. A vocal advocate for the merger, Ackman dismissed the NS board's resistance to the deal as similar to the resistance that followed his efforts to install Harrison as CEO of CP in 2012. "I've seen this movie before," he said." Following the second conference call about the deal on December 16, NS and CP closed at $89.79 and $128.56, respectively. (Exhibits 9a and 9b show stock prices for CP and NS from October 1 through December 18.) The Merger Rationale According to CP, the merger provided an opportunity to create a 21 century railroad for a 21- century economy."60 Although additional rail capacity was desperately needed to meet the demands of a growing economy, it was becoming increasingly difficult to add rail infrastructure in urban areas where most customers were located and railroads exchanged freight with trucks. CP argued that industry consolidation offered the best opportunity to improve efficiency and add incremental capacity without requiring additional infrastructure. Importantly, consolidation would also improve service for shippers. Nowhere was the need for additional infrastructure more crucial than in Chicago, Illinois. In 2014, close to 25% of U.S. rail traffic passed through Chicago, and the volume of traffic was expected to double over the next 10 years. Despite various attempts to add infrastructure, the problem was only getting worse. CP argued that the CP-NS merger offered the best opportunity to increase capacity in the critical Chicago train yards: Consolidation enables far better utilization of existing infrastructure. For example, trains interchanged in Chicago today must be broken apart and rebuilt in yards within the city and then delivered to receiving carriers. The process involves multiple interchanges between multiple carriers in multiple yards. A merger would allow these activities to be performed elsewhere so that trains moving through Chicago can move smoothly through the city without exiting the mainline... A merger would allow CP- NS to provide end-to-end service to customers, without hand-offs and interchanges Reducing these disruptive activities can significantly improve velocity, lower costs, and enable the combined company to move goods more quickly without increasing rates In addition to improving efficiency, CP argued that a CP-NS merger would not reduce competition because the two networks met "end-to-end" rather than serving overlapping geographies. (Exhibit 10 shows the combined CP-NS rail network.) However, to address potential regulatory concerns, CP proposed that the new company would give shippers the choice of where they could connect with another railroad along its network, ending the industry practice of "bottleneck pricing" (ie, monopoly pricing on routes served by a single railroad) and would allow competing railroads to access its railway if the new company was not providing appropriate service or competitive rates in a particular location. Finally, CP also identified significant opportunities to improve operating efficiencies on the NS system, thereby creating additional value 65 According to the plan, CP anticipated that the transaction would close by the end of April 2016, and the STB would render a decision to approve (or not) the merger by December 2017. From May 2016 to December 2017, CP and NS would be merged into a "voting trust" holding company that would allow the two companies to operate independently. Newly created shares in this holding company (CP-NS shares) would begin trading immediately. Notably, however, CP proposed that Harrison would immediately resign from CP-severing all ties, including his pension and any stock holdings -and would become CEO of NS. This meant that Harrison could immediately start implementing the planned operational improvements at NS, independent of the STB's ultimate decision. If the STB ultimately rejected the merger, then the "improved" Norfolk Southern would be spun off, leaving the companies to operate independently. On the other hand, if the STB ultimately approved the merger, then the combined entity would start realizing CP's projected "post-merger combination synergies." CP argued that this novel structure was vital to the transaction, as 72% of its projected operational efficiencies were from pre-merger operational improvements.66 Table A Projected Merger Benefits ($ millions) 2016 2017 2018 2019 2020 2021 Pre-Merger Operational Improvements Phase-in (%) Increase in EBIT 42% 17% $214 $529 67% $844 92% $1,159 100% $1,260 100% $1,260 Post-Merger Combination Synergies Phase-In (%) Increase in EBIT 25% 0% $0 0% $0 $124 50% $248 75% $371 100% $495 Projected Total Increase in CP-NS EBIT $214 $529 $968 $1,407 $1,631 $1,755 synergies resulting from the merger. The cash flows were on a pre-tax basis and were net of merger- related costs and restructuring expenses. The $1.26 billion of pre-merger operational improvements included improvements in fuel efficiency ($100 million), train productivity ($610 million), and labor productivity ($550 million). The $495 million of post-merger combination synergies included both revenue and cost synergies ($225 million and $270 million, respectively). CP assumed a tax rate of 36% for income earned by NS. CP argued that its assumed tax rate was conservative because, if the STB approved the merger, the overall tax rate of the combined entity could be somewhat lower. These tax savings --expected to be approximately $200 million annually starting in 2018-were not included in the projections of pre-merger operating improvements and post-merger combination synergies shown in Table A. Finally, CP's CFO Mark Erceg stated that the combined company would initially have a BBB/Baa credit rating (Standard & Poor's/Moody's). However, because of the combined company's strong ability to generate cash flow, he anticipated that its credit rating would rise to BBB+/Baat by 2017, and its debt-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio would fall from 4.0x in 2016 to 1.6x in 2020.70 The temporary increase in the combined firm's debt-to-EBITDA ratio and the decline in its credit rating were due to the fact that CP would borrow funds to pay for the entire cash portion of the merger consideration. CP's "Sweetened" Offer On December 16, CP sweetened its revised offer to include 0.451 units of a CVR in addition to the $32.86 in cash and 0.451 CP shares for each NS share it had offered on December 8. The CVR would expire in October 2017 (18 months after the transaction closed at the end of April 2016 and approximately two months before it expected to receive the final regulatory decision), and would be listed on a major exchange (eg, the NYSE). At maturity, each CVR would receive a cash payment equal to $175 minus the CP-NS share price at maturity up to a maximum cash payment of $25.71.72 To determine the value of the CVR, CP used data on current market interest rates (see Exhibit 11). assumed annual stock price volatility for the combined entity of 25%, and assumed that no dividends would be paid between the closing of the transaction and the expiration of the CVR794 Because the CVR would be highly liquid, NS shareholders could choose to hold the security to maturity or sell it after the transaction closed. Ackman said: [T]hink about this as a long-life insurance policy on the trading price.... It protects you on a downside case....CP believes that the market will value this (combined) company-the way it's run by Hunter-at a meaningfully higher price and that the CVR ultimately will require no payout by CP. So it's the way you put your money where your mouth is.... Canadian Pacific is basically ... saying we're willing to bet $3.4 billion that this stock is above $175 a share in 2017)." Conclusion With a live offer to acquire the firm on the table, Squires had to respond. Before he could respond, however, he and his advisors had to determine how much the sweetened" offer was worth- particularly given the addition of the CVR-and make a recommendation to the NS board members on whether to accept or reject the offer. If they were going to reject the offer the board had to consider what NS might do next given how quickly it had responded to the prior rejection. If, on the other hand, they accepted the offer, they had to consider whether the merger would receive regulatory approval from the STB and what might happen if it did not. Squires needed to prepare answers to the full range of questions the board members were certain to ask concerning the offer, its value, and the ramifications of accepting the deal. Time was short and he had a lot to do. Exhibit1 Class I Railroad Operating and Financial Performance Metrics ($ millions) BNSF Railway Canadian National Railway Canadian Pacific Railway CSX Corp Kansas City Southern Norfolk Southern Corp Union Pacific Corp Operating Statistics (2014) Miles of Track Operated (miles) Number of Employees (number) Carloads Originated (thousands) Revenue Ton Miles (RTM) (billions) (1) 32,643 46,240 9,322 771 19,600 24,635 5,625 232 12,559 14,698 2,684 150 20,769 28,123 5,190 3,339 3,038 443 34 19,759 29,482 5,137 205 31,974 49,652 7,771 550 245 Productivity Measures (2014) Revenue per RTM (cents) Revenue per Employee (5000) Carloads Origin.per Employee Employees per Billion RTM Million RTM per Mile of Track $2.99 $498 202 60 24 $4.51 $425 228 106 12 $3.81 $389 183 98 12 $5.03 $439 185 115 12 $4.02 $447 146 90 10 $5.67 $394 174 $4.36 $483 157 90 17 144 10 Financial Statistics (9/30/15) Operating Revenues Operating Expenses Operating Income Operating Ratio (%) $22,452 $14,832 $7,620 66.1% $10,126 $5.997 $4, 129 59 2% $5,434 $3310 $2,124 60.9% $12,222 $8.482 $3,740 69.4% $2,463 $1,655 $808 672% $10,863 $7.730 $3,133 71.2% $22,758 $14 251 $8.507 82.6% EBITDA Net Income Return on Sales (ROS) Return on Equity (ROE) $7,620 $6,218 27.7% 17.8% $5,047 $2,747 27.1% 25.4% $2,586 $1,196 22.0% 40.1% $4,926 $1,993 16.3% 17.1% $1,086 $485 19.7% 11.6% $4,140 $1,706 15.7% 14.1% $10,491 $5,086 22.3% 24.7% Cash Assets Debt Equity (book value) Debt-to-Total Cap (book) $3,040 $81,503 $21,882 $34,897 38.5% $401 $26,742 $7,828 $10,800 42.0% $493 $13,759 $6,477 $2,980 68.5% $966 $34,015 $10,106 $11,660 46.4% $117 $8,323 $2,345 $4,184 35.9% $433 $33,527 $9,496 $12, 129 43.9% $1,078 $53,763 $13,319 $20,599 39.3% Equity (market value) Stock Price (5) Shares Outstanding (basic) Avg. Leverage (2 year, market) Avg. Leverage (5 year, market) n/a n/a n/a n/a n/a $46,324 $58.46 792.4 12.9% 15.4% $23,115 $143.57 161.0 15.2% 22.4% $26,225 $26.90 974.9 24.1% 27.5% $9,915 $90.88 109.1 16.OK 16.6% $23,027 $76.40 3014 24.2% 26.1% $75,652 $88.41 855.7 11.6N 13.3N 8.7 12.5 7.7 BBB+ 7.0 888 10.6 BBB BBB 5.9 888 14.2 Interest coverage S&P Credit Rating Equity Beta (vs. S&P 500) Two year weekly Five year monthly Ticker n/a n/a private 1.15 1.04 CNI 1.28 1.31 CP 1.14 1.29 CSX 1.30 1.24 KSU 1.14 1.13 NSC 115 1.02 UNP Exhibit 2 Major Railroad Acquisitions and Transaction Multiples, 1995-2014 Total Enterprise Value EBITDA Acquirer Target Year 9x 8x Burlington Northern Union Pacific Union Pacific Norfolk Southern & CSX Canadian National Canadian National Canadian National Canadian Pacific Berkshire Hathaway Sante Fe Pacific Chicago Northwestern Southern Pacific Conrail Illinois Central Wisconsin Central BC Rail DM&E BNSF 1995 1995 1996 1997 1998 2001 2004 2008 2010 14x 14x 10x 10x 9x 13x 9x Average 10.7x Exhibit 3 Norfolk Southern Income Statements, 2011-2015 ($ millions) Years Ended December 31 2011 2012 2013 2014 LTM (1) Sep 2015 $11,172 $11,040 $11,245 $11,624 $10,863 Operating Revenue Operating Expenses Compensation & benefits Materials, services, and other Fuel Depreciation & amortization Total Operating Expense $2,974 $2,960 $2,534/ $2,463 $1,589 $1,577 $862 $916 $7,959 $7,916 $3,002 $2,457 $1,613 $916 $7,988 $2,897 $2,627 $1,574 $951 $8,049 $2,923 $2,713 $1,087 $1,007 $7,730 Operating Income Interest expense Unusual items Profit before tax Income tax expense Net Income $3,213 $455 $160 $2,918 $1,002 $1,916 $3,124 $495 $129 $2,758 $1,009 $1,749 $3,257 $525 $233 $2,965 $1,055 $1,910 $3,575 $545 $104 $3,134 $1,134 $2,000 $3,133 $532 $107 $2,708 $1,002 $1,706 Per Share Items Basic Earnings per share Dividends per share $5.52 $1.66 $5.42 $1.94 $6.1 $2.04 $6.44 $2.22 $5.59 $2.34 Cash Flow Items Capital Expenditures $2,160 $2,241 $1,971 $2,118 $2,516 Financial Ratios and Information Revenue Growth Rate [2] Operating Ratio Effective Tax Rate Return on Sales (ROS) Number of employees 17.4% 71.2% 34.3% 17.2% 30,329 -1.2% 71.7% 36.6% 15.8% 30,943 1.9% 71.0% 35.6% 17.0% 30, 103 3.4% 69.2% 36.2% 17.2% 29,482 -6.6% 71.2% 37.0% 15.7% 30,456 Exhibit 6 Norfolk Southern Projections on a Stand-alone Basis, October 2015 (5 millions) Est. Projected (period ending 12/31) 2017 2018 2019 2020 2015 2016 2021 $10,649 Income statement items Revenue Growth rate (%) Operating expenses Depreciation (1) EBIT $11,671 4.4% $6,548 $1,049 $3,052 $10,698 0.5% $6,397 $1,091 $3,210 $11,175 4.5% $6,570 $1,135 $3,470 $6,808 $1,180 $3,683 $12,191 $12,557 4.5% 3.0% $7,049 $7,139 $1,227 $1,300 $3,915 $4,118 $12,871 2.5% $7,440 $1,313 $4,118 Operating ratio 71% 70% 69% 68% 68% 67% 68% Balance sheet items Capital expenditures Net working capital (2) $2,365 ($192) $2,070 ($128) $1,910 ($134) $1,930 ($140) $1,930 ($146) $1,949 ($151) $1,969 ($154) Exhibit 7 Canadian Pacific Railway Income Statements, 2011-2015 ($ millions) Years Ended December 31 2011 2012 2013 LTM (1) 2014 Sep 2015 $5,092 $5,714 $5,773 $5,716 $5,434 Operating Revenue Operating Expenses Compensation & benefits Materials, services, and other Fuel Depreciation & amortization Total Operating Expense $1,403 / $1,479 $1,304 $1,421 $952 $1,002 $482 $541 $4,141 $4,443 $1,297 $1,253 $945 $532 $4,027 $1,164 $1,151 $905 $477 $3,697 $1,079 $1,125 $643 $463 $3,310 Operating Income Interest expense Unusual items Profit before tax Income tax expense Net Income $951 $248 ($18) $686 $125 $561 $1,271 $277 ($356) $638 $153 $485 $1,746 $262 ($426) $1,059 $235 $824 $2,020 $244 ($16) $1,760 $485 $1,274 $2,124 $274 ($141) $1,708 $512 $1,196 Per Share Items Basic Earnings per share Dividends per share $3.31 $1.15 $2.83 $1.35 $4.71 $1.32 $7.37 $1.21 $7.27 $1.12 Cash Flow Items Capital Expenditures $1,086 $1,152 $1,163 $1,251 $1,210 Financial Ratios and Information Revenue Growth Rate [2] Operating Ratio Effective Tax Rate Return on Sales (ROS) Number of employees 1.7% 81.3% 18.2% 11.0% 14,169 12.2% 77.8% 23.9% 8.5% 14,594 1.0% 69.8% 22.2% 14.3% 14,977 - 1.0% 64.7% 27.6% 22.3% 14,698 -8.7% 60.9% 30.0% 22.0% 14,698 Exhibit 8 Canadian Pacific Railway Balance Sheets, 2011-2015 (5 millions) Years Ended December 31 2011 2012 2013 2014 Sept 2015 Assets Cash and ST investments Accounts receiveable Inventory Other current assets Total current assets Net PP&E Investments Other LT Assets Total assets $46 $510 $136 $151 $842 $12,544 $164 $330 $13,880 $334 $548 $136 $315 $1,333 $13,055 $83 $303 $14,775 $448 $546 $155 $761 $1,910 $12,545 $87 $1,483 $16,024 $195 $606 $153 $100 $1,054 $12,467 $97 $673 $14,291 $493 $539 $130 $110 $1,273 $11,766 $107 $612 $13,759 Liabilities and stock holders' equi Accounts payable Short-term debt Current maturities of LT debt Other current liabilities Total current liabilities Long-term debt Other liabilities Deferred income taxes Total Liabilities Sharholders equity Total liabilities & equity 0.0% $381 $27 $49 $733 $1,190 $4,618 $1,709 $1,789 $9,307 $4,573 $13,880 0.0% $322 $0 $54 $858 $1,234 $4,651 $1,677 $2,099 $9,661 $5,114 $14,775 0.0% $337 $0 $178 $782 $1,297 $4,377 $937 $2,733 $9,343 $6,680 $16,024 0.0% $351 $0 $116 $752 $1,218 $4,857 $1,025 $2,346 $9,447 $4,844 $14,291 0.0% $271 $0 $22 $914 $1,206 $6,456 $826 $2,291 $10,779 $2.980 $13,759 Financial Ratios & Other Information Current Ratio Debt-to-Total Capital S&P Long-term Debt Rating Shares outstanding Stock price per share 0.71 50.7% BBB- 170.4 67.67 1.08 47.9% BBB- 174.2 10162 1.47 40.5% BBB- 175.2 151.32 0.87 50.7% BBB+ 171.0 192.69 1.06 68.5% BBB 161.0 143.57 Canadian Pacific's Bid for Norfolk Southern Formed in 1982 out of railroads that had been in existence for 100 years, Norfolk Southern Corporation (NS) had a proud history as one of the largest and most efficient railroads in the United States. Despite this legacy, both revenues and profits began falling in 2015 as shipments of coal (20% of revenues) and other commodities declined and cost reduction efforts stalled. As a result, the company's stock price had fallen by almost 40% from a high of $117 in late 2014 to a low of $72 in August 2015 Rumors that Canadian Pacific Railway Limited (CP) wanted to acquire Norfolk Southern began circulating in the market in early November 2015.1 Canadian Pacific did, in fact, make an offer to acquire NS on November 17, which the company acknowledged in a press release later that day (note: all amounts in this case refer to U.S. dollars): Norfolk Southern Corporation ("the Company") today confirmed that it has received an unsolicited, low-premium, non-binding, highly conditional indication of interest from Canadian Pacific to acquire the Company for $46.72 in cash and a fixed exchange ratio of 0.348 Canadian Pacific shares per Norfolk Southern share, representing a premium of less than 10% based on closing prices today.... Notably, any consolidation among Class I railroads in North America would face significant regulatory hurdles. Two weeks later, Norfolk Southern's board of directors unanimously rejected the offer, stating: After a comprehensive review ... the Norfolk Southern board concluded that the indication of interest is grossly inadequate, creates substantial regulatory risks and uncertainties that are highly unlikely to overcome, and is not in the best interest of the Company and its shareholders.... We believe that Canadian Pacific's short-term, cut-to- the-bone strategy could cause Norfolk Southern to lose substantial revenues from our service-sensitive customer base. We also believe the proposed transaction risks harm to vital transportation infrastructure and the communities we serve. In addition to rejecting CP's offer, James Squires, Norfolk Southern's CEO, announced a new strategic plan designed to improve the company's long-term performance by reducing its operating ratio (defined as operating expenses divided by operating revenues-- it was an industry measure of cost efficiency). Squires argued that Norfolk Southern could, on a stand-alone basis, reduce its operating ratio from over 70% to below 65% by 2020 through aggressive cost reduction and, in doing so, generate double-digit earnings per share (EPS) growth Within days of the rejection, Canadian Pacific announced a revised offer and proposed a novel deal structure that would allow operational improvements at Norfolk Southern to be implemented even before the merger received regulatory approval. To further sweeten the deal, CP added a new security known as a Contingent Value Right (CVR) several days later. This security, which CP described as a "long-term insurance policy," was designed to protect investors if the share price of the combined entity fell below a certain level for any reason before the regulators approved the merger. By including the CVR in the deal, CP was demonstrating confidence in its ability to achieve the projected merger benefits. Before Squires and the NS board could respond to CP's "sweetened" offer, however, they had to review the offer with their financial and legal advisors, understand how the merger would affect the firm's operations and impact its shareholders, and prepare a response justifying their decision. That response would not only determine the firm's prospects for many years to come, but could affect Squires's professional reputation and career prospects, as well. The U.S. Railroad Industry The U.S. railroad industry had a long history of regulation starting with the establishment of the Interstate Commerce Commission (ICC) in 1887. ICC mandates and other federal regulation limited what railroads could charge on interstate routes, where they could construct new infrastructure, and whether they could divest rail lines. After growing for years, total rail mileage peaked in 1916 as the federal government began subsidizing highway construction? As trucking became an increasingly important form of competition, the share of intercity freight carried by trains fell steadily through the 1950s and 1960s. The 1970s was an especially difficult decade for railroads as inflation caused costs to rise (eg, fuel, labor, and equipment), yet regulations prevented railroads from raising rates commensurately. The end result was falling returns--the average return on investment (ROI) during the 1970s was 2%-and bankruptcies: Penn Central, a Class I railroad, declared bankruptcy in 1970, the largest U.S. corporate bankruptcy at that time. 10 The Staggers Rail Act of 1980 provided much needed relief to U.S. railroads, giving them the flexibility to set their own rates, abandon low-density routes, and make acquisitions with limited scrutiny. In the following years, a flurry of mergers intended to improve service, efficiency, and safety reduced the number of Class I railroads from 56 to 7.12 In this new consolidated environment, railroads regained financial stability as they streamlined operations and cut costs. For example, employment at Class 1 railroads fell from 458,000 people in 1980 to 178,000 people in 1998; and the industry's average operating ratio fell from 93% to 85%.1 With higher profitability, the average ROI grew to 7% in the 1990s and then to 9.4% by mid-2015.** (Exhibit 1 provides operating and financial statistics for the major railroads operating in the US and Canada as of 2015) Two important changes occurred in the 1990s. First, the Surface Transportation Board (STB) replaced the ICC as the primary regulator in 1996, and gained the ability to regulate all mergers and acquisitions. Second, the rapid consolidation of Class I railroads continued: Burlington Northern acquired Santa Fe Pacific in 1995 after an intense bidding war with Union Pacific, Union Pacific then acquired Southern Pacific in 1995;" CSX acquired Conrail in 1996 and agreed to split the railroad with Norfolk Southern as a solution to an escalating bidding war;" and finally, Canadian National acquired Illinois Central in 1998." (Exhibit 2 shows data on railroad acquisitions from 1995-2014.) Rather than enhancing service and improving efficiency as promised, these mergers often disrupted service, increased costs and prices), and reduced safety, at least in the short term, which prompted heightened regulatory scrutiny 2 For example, after BNSF and Canadian National agreed to merge in December 1999, the STB blocked the merger and froze all major rail mergers for 16 months, beginning in March 2000. According to the STB,"the shipping public has not yet fully recovered from the service interruptions associated with the previous round of mergers (from 1995 to 1998). "2 The next year, the STB established rules forbidding all railroad mergers unless they were in the public interest, as it tried to create a stable, balanced, and reliable rail transportation system."23 Under the new rules, companies had to demonstrate that merging with another railroad would boost competition and maintain service quality. 2 An STB spokesman said, "Although our new rules and policy statement do not, as the Class I railroads argue, reflect an anti-merger bias, we do plan to take a more skeptical 'show me' attitude toward claims of merger benefits and toward claims that no transitional problems would occur." At the time, the prevailing view was that another round of consolidation could leave the continent with just two Class I railroads.* Norfolk Southern Corporation Norfolk Southern Corporation (NS or NSC) was formed in 1982 by the merger of two railways: Norfolk & Westem and Southern Railway. As the fourth-largest Class I railroad operating in North America, NS had 30,456 employees, controlled 20,000 miles of track in 22 eastern states, and served all of the major East Coast ports. The company generated $20 billion of income on operating revenues of $11.6 billion in 2014. (Exhibits 3 and 4 show NS's income statements and balance sheets, respectively.) By early 2015, revenues and profits were falling and the firm's relative cost position was deteriorating. After being in the middle of the pack of Class I railroads in terms of its operating ratio, NS was at the high end of the group as of 2015. (Exhibit 5 shows operating ratios over time for Class I railroads). Analysts, however, expected the firm's performance would improve in the coming years. (Exhibit 6 shows financial projections for NS on a stand-alone basis according to equity analysts at UBS in October 2015.) Squires became CEO of NS on June 1, 2015, at the age of 53. When former CEO Charles "Wick Moorman announced his successor, he said, "I am confident that the company is poised for continued growth, success, and shareholder value creation." Squires had joined the company in 1992, as a newly minted graduate of the University of Chicago Law School. He rose through the ranks of the legal division before being named senior vice president of financial planning in 2006, CFO in 2007 and then president in 2013, Canadian Pacific Railway Limited Canadian Pacific Railway Ltd. was founded in the late 19 century to connect the major cities in eastern Canada with the less populous western territories. By 1986, CP had become Canada's second- largest company. Headquartered in Calgary, Alberta, CP had 13.700 employees and operated 12,500 miles of track in Canada as well as the midwestern and northeastern parts of the United States CP's main competitors were Canadian National Railway Company (Canadian National) in Canada and BNSF Railway in the U.S. Midwest. With revenues of $5.7 billion and net income of $1.3 billion in 2014, CP was considerably smaller than NS.3 (Exhibits 7 and 8 show CP's income statements and balance sheets, respectively.) In 2011, hedge-fund manager and activist investor William Bill" Ackman (HBS 1992) acquired a 12% stake in CP through his firm Pershing Square Capital Management. Ackman was known in the financial world for his overwhelming confidence and his willingness to place enormous bets based on his convictions. For example, he told one author: "I don't care what other people think. I invest based on what I believe the opportunity for profit is compared with my estimate of the potential for loss. ** Ackman subsequently forced CP's CEO to resign, ousted the company's board of directors, and installed Hunter Harrison as chief executive after a proxy fight.1 Harrison, a long-term railroad executive, had retired as the CEO of Canadian National (CN) in 2009.2 During his time at CN, Harrison had won various awards, including Canadian CEO of the Year and Railroader of the Year 44 Harrison believed consolidation was a good way to add critical rail capacity and simultaneously improve efficiency. Toward that end, he had unsuccessfully approached CSX Corp, another Class I railroad located in the eastern United States, in 2014 about a possible merger, arguing, "A pro- competition, customer-friendly, safety-focused railway combination is one such solution that could not be ignored on its merits by regulators." Yet NS's then CEO Moorman said in 2014 that major railroad mergers would be "highly problematic" from both a regulatory and a service perspective Absent mergers, careful cost control could also improve efficiency. In fact, under Harrison's leadership, CP's operating ratio had fallen from 81% in 2011 to close to 60% in 2015. In response, the firm's share price during his tenure had soared from less than $68 at the end of 2011 to almost $215 in October 2014, yet had fallen back down to 5135 as of early November 2015." (CP was traded on both the Toronto and New York stock exchanges.) Bidding for Norfolk Southern Despite market rumors of a possible bid for NS by CP, CP denied the rumors in a press release on November 9, claiming: "[There is no material news pending at this time. CP does not comment on market rumor and speculation."" Nevertheless, NS's stock price increased 11.0% (from $79.87 to $88.62) and CP's price increased 5.9% (from $134.31 to $142.18) on a day the market was down 10%. Eight days later, after the market closed on November 17, 2015, CP did, in fact, make an offer for NS: Canadian Pacific (CP)... has sent an offer letter to Norfolk Southern Corp. (NS) proposing a business combination ... The proposal, which includes a sizable premium in cash and stock offered to NS shareholders, would result in a company with the potential for faster earnings growth than either CP or NS could achieve on their own, all the while maintaining a strong investment grade credit rating.So NS confirmed that it had received an offer from CP to acquire the firm's shares for $46.72 in cash and a fixed exchange ratio of 0.348 CP shares for each NS share. Based on closing stock prices that day, reporters estimated the offer was worth $94.95 per NS share (-$46.72 in cash +0.348 * $138.58), which represented an acquisition premium of 9% over NS's closing price of $86.97. The next day, after the market incorporated the news of the proposed acquisition, NS's share price increased 6.3% to $92.49, while CP's price increased 5.4% to $146.65.9 NS responded by saying that in addition to facing significant regulatory hurdles," the offer was deficient, with a premium of less than 10% over the previous day's closing share price of $86.97 CP responded by noting that there had been a significant run-up in NS's share price due to market rumors of the impending bid, and that its offer should be compared to an "unaffected" share price that did not include the effect of the potential merger. In addition, CP argued that the merger would result in significant improvements in operating performance and synergies that should explicitly be recognized when valuing the offer 55 On December 4, 2015, the NS board of directors rejected the CP offer, stating that it was "grossly inadequate."** CEO Squires said: There is a high probability that, after years of disruption and expense, the proposed combination would be rejected by the Surface Transportation Board.... Even if the proposed combination were ultimately to be cleared, it would be subject to a wide range of onerous conditions that would reduce the value of the stock consideration that has been proposed. Canadian Pacific quickly revised its offer to $32.86 in cash and 0.451 CP shares for each NS share (ie, less cash and more stock) on December 8.5* During a conference call that day, Harrison and Ackman gave formal presentations about the proposed merger and took questions from analysts regarding the merits of the proposed combination. A vocal advocate for the merger, Ackman dismissed the NS board's resistance to the deal as similar to the resistance that followed his efforts to install Harrison as CEO of CP in 2012. "I've seen this movie before," he said." Following the second conference call about the deal on December 16, NS and CP closed at $89.79 and $128.56, respectively. (Exhibits 9a and 9b show stock prices for CP and NS from October 1 through December 18.) The Merger Rationale According to CP, the merger provided an opportunity to create a 21 century railroad for a 21- century economy."60 Although additional rail capacity was desperately needed to meet the demands of a growing economy, it was becoming increasingly difficult to add rail infrastructure in urban areas where most customers were located and railroads exchanged freight with trucks. CP argued that industry consolidation offered the best opportunity to improve efficiency and add incremental capacity without requiring additional infrastructure. Importantly, consolidation would also improve service for shippers. Nowhere was the need for additional infrastructure more crucial than in Chicago, Illinois. In 2014, close to 25% of U.S. rail traffic passed through Chicago, and the volume of traffic was expected to double over the next 10 years. Despite various attempts to add infrastructure, the problem was only getting worse. CP argued that the CP-NS merger offered the best opportunity to increase capacity in the critical Chicago train yards: Consolidation enables far better utilization of existing infrastructure. For example, trains interchanged in Chicago today must be broken apart and rebuilt in yards within the city and then delivered to receiving carriers. The process involves multiple interchanges between multiple carriers in multiple yards. A merger would allow these activities to be performed elsewhere so that trains moving through Chicago can move smoothly through the city without exiting the mainline... A merger would allow CP- NS to provide end-to-end service to customers, without hand-offs and interchanges Reducing these disruptive activities can significantly improve velocity, lower costs, and enable the combined company to move goods more quickly without increasing rates In addition to improving efficiency, CP argued that a CP-NS merger would not reduce competition because the two networks met "end-to-end" rather than serving overlapping geographies. (Exhibit 10 shows the combined CP-NS rail network.) However, to address potential regulatory concerns, CP proposed that the new company would give shippers the choice of where they could connect with another railroad along its network, ending the industry practice of "bottleneck pricing" (ie, monopoly pricing on routes served by a single railroad) and would allow competing railroads to access its railway if the new company was not providing appropriate service or competitive rates in a particular location. Finally, CP also identified significant opportunities to improve operating efficiencies on the NS system, thereby creating additional value 65 According to the plan, CP anticipated that the transaction would close by the end of April 2016, and the STB would render a decision to approve (or not) the merger by December 2017. From May 2016 to December 2017, CP and NS would be merged into a "voting trust" holding company that would allow the two companies to operate independently. Newly created shares in this holding company (CP-NS shares) would begin trading immediately. Notably, however, CP proposed that Harrison would immediately resign from CP-severing all ties, including his pension and any stock holdings -and would become CEO of NS. This meant that Harrison could immediately start implementing the planned operational improvements at NS, independent of the STB's ultimate decision. If the STB ultimately rejected the merger, then the "improved" Norfolk Southern would be spun off, leaving the companies to operate independently. On the other hand, if the STB ultimately approved the merger, then the combined entity would start realizing CP's projected "post-merger combination synergies." CP argued that this novel structure was vital to the transaction, as 72% of its projected operational efficiencies were from pre-merger operational improvements.66 Table A Projected Merger Benefits ($ millions) 2016 2017 2018 2019 2020 2021 Pre-Merger Operational Improvements Phase-in (%) Increase in EBIT 42% 17% $214 $529 67% $844 92% $1,159 100% $1,260 100% $1,260 Post-Merger Combination Synergies Phase-In (%) Increase in EBIT 25% 0% $0 0% $0 $124 50% $248 75% $371 100% $495 Projected Total Increase in CP-NS EBIT $214 $529 $968 $1,407 $1,631 $1,755 synergies resulting from the merger. The cash flows were on a pre-tax basis and were net of merger- related costs and restructuring expenses. The $1.26 billion of pre-merger operational improvements included improvements in fuel efficiency ($100 million), train productivity ($610 million), and labor productivity ($550 million). The $495 million of post-merger combination synergies included both revenue and cost synergies ($225 million and $270 million, respectively). CP assumed a tax rate of 36% for income earned by NS. CP argued that its assumed tax rate was conservative because, if the STB approved the merger, the overall tax rate of the combined entity could be somewhat lower. These tax savings --expected to be approximately $200 million annually starting in 2018-were not included in the projections of pre-merger operating improvements and post-merger combination synergies shown in Table A. Finally, CP's CFO Mark Erceg stated that the combined company would initially have a BBB/Baa credit rating (Standard & Poor's/Moody's). However, because of the combined company's strong ability to generate cash flow, he anticipated that its credit rating would rise to BBB+/Baat by 2017, and its debt-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio would fall from 4.0x in 2016 to 1.6x in 2020.70 The temporary increase in the combined firm's debt-to-EBITDA ratio and the decline in its credit rating were due to the fact that CP would borrow funds to pay for the entire cash portion of the merger consideration. CP's "Sweetened" Offer On December 16, CP sweetened its revised offer to include 0.451 units of a CVR in addition to the $32.86 in cash and 0.451 CP shares for each NS share it had offered on December 8. The CVR would expire in October 2017 (18 months after the transaction closed at the end of April 2016 and approximately two months before it expected to receive the final regulatory decision), and would be listed on a major exchange (eg, the NYSE). At maturity, each CVR would receive a cash payment equal to $175 minus the CP-NS share price at maturity up to a maximum cash payment of $25.71.72 To determine the value of the CVR, CP used data on current market interest rates (see Exhibit 11). assumed annual stock price volatility for the combined entity of 25%, and assumed that no dividends would be paid between the closing of the transaction and the expiration of the CVR794 Because the CVR would be highly liquid, NS shareholders could choose to hold the security to maturity or sell it after the transaction closed. Ackman said: [T]hink about this as a long-life insurance policy on the trading price.... It protects you on a downside case....CP believes that the market will value this (combined) company-the way it's run by Hunter-at a meaningfully higher price and that the CVR ultimately will require no payout by CP. So it's the way you put your money where your mouth is.... Canadian Pacific is basically ... saying we're willing to bet $3.4 billion that this stock is above $175 a share in 2017)." Conclusion With a live offer to acquire the firm on the table, Squires had to respond. Before he could respond, however, he and his advisors had to determine how much the sweetened" offer was worth- particularly given the addition of the CVR-and make a recommendation to the NS board members on whether to accept or reject the offer. If they were going to reject the offer the board had to consider what NS might do next given how quickly it had responded to the prior rejection. If, on the other hand, they accepted the offer, they had to consider whether the merger would receive regulatory approval from the STB and what might happen if it did not. Squires needed to prepare answers to the full range of questions the board members were certain to ask concerning the offer, its value, and the ramifications of accepting the deal. Time was short and he had a lot to do. Exhibit1 Class I Railroad Operating and Financial Performance Metrics ($ millions) BNSF Railway Canadian National Railway Canadian Pacific Railway CSX Corp Kansas City Southern Norfolk Southern Corp Union Pacific Corp Operating Statistics (2014) Miles of Track Operated (miles) Number of Employees (number) Carloads Originated (thousands) Revenue Ton Miles (RTM) (billions) (1) 32,643 46,240 9,322 771 19,600 24,635 5,625 232 12,559 14,698 2,684 150 20,769 28,123 5,190 3,339 3,038 443 34 19,759 29,482 5,137 205 31,974 49,652 7,771 550 245 Productivity Measures (2014) Revenue per RTM (cents) Revenue per Employee (5000) Carloads Origin.per Employee Employees per Billion RTM Million RTM per Mile of Track $2.99 $498 202 60 24 $4.51 $425 228 106 12 $3.81 $389 183 98 12 $5.03 $439 185 115 12 $4.02 $447 146 90 10 $5.67 $394 174 $4.36 $483 157 90 17 144 10 Financial Statistics (9/30/15) Operating Revenues Operating Expenses Operating Income Operating Ratio (%) $22,452 $14,832 $7,620 66.1% $10,126 $5.997 $4, 129 59 2% $5,434 $3310 $2,124 60.9% $12,222 $8.482 $3,740 69.4% $2,463 $1,655 $808 672% $10,863 $7.730 $3,133 71.2% $22,758 $14 251 $8.507 82.6% EBITDA Net Income Return on Sales (ROS) Return on Equity (ROE) $7,620 $6,218 27.7% 17.8% $5,047 $2,747 27.1% 25.4% $2,586 $1,196 22.0% 40.1% $4,926 $1,993 16.3% 17.1% $1,086 $485 19.7% 11.6% $4,140 $1,706 15.7% 14.1% $10,491 $5,086 22.3% 24.7% Cash Assets Debt Equity (book value) Debt-to-Total Cap (book) $3,040 $81,503 $21,882 $34,897 38.5% $401 $26,742 $7,828 $10,800 42.0% $493 $13,759 $6,477 $2,980 68.5% $966 $34,015 $10,106 $11,660 46.4% $117 $8,323 $2,345 $4,184 35.9% $433 $33,527 $9,496 $12, 129 43.9% $1,078 $53,763 $13,319 $20,599 39.3% Equity (market value) Stock Price (5) Shares Outstanding (basic) Avg. Leverage (2 year, market) Avg. Leverage (5 year, market) n/a n/a n/a n/a n/a $46,324 $58.46 792.4 12.9% 15.4% $23,115 $143.57 161.0 15.2% 22.4% $26,225 $26.90 974.9 24.1% 27.5% $9,915 $90.88 109.1 16.OK 16.6% $23,027 $76.40 3014 24.2% 26.1% $75,652 $88.41 855.7 11.6N 13.3N 8.7 12.5 7.7 BBB+ 7.0 888 10.6 BBB BBB 5.9 888 14.2 Interest coverage S&P Credit Rating Equity Beta (vs. S&P 500) Two year weekly Five year monthly Ticker n/a n/a private 1.15 1.04 CNI 1.28 1.31 CP 1.14 1.29 CSX 1.30 1.24 KSU 1.14 1.13 NSC 115 1.02 UNP Exhibit 2 Major Railroad Acquisitions and Transaction Multiples, 1995-2014 Total Enterprise Value EBITDA Acquirer Target Year 9x 8x Burlington Northern Union Pacific Union Pacific Norfolk Southern & CSX Canadian National Canadian National Canadian National Canadian Pacific Berkshire Hathaway Sante Fe Pacific Chicago Northwestern Southern Pacific Conrail Illinois Central Wisconsin Central BC Rail DM&E BNSF 1995 1995 1996 1997 1998 2001 2004 2008 2010 14x 14x 10x 10x 9x 13x 9x Average 10.7x Exhibit 3 Norfolk Southern Income Statements, 2011-2015 ($ millions) Years Ended December 31 2011 2012 2013 2014 LTM (1) Sep 2015 $11,172 $11,040 $11,245 $11,624 $10,863 Operating Revenue Operating Expenses Compensation & benefits Materials, services, and other Fuel Depreciation & amortization Total Operating Expense $2,974 $2,960 $2,534/ $2,463 $1,589 $1,577 $862 $916 $7,959 $7,916 $3,002 $2,457 $1,613 $916 $7,988 $2,897 $2,627 $1,574 $951 $8,049 $2,923 $2,713 $1,087 $1,007 $7,730 Operating Income Interest expense Unusual items Profit before tax Income tax expense Net Income $3,213 $455 $160 $2,918 $1,002 $1,916 $3,124 $495 $129 $2,758 $1,009 $1,749 $3,257 $525 $233 $2,965 $1,055 $1,910 $3,575 $545 $104 $3,134 $1,134 $2,000 $3,133 $532 $107 $2,708 $1,002 $1,706 Per Share Items Basic Earnings per share Dividends per share $5.52 $1.66 $5.42 $1.94 $6.1 $2.04 $6.44 $2.22 $5.59 $2.34 Cash Flow Items Capital Expenditures $2,160 $2,241 $1,971 $2,118 $2,516 Financial Ratios and Information Revenue Growth Rate [2] Operating Ratio Effective Tax Rate Return on Sales (ROS) Number of employees 17.4% 71.2% 34.3% 17.2% 30,329 -1.2% 71.7% 36.6% 15.8% 30,943 1.9% 71.0% 35.6% 17.0% 30, 103 3.4% 69.2% 36.2% 17.2% 29,482 -6.6% 71.2% 37.0% 15.7% 30,456 Exhibit 6 Norfolk Southern Projections on a Stand-alone Basis, October 2015 (5 millions) Est. Projected (period ending 12/31) 2017 2018 2019 2020 2015 2016 2021 $10,649 Income statement items Revenue Growth rate (%) Operating expenses Depreciation (1) EBIT $11,671 4.4% $6,548 $1,049 $3,052 $10,698 0.5% $6,397 $1,091 $3,210 $11,175 4.5% $6,570 $1,135 $3,470 $6,808 $1,180 $3,683 $12,191 $12,557 4.5% 3.0% $7,049 $7,139 $1,227 $1,300 $3,915 $4,118 $12,871 2.5% $7,440 $1,313 $4,118 Operating ratio 71% 70% 69% 68% 68% 67% 68% Balance sheet items Capital expenditures Net working capital (2) $2,365 ($192) $2,070 ($128) $1,910 ($134) $1,930 ($140) $1,930 ($146) $1,949 ($151) $1,969 ($154) Exhibit 7 Canadian Pacific Railway Income Statements, 2011-2015 ($ millions) Years Ended December 31 2011 2012 2013 LTM (1) 2014 Sep 2015 $5,092 $5,714 $5,773 $5,716 $5,434 Operating Revenue Operating Expenses Compensation & benefits Materials, services, and other Fuel Depreciation & amortization Total Operating Expense $1,403 / $1,479 $1,304 $1,421 $952 $1,002 $482 $541 $4,141 $4,443 $1,297 $1,253 $945 $532 $4,027 $1,164 $1,151 $905 $477 $3,697 $1,079 $1,125 $643 $463 $3,310 Operating Income Interest expense Unusual items Profit before tax Income tax expense Net Income $951 $248 ($18) $686 $125 $561 $1,271 $277 ($356) $638 $153 $485 $1,746 $262 ($426) $1,059 $235 $824 $2,020 $244 ($16) $1,760 $485 $1,274 $2,124 $274 ($141) $1,708 $512 $1,196 Per Share Items Basic Earnings per share Dividends per share $3.31 $1.15 $2.83 $1.35 $4.71 $1.32 $7.37 $1.21 $7.27 $1.12 Cash Flow Items Capital Expenditures $1,086 $1,152 $1,163 $1,251 $1,210 Financial Ratios and Information Revenue Growth Rate [2] Operating Ratio Effective Tax Rate Return on Sales (ROS) Number of employees 1.7% 81.3% 18.2% 11.0% 14,169 12.2% 77.8% 23.9% 8.5% 14,594 1.0% 69.8% 22.2% 14.3% 14,977 - 1.0% 64.7% 27.6% 22.3% 14,698 -8.7% 60.9% 30.0% 22.0% 14,698 Exhibit 8 Canadian Pacific Railway Balance Sheets, 2011-2015 (5 millions) Years Ended December 31 2011 2012 2013 2014 Sept 2015 Assets Cash and ST investments Accounts receiveable Inventory Other current assets Total current assets Net PP&E Investments Other LT Assets Total assets $46 $510 $136 $151 $842 $12,544 $164 $330 $13,880 $334 $548 $136 $315 $1,333 $13,055 $83 $303 $14,775 $448 $546 $155 $761 $1,910 $12,545 $87 $1,483 $16,024 $195 $606 $153 $100 $1,054 $12,467 $97 $673 $14,291 $493 $539 $130 $110 $1,273 $11,766 $107 $612 $13,759 Liabilities and stock holders' equi Accounts payable Short-term debt Current maturities of LT debt Other current liabilities Total current liabilities Long-term debt Other liabilities Deferred income taxes Total Liabilities Sharholders equity Total liabilities & equity 0.0% $381 $27 $49 $733 $1,190 $4,618 $1,709 $1,789 $9,307 $4,573 $13,880 0.0% $322 $0 $54 $858 $1,234 $4,651 $1,677 $2,099 $9,661 $5,114 $14,775 0.0% $337 $0 $178 $782 $1,297 $4,377 $937 $2,733 $9,343 $6,680 $16,024 0.0% $351 $0 $116 $752 $1,218 $4,857 $1,025 $2,346 $9,447 $4,844 $14,291 0.0% $271 $0 $22 $914 $1,206 $6,456 $826 $2,291 $10,779 $2.980 $13,759 Financial Ratios & Other Information Current Ratio Debt-to-Total Capital S&P Long-term Debt Rating Shares outstanding Stock price per share 0.71 50.7% BBB- 170.4 67.67 1.08 47.9% BBB- 174.2 10162 1.47 40.5% BBB- 175.2 151.32 0.87 50.7% BBB+ 171.0 192.69 1.06 68.5% BBB 161.0 143.57