Answered step by step

Verified Expert Solution

Question

1 Approved Answer

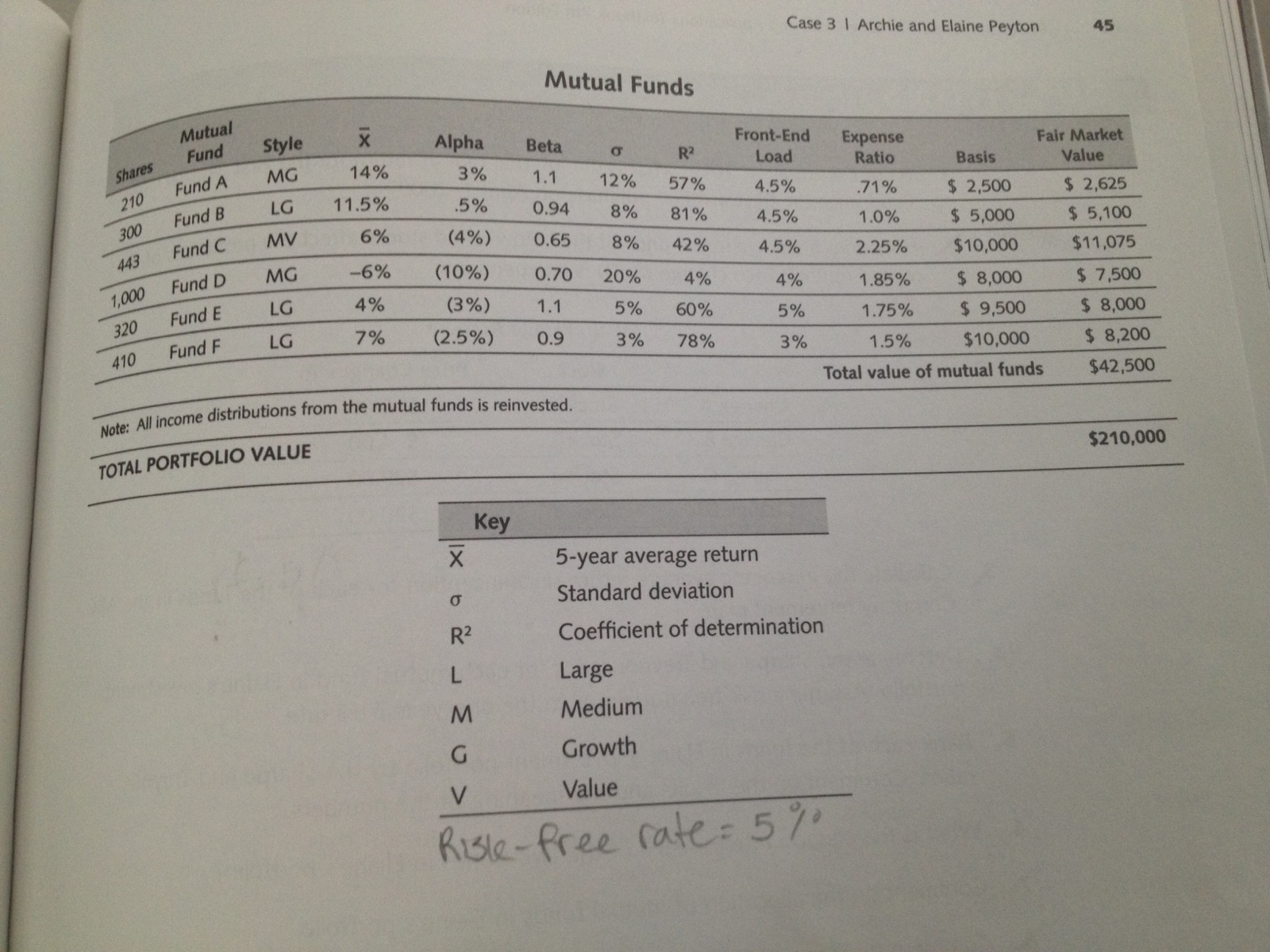

1. Determine the Sharpe and Treynor ratios for each mutual fund in Elaine's investment portfolio. The risk-free rate is 5% and the T-bill rate is

1. Determine the Sharpe and Treynor ratios for each mutual fund in Elaine's investment portfolio. The risk-free rate is 5% and the T-bill rate is also 5%.

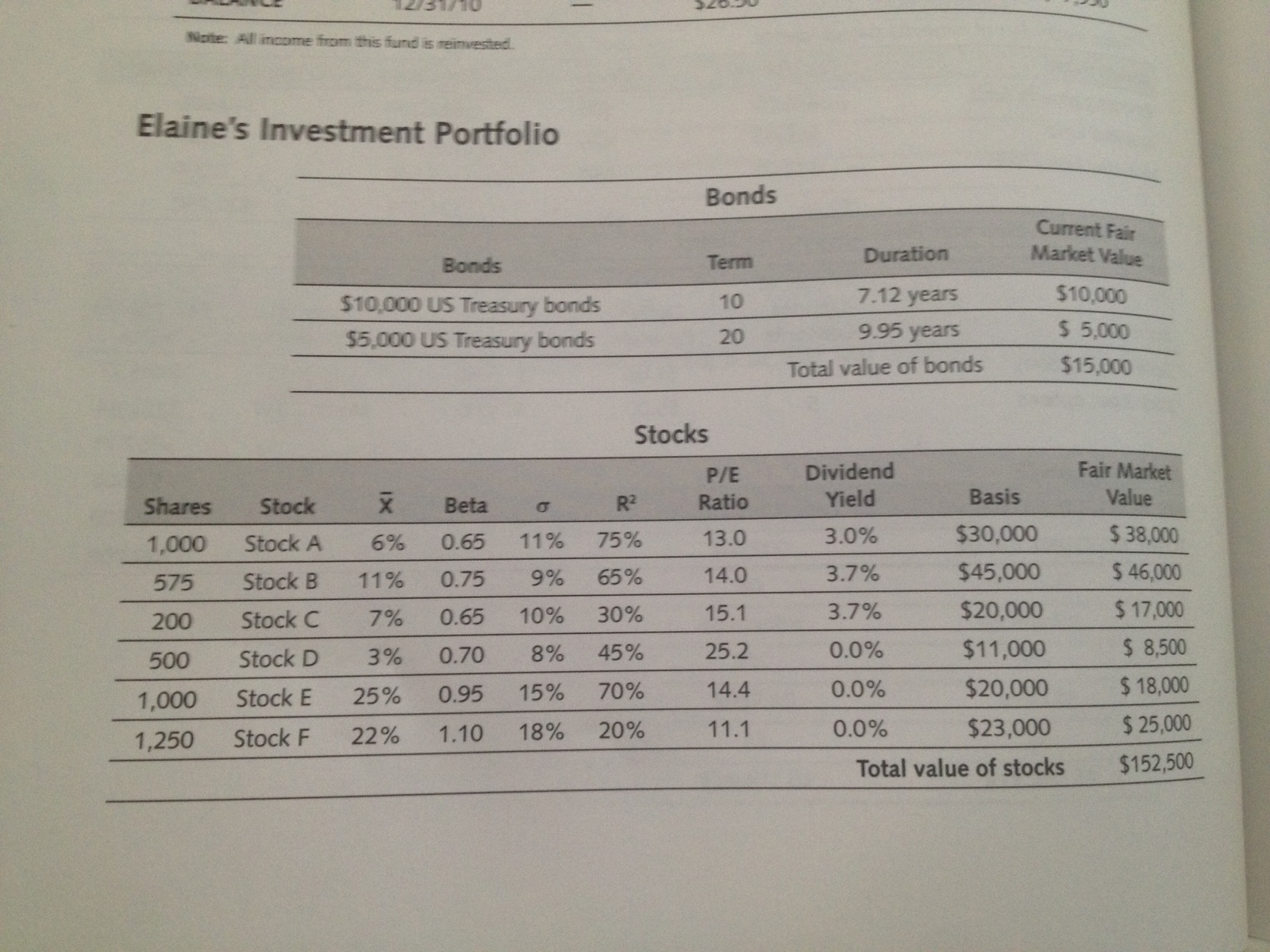

2. What is the coupon rate for each of the two bonds in Elaine's portfolio?

3. What is the weighted duration for the bond portfolio portion of Elaine's investment portfolio?

4. What is the holding period return (HPR) for Elaine's stock portfolio portion held in her investment portfolio?

Note: All income from this fund is reinvested Elaine's Investment Portfolio Bonds Current Fair Duration Market Value $10,000 US Treasury bonds $5,000 US Treasury bonds 7.12 years $10,000 9.95 years S 5,000 Total value of bonds $15,000 Stocks PIE Dividend Shares Stock Beta Ratio Yield Basis Fair Market Value 1,000 Stock A 6% 0.65 11 % 75% 13.0 3.0% $30,000 $38,000 575 Stock B 11% 0.75 9% 65% 14.0 3.7% $45,000 $ 46000 200 Stock C70.65 10% 30% 15.1 3.7% $20,000 $ 17,000 500 Stock D 3% 0.70 8% 45% 25.2 0.0% $11,000 $ 8,500 1,000 Stock E25% 0.95 15% 70% 14.4 0.0% $20,000 $ 18,000 1,250 Stock F 22% 1.10 18% 20% 11.1 0.0% $23,000 $ 25,000 Total value of stocks $152500

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started