Question

1. Evaluate Joanna Cohens estimation of cost of capital: a. Is it appropriate to use a single cost of capital for all Nikes businesses? Explain.

1. Evaluate Joanna Cohens estimation of cost of capital:

a. Is it appropriate to use a single cost of capital for all Nikes businesses? Explain.

b. How does Joanna Cohen calculate the weights for debt and equity? Do you agree with these calculations? Why? (If you do not agree, show your calculations)

c. How does she calculate cost of debt? Do you agree with these calculations? Why? (If you do not agree, show your calculations)

d. How does she calculate cost of equity? Do you agree with these calculations? Why? (If you do not agree, show your calculations)

2. Calculate cost of equity using Dividend Discount Model. Is it appropriate to use this model for Nike? Explain.

3. What is your estimate for Nikes cost of capital (i.e., calculate WACC)? Do you recommend an investment in Nike stock? Why?

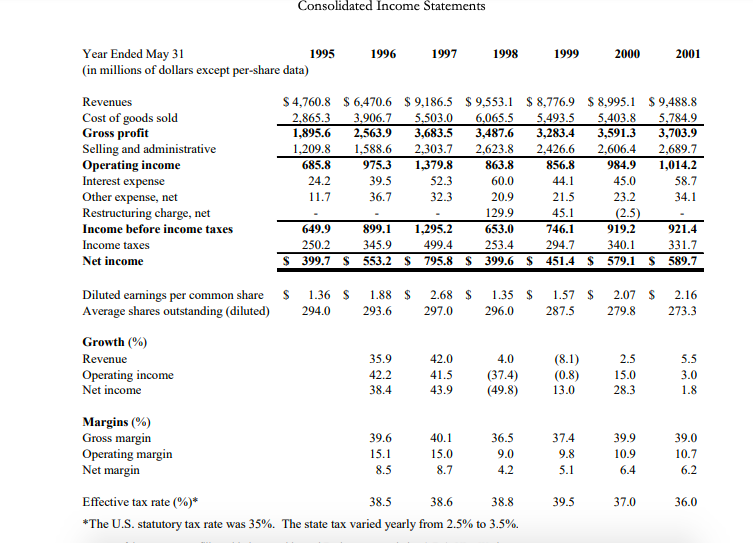

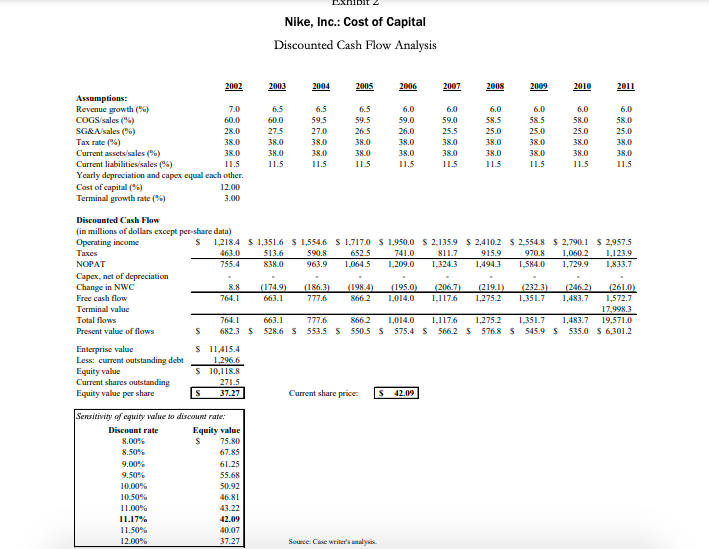

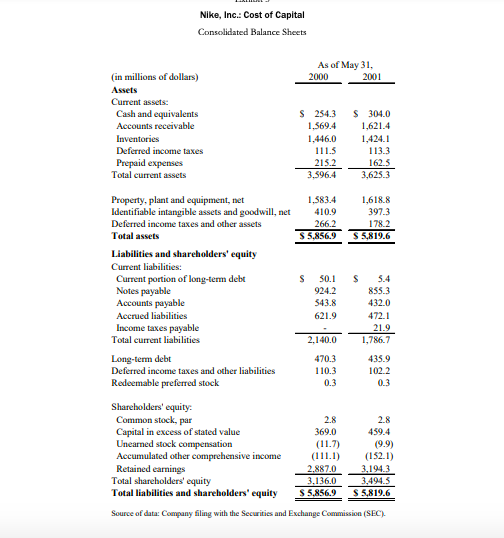

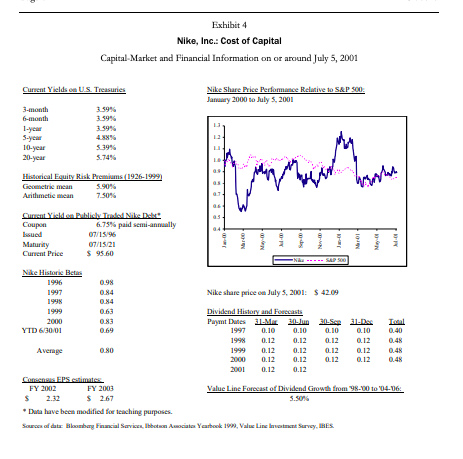

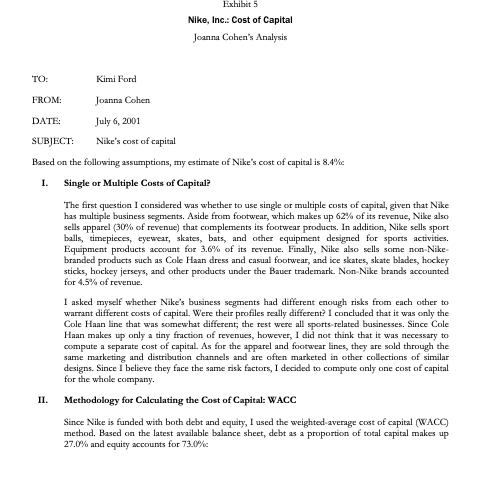

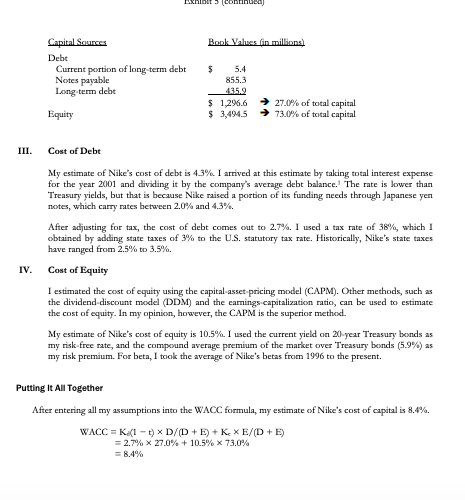

On July 5, 2001, Kimi Ford, a portfolio manager at NorthPoint Group, a mutual fund management firm, pored over analysts' write-ups of Nike, Inc., the athletic-shoe manufacturer. Nike's share price had declined significantly from the beginning of the year. Ford was considering buying some shares for the fund she managed, the NorthPoint Large-Cap Fund, which invested mostly in Fortune 500 companies, with an emphasis on value investing. Its top holdings included ExxonMobil, General Motors, McDonald's, 3M, and other large-cap, generally old-economy stocks. Although the stock market had declined over the last 18 months, the North Point Large-Cap Fund had performed extremely well. In 2000, the fund earned a return of 20.7%, even as the S&P 500 fell 10.1%. At the end of June 2001, the fund's year-to-date returns stood at 6.4% versus - 7.3% for the S&P 500. Only a week earlier, on June 28, 2001, Nike had held an analysts' meeting to disclose its fiscal-year 2001 results.? The meeting, however, had another purpose: Nike management wanted to communicate a strategy for revitalizing the company. Since 1997, its revenues had plateaued at around $9 billion, while net income had fallen from almost $800 million to $580 million (see Exhibit 1). Nike's market share in U.S. athletic shoes had fallen from 48%, in 1997, to 42% in 2000.2 In addition, recent supply-chain issues and the adverse effect of a strong dollar had negatively affected revenue. At the meeting, management revealed plans to address both top-line growth and operating performance. To boost revenue, the company would develop more athletic-shoe products in the mid-priced segmenta segment that Nike had overlooked in recent years. Nike also planned to push its apparel line, which, under the recent leadership of industry veteran Mindy Grossman,' had performed extremely well. On the cost side, Nike would exert more effort on expense control. Finally, company executives reiterated their long-term revenue-growth targets of 8% to 10% and earnings-growth targets of above 15%. Analysts' reactions were mixed. Some thought the financial targets were too aggressive; others saw significant growth opportunities in apparel and in Nike's international businesses. Ford read all the analysts' reports that she could find about the June 28 meeting, but the reports gave her no clear guidance: a Lehman Brothers report recommended a strong buy, while UBS Warburg and CSFB analysts expressed misgivings about the company and recommended a hold. Ford decided instead to develop her own discounted cash flow forecast to come to a clearer conclusion. Page 2 UV0010 Her forecast showed that, at a discount rate of 12%, Nike was overvalued at its current share price of $42.09 (Exhibit 2). She had done a quick sensitivity analysis, however, which revealed Nike was undervalued at discount rates below 11.17%. Because she was about to go into a meeting, she asked her new assistant, Joanna Cohen, to estimate Nike's cost of capital. Cohen immediately gathered all the data she thought she might need (Exhibit 1 through Exhibit 4) and began to work on her analysis. At the end of the day, Cohen submitted her cost-of-capital estimate and a memo (Exhibit 5) explaining her assumptions to Ford. Consolidated Income Statements 1996 1997 1998 1999 2000 2001 Year Ended May 31 1995 (in millions of dollars except per-share data) Revenues Cost of goods sold Gross profit Selling and administrative Operating income Interest expense Other expense, net Restructuring charge, net Income before income taxes Income taxes Net income $ 4,760.8 $ 6,470.6 $ 9,186.5 $ 9,553.1 $ 8,776.9 $8,995.1 $ 9,488.8 2.865.3 3,906.7 5,503.0 6,065.5 5,493.5 5,403.8 5,784.9 1,895.6 2,563.9 3,683.5 3,487.6 3,283.4 3,591.3 3,703.9 1,209.8 1,588,6 2,303.7 2,623.8 2,426.6 2,606.4 2,689.7 685.8 975.3 1,379.8 863.8 856.8 984.9 1,014.2 24.2 39.5 52.3 60.0 44.1 45.0 58.7 11.7 36.7 32.3 20.9 21.5 23.2 34.1 129.9 45.1 (2.5) 649.9 899.1 1,295.2 653.0 746.1 919.2 921.4 250.2 345.9 499.4 253.4 294.7 340.1 331.7 $ 399.7 $ 553.2 $ 795.8 $ 399.6 $ 451.4 $ 579.1 S 589.7 1.36 $ 294.0 1.88 $ 293.6 2.68 $ 297.0 1.35 $ 296.0 1.57 $ 287.5 2.07 $ 279.8 2.16 273.3 Diluted earnings per common share $ Average shares outstanding (diluted) Growth (%) Revenue Operating income Net income 2.5 5.5 35.9 42.2 38.4 42.0 41.5 4.0 (37.4) (49.8) (8.1) (0.8) 3.0 43.9 13.0 15.0 28.3 1.8 Margins (%) Gross margin Operating margin Net margin 39.6 15.1 8.5 40.1 15.0 8.7 36.5 9.0 4.2 37.4 9.8 5.1 39.9 10.9 6.4 39.0 10.7 6.2 38.5 38.6 39.5 37.0 36.0 Effective tax rate (%)* 38.8 *The U.S. statutory tax rate was 35%. The state tax varied yearly from 2.5% to 3.5%. Nike, Inc.: Cost of Capital Discounted Cash Flow Analysis 2003 2004 2005 2006 2007 2008 2009 2010 2011 2002 Assumptions: Revenue growth (%) 7.0 COGS/sales (%) 60.0 SG&A/sales (%) 28.0 Tax rate (%) 38.0 Current assets/sales (%) 38.0 Current liabilities/sales (%) 11.5 Yearly depreciation and capex equal each other. Cost of capital (9) 12.00 Terminal growth rate (%) 3.00 6.5 60.0 27.5 38.0 38.0 11.5 6.5 59.5 27.0 38.0 6.5 59.5 26,5 38.0 38.0 11.5 6.0 59,0 26.0 38.0 38.0 6.0 59.0 25.5 38.0 38.0 11.5 6.0 58.5 25.0 38.0 380 11.5 6.0 58.5 25.0 38.0 38.0 11.5 6.0 58.0 25.0 38.0 38.0 11.5 6.0 58.0 25.0 38.0 38.0 11.5 38.0 11.5 11.5 Taxes Discounted Cash Flow (in millions of dollars except per-share data) Operating income S 1,218.4 $ 1.351.6 $ 1,554.6 S 1,717,0 $ 1,950.0 S 2,135.9 $ 2.410.2 $ 2.554.8 $ 2,790.1 $ 2,957.5 4610 513.6 590.8 652.5 741.0 811.7 915.9 970.8 1,060.2 1,123,9 NOPAT 755.4 838.0 963.9 1,064.5 1,209.0 1.324.3 1.494.3 1.584.0 1,729.9 1,833.7 Capex, net of depreciation Change in NWC 8.8 (174.9) (186.3) (1984) (1950) (206.7) (219.1) (2323) (246.2) (261.0) Free cash flow 764.1 663.1 777.6 866.2 1,014.0 1.117.6 1.275.2 1.351.7 1,483.7 1,572.7 Terminal value 17,998,3 Total flows 764.1 663.1 777.6 866.2 1,014.0 1.1176 1.275.2 1.351.7 1.483.7 19,571.0 Present value of flows S 682.3 $ 528.6 $ 553.5 S 550.5 S 575.4 5 566.2 $ 576.8 $ 545.9 $ 535.0 $ 6,301.2 Enterprise value S 11,415.4 Less: current outstanding debt 1.296.6 Equity value S 10,118.8 Current shares outstanding 271.5 Equity value per share S 37.27 Current share price S 42.09 Sensitivity of equity value to discount rate: Discount rate Equity value 8.00% S 75.80 8.50% 67.85 9.00% 61.25 9.50% 55.68 10.00% 50.92 10.50% 46.81 11.00% 43.22 11.17% 42.09 11.50% 40.07 12.00% 37.27 Source: Case writer's analyse Nike, Inc.: Cost of Capital Consolidated Balance Sheets As of May 31, 2000 2001 (in millions of dollars) Assets Current assets: Cash and equivalents Accounts receivable Inventories Deferred income taxes Prepaid expenses Total current assets s 254.3 1.569.4 1.446.0 111.5 215.2 3.596.4 $ 304.0 1,621.4 1,424.1 113.3 162.5 3,625 3 1.583.4 410.9 266.2 $5.856.9 1,618.8 397.3 178.2 S 5,819.6 S s Property, plant and equipment, net Identifiable intangible assets and goodwill, net Deferred income taxes and other assets Total assets Liabilities and shareholders' equity Current liabilities: Current portion of long-term debt Notes payable Accounts payable Accrued liabilities Income taxes payable Total current liabilities Long-term debt Deferred income taxes and other liabilities Redeemable preferred stock 30.1 924.2 543.8 621.9 5.4 855.3 432.0 472.1 21.9 1,786.7 2.140.0 470.3 110.3 0.3 435.9 102.2 0.3 Shareholders' equity: Common stock, par Capital in excess of stated value Unearned stock compensation Accumulated other comprehensive income Retained earnings Total shareholders' equity Total liabilities and shareholders' equity 2.8 369.0 (11.7) (111.1) 2.887.0 3,136,0 $5.856.9 2.8 459.4 (9.9) (152.1) 3.194.3 3,494.5 S 5,819.6 Source of data: Company filing with the Securities and Exchange Commission (SEC) Exhibit 4 Nike, Inc.: Cost of Capital Capital Market and Financial Information on or around July 5, 2001 Nike Share Price Performance Relative to S&P 500 January 2000 to July , 2001 Current Yields on US. Treasures 3-month 3.59% 6-month 3.59% 3.59% 5-year 10-year 5.39% 20-year 5.74% 13 LE 04 Mr. My. Historical Equity Risk Premiums (1926-1999) Geometric mean 5.90% Arithmetic mean 7.50% Current Yield Publicly Timed Nike Delet Coupon 6.75% paid semi-annually Issued 07/15196 Maturity 07/15/21 Current Price $ 95.60 Nike Historie Betas 1996 0.98 1997 0.84 Nike share price on July 5, 2001: $42.09 1998 0.84 0.63 Dividend History and Forecasts 2000 0.83 Paymt Dutes 31 ME 30- 30-Sep 31-Dec YTD 6/30/01 1997 0.10 0.10 0.10 1994 0.12 0.12 0.12 0.48 Average 0.80 0.12 0.12 0.12 0.12 0.48 0.12 0.12 0.12 0.48 0.12 0.12 Comen EPS timates FY 2002 FY 2003 Value Line Forecast of Dividend Growth from 98-00 to '04-06 $ $ 2.67 5.50% Duta have been modified for teaching purposes. Sarcal data: Blomberg Financial Services, Ibodae Amacial Yearbook 19. Valu Lint Survey, IBES 0.10 0.12 Exhibit 5 Nike, Inc.: Cost of Capital Joanna Cohen's Analysis TO: Kimi Ford FROM: Joanna Cohen DATE: July 6, 2001 SUBJECT: Nike's cost of capital Based on the following assumptions, my estimate of Nike's cost of capital is 8.4% I. Single or Multiple Costs of Capital? The first question I considered was whether to use single or multiple costs of capital, given that Nike has multiple business segments. Aside from footwear, which makes up 62% of its revenue, Nike also sells apparel (50% of revenue) that complements its footwear products. In addition, Nike sells sport balls, timepieces, eyewear, skates, bats, and other equipment designed for sports activities. Equipment products account for 3.6% of its revenue. Finally, Nike also sells some non-Nike- branded products such as Cole Haan dress and casual footwear, and ice skates, skate blades, hockey sticks, hockey jerseys, and other products under the Bauer trademark. Non-Nike brands accounted for 4.5% of revenue. I asked myself whether Nike's business segments had different enough risks from each other to warrant different costs of capital. Were their profiles really different? I concluded that it was only the Cole Haan line that was somewhat different; the rest were all sports-related businesses. Since Cole Haan makes up only a tiny fraction of revenues, however, I did not think that it was necessary to compute a separate cost of capital. As for the apparel and footwear lines, they are sold through the same marketing and distribution channels and are often marketed in other collections of similar designs. Since I believe they face the same risk factors, I decided to compute only one cost of capital for the whole company. II. Methodology for Calculating the Cost of Capital: WACC Since Nike is funded with both debt and equity, I used the weighted average cost of capital (WACC) method. Based on the latest available balance sheet, debt as a proportion of total capital makes up 27.0% and equity accounts for 73.0% Book Values in millions) Capital Sources Debt Current portion of long term debt Notes payable Long term debt $ 5.4 855.3 48.5.2 $ 1,296.6 $ 3,494.5 27.0% of total capital 73.0% of total capital Equity III. Cost of Debt My estimate of Nike's cost of debt is 43%. I arrived at this estimate by taking total interest expense for the year 2001 and dividing it by the company's average debt balance. The rate is lower than Treasury yields, but that is because Nike raised a portion of its funding needs through Japanese yen notes, which carry rates between 2.0% and 4.3%. After adjusting for tax, the cost of debt comes out to 2.7%. I used a tax rate of 38%, which I obtained by adding state taxes of 3% to the U.S. statutory tax rate. Historically, Nike's state taxes have ranged from 2.5% to 3.5%. Cost of Equity I estimated the cost of equity using the capital-asset pricing model (CAPM). Other methods, such as the dividend discount model (DDM) and the earnings-capitalization ratio, can be used to estimate the cost of equity. In my opinion, however, the CAPM is the superior method. My estimate of Nike's cost of equity is 10.5%. I used the current yield on 20-year Treasury bonds as my risk-free rate, and the compound average premium of the market over Treasury bonds (5.9%) as my risk premium. For beta, I took the average of Nike's betas from 1996 to the present. IV. Putting It All Together After entering all my assumptions into the WACC formula, my estimate of Nike's cost of capital is 8.9%. WACC = K (1 t) * D/D + E) + K XE/(D+E) = 2.7% X 27.0% + 10.5% x 73.0% = 8.4% On July 5, 2001, Kimi Ford, a portfolio manager at NorthPoint Group, a mutual fund management firm, pored over analysts' write-ups of Nike, Inc., the athletic-shoe manufacturer. Nike's share price had declined significantly from the beginning of the year. Ford was considering buying some shares for the fund she managed, the NorthPoint Large-Cap Fund, which invested mostly in Fortune 500 companies, with an emphasis on value investing. Its top holdings included ExxonMobil, General Motors, McDonald's, 3M, and other large-cap, generally old-economy stocks. Although the stock market had declined over the last 18 months, the North Point Large-Cap Fund had performed extremely well. In 2000, the fund earned a return of 20.7%, even as the S&P 500 fell 10.1%. At the end of June 2001, the fund's year-to-date returns stood at 6.4% versus - 7.3% for the S&P 500. Only a week earlier, on June 28, 2001, Nike had held an analysts' meeting to disclose its fiscal-year 2001 results.? The meeting, however, had another purpose: Nike management wanted to communicate a strategy for revitalizing the company. Since 1997, its revenues had plateaued at around $9 billion, while net income had fallen from almost $800 million to $580 million (see Exhibit 1). Nike's market share in U.S. athletic shoes had fallen from 48%, in 1997, to 42% in 2000.2 In addition, recent supply-chain issues and the adverse effect of a strong dollar had negatively affected revenue. At the meeting, management revealed plans to address both top-line growth and operating performance. To boost revenue, the company would develop more athletic-shoe products in the mid-priced segmenta segment that Nike had overlooked in recent years. Nike also planned to push its apparel line, which, under the recent leadership of industry veteran Mindy Grossman,' had performed extremely well. On the cost side, Nike would exert more effort on expense control. Finally, company executives reiterated their long-term revenue-growth targets of 8% to 10% and earnings-growth targets of above 15%. Analysts' reactions were mixed. Some thought the financial targets were too aggressive; others saw significant growth opportunities in apparel and in Nike's international businesses. Ford read all the analysts' reports that she could find about the June 28 meeting, but the reports gave her no clear guidance: a Lehman Brothers report recommended a strong buy, while UBS Warburg and CSFB analysts expressed misgivings about the company and recommended a hold. Ford decided instead to develop her own discounted cash flow forecast to come to a clearer conclusion. Page 2 UV0010 Her forecast showed that, at a discount rate of 12%, Nike was overvalued at its current share price of $42.09 (Exhibit 2). She had done a quick sensitivity analysis, however, which revealed Nike was undervalued at discount rates below 11.17%. Because she was about to go into a meeting, she asked her new assistant, Joanna Cohen, to estimate Nike's cost of capital. Cohen immediately gathered all the data she thought she might need (Exhibit 1 through Exhibit 4) and began to work on her analysis. At the end of the day, Cohen submitted her cost-of-capital estimate and a memo (Exhibit 5) explaining her assumptions to Ford. Consolidated Income Statements 1996 1997 1998 1999 2000 2001 Year Ended May 31 1995 (in millions of dollars except per-share data) Revenues Cost of goods sold Gross profit Selling and administrative Operating income Interest expense Other expense, net Restructuring charge, net Income before income taxes Income taxes Net income $ 4,760.8 $ 6,470.6 $ 9,186.5 $ 9,553.1 $ 8,776.9 $8,995.1 $ 9,488.8 2.865.3 3,906.7 5,503.0 6,065.5 5,493.5 5,403.8 5,784.9 1,895.6 2,563.9 3,683.5 3,487.6 3,283.4 3,591.3 3,703.9 1,209.8 1,588,6 2,303.7 2,623.8 2,426.6 2,606.4 2,689.7 685.8 975.3 1,379.8 863.8 856.8 984.9 1,014.2 24.2 39.5 52.3 60.0 44.1 45.0 58.7 11.7 36.7 32.3 20.9 21.5 23.2 34.1 129.9 45.1 (2.5) 649.9 899.1 1,295.2 653.0 746.1 919.2 921.4 250.2 345.9 499.4 253.4 294.7 340.1 331.7 $ 399.7 $ 553.2 $ 795.8 $ 399.6 $ 451.4 $ 579.1 S 589.7 1.36 $ 294.0 1.88 $ 293.6 2.68 $ 297.0 1.35 $ 296.0 1.57 $ 287.5 2.07 $ 279.8 2.16 273.3 Diluted earnings per common share $ Average shares outstanding (diluted) Growth (%) Revenue Operating income Net income 2.5 5.5 35.9 42.2 38.4 42.0 41.5 4.0 (37.4) (49.8) (8.1) (0.8) 3.0 43.9 13.0 15.0 28.3 1.8 Margins (%) Gross margin Operating margin Net margin 39.6 15.1 8.5 40.1 15.0 8.7 36.5 9.0 4.2 37.4 9.8 5.1 39.9 10.9 6.4 39.0 10.7 6.2 38.5 38.6 39.5 37.0 36.0 Effective tax rate (%)* 38.8 *The U.S. statutory tax rate was 35%. The state tax varied yearly from 2.5% to 3.5%. Nike, Inc.: Cost of Capital Discounted Cash Flow Analysis 2003 2004 2005 2006 2007 2008 2009 2010 2011 2002 Assumptions: Revenue growth (%) 7.0 COGS/sales (%) 60.0 SG&A/sales (%) 28.0 Tax rate (%) 38.0 Current assets/sales (%) 38.0 Current liabilities/sales (%) 11.5 Yearly depreciation and capex equal each other. Cost of capital (9) 12.00 Terminal growth rate (%) 3.00 6.5 60.0 27.5 38.0 38.0 11.5 6.5 59.5 27.0 38.0 6.5 59.5 26,5 38.0 38.0 11.5 6.0 59,0 26.0 38.0 38.0 6.0 59.0 25.5 38.0 38.0 11.5 6.0 58.5 25.0 38.0 380 11.5 6.0 58.5 25.0 38.0 38.0 11.5 6.0 58.0 25.0 38.0 38.0 11.5 6.0 58.0 25.0 38.0 38.0 11.5 38.0 11.5 11.5 Taxes Discounted Cash Flow (in millions of dollars except per-share data) Operating income S 1,218.4 $ 1.351.6 $ 1,554.6 S 1,717,0 $ 1,950.0 S 2,135.9 $ 2.410.2 $ 2.554.8 $ 2,790.1 $ 2,957.5 4610 513.6 590.8 652.5 741.0 811.7 915.9 970.8 1,060.2 1,123,9 NOPAT 755.4 838.0 963.9 1,064.5 1,209.0 1.324.3 1.494.3 1.584.0 1,729.9 1,833.7 Capex, net of depreciation Change in NWC 8.8 (174.9) (186.3) (1984) (1950) (206.7) (219.1) (2323) (246.2) (261.0) Free cash flow 764.1 663.1 777.6 866.2 1,014.0 1.117.6 1.275.2 1.351.7 1,483.7 1,572.7 Terminal value 17,998,3 Total flows 764.1 663.1 777.6 866.2 1,014.0 1.1176 1.275.2 1.351.7 1.483.7 19,571.0 Present value of flows S 682.3 $ 528.6 $ 553.5 S 550.5 S 575.4 5 566.2 $ 576.8 $ 545.9 $ 535.0 $ 6,301.2 Enterprise value S 11,415.4 Less: current outstanding debt 1.296.6 Equity value S 10,118.8 Current shares outstanding 271.5 Equity value per share S 37.27 Current share price S 42.09 Sensitivity of equity value to discount rate: Discount rate Equity value 8.00% S 75.80 8.50% 67.85 9.00% 61.25 9.50% 55.68 10.00% 50.92 10.50% 46.81 11.00% 43.22 11.17% 42.09 11.50% 40.07 12.00% 37.27 Source: Case writer's analyse Nike, Inc.: Cost of Capital Consolidated Balance Sheets As of May 31, 2000 2001 (in millions of dollars) Assets Current assets: Cash and equivalents Accounts receivable Inventories Deferred income taxes Prepaid expenses Total current assets s 254.3 1.569.4 1.446.0 111.5 215.2 3.596.4 $ 304.0 1,621.4 1,424.1 113.3 162.5 3,625 3 1.583.4 410.9 266.2 $5.856.9 1,618.8 397.3 178.2 S 5,819.6 S s Property, plant and equipment, net Identifiable intangible assets and goodwill, net Deferred income taxes and other assets Total assets Liabilities and shareholders' equity Current liabilities: Current portion of long-term debt Notes payable Accounts payable Accrued liabilities Income taxes payable Total current liabilities Long-term debt Deferred income taxes and other liabilities Redeemable preferred stock 30.1 924.2 543.8 621.9 5.4 855.3 432.0 472.1 21.9 1,786.7 2.140.0 470.3 110.3 0.3 435.9 102.2 0.3 Shareholders' equity: Common stock, par Capital in excess of stated value Unearned stock compensation Accumulated other comprehensive income Retained earnings Total shareholders' equity Total liabilities and shareholders' equity 2.8 369.0 (11.7) (111.1) 2.887.0 3,136,0 $5.856.9 2.8 459.4 (9.9) (152.1) 3.194.3 3,494.5 S 5,819.6 Source of data: Company filing with the Securities and Exchange Commission (SEC) Exhibit 4 Nike, Inc.: Cost of Capital Capital Market and Financial Information on or around July 5, 2001 Nike Share Price Performance Relative to S&P 500 January 2000 to July , 2001 Current Yields on US. Treasures 3-month 3.59% 6-month 3.59% 3.59% 5-year 10-year 5.39% 20-year 5.74% 13 LE 04 Mr. My. Historical Equity Risk Premiums (1926-1999) Geometric mean 5.90% Arithmetic mean 7.50% Current Yield Publicly Timed Nike Delet Coupon 6.75% paid semi-annually Issued 07/15196 Maturity 07/15/21 Current Price $ 95.60 Nike Historie Betas 1996 0.98 1997 0.84 Nike share price on July 5, 2001: $42.09 1998 0.84 0.63 Dividend History and Forecasts 2000 0.83 Paymt Dutes 31 ME 30- 30-Sep 31-Dec YTD 6/30/01 1997 0.10 0.10 0.10 1994 0.12 0.12 0.12 0.48 Average 0.80 0.12 0.12 0.12 0.12 0.48 0.12 0.12 0.12 0.48 0.12 0.12 Comen EPS timates FY 2002 FY 2003 Value Line Forecast of Dividend Growth from 98-00 to '04-06 $ $ 2.67 5.50% Duta have been modified for teaching purposes. Sarcal data: Blomberg Financial Services, Ibodae Amacial Yearbook 19. Valu Lint Survey, IBES 0.10 0.12 Exhibit 5 Nike, Inc.: Cost of Capital Joanna Cohen's Analysis TO: Kimi Ford FROM: Joanna Cohen DATE: July 6, 2001 SUBJECT: Nike's cost of capital Based on the following assumptions, my estimate of Nike's cost of capital is 8.4% I. Single or Multiple Costs of Capital? The first question I considered was whether to use single or multiple costs of capital, given that Nike has multiple business segments. Aside from footwear, which makes up 62% of its revenue, Nike also sells apparel (50% of revenue) that complements its footwear products. In addition, Nike sells sport balls, timepieces, eyewear, skates, bats, and other equipment designed for sports activities. Equipment products account for 3.6% of its revenue. Finally, Nike also sells some non-Nike- branded products such as Cole Haan dress and casual footwear, and ice skates, skate blades, hockey sticks, hockey jerseys, and other products under the Bauer trademark. Non-Nike brands accounted for 4.5% of revenue. I asked myself whether Nike's business segments had different enough risks from each other to warrant different costs of capital. Were their profiles really different? I concluded that it was only the Cole Haan line that was somewhat different; the rest were all sports-related businesses. Since Cole Haan makes up only a tiny fraction of revenues, however, I did not think that it was necessary to compute a separate cost of capital. As for the apparel and footwear lines, they are sold through the same marketing and distribution channels and are often marketed in other collections of similar designs. Since I believe they face the same risk factors, I decided to compute only one cost of capital for the whole company. II. Methodology for Calculating the Cost of Capital: WACC Since Nike is funded with both debt and equity, I used the weighted average cost of capital (WACC) method. Based on the latest available balance sheet, debt as a proportion of total capital makes up 27.0% and equity accounts for 73.0% Book Values in millions) Capital Sources Debt Current portion of long term debt Notes payable Long term debt $ 5.4 855.3 48.5.2 $ 1,296.6 $ 3,494.5 27.0% of total capital 73.0% of total capital Equity III. Cost of Debt My estimate of Nike's cost of debt is 43%. I arrived at this estimate by taking total interest expense for the year 2001 and dividing it by the company's average debt balance. The rate is lower than Treasury yields, but that is because Nike raised a portion of its funding needs through Japanese yen notes, which carry rates between 2.0% and 4.3%. After adjusting for tax, the cost of debt comes out to 2.7%. I used a tax rate of 38%, which I obtained by adding state taxes of 3% to the U.S. statutory tax rate. Historically, Nike's state taxes have ranged from 2.5% to 3.5%. Cost of Equity I estimated the cost of equity using the capital-asset pricing model (CAPM). Other methods, such as the dividend discount model (DDM) and the earnings-capitalization ratio, can be used to estimate the cost of equity. In my opinion, however, the CAPM is the superior method. My estimate of Nike's cost of equity is 10.5%. I used the current yield on 20-year Treasury bonds as my risk-free rate, and the compound average premium of the market over Treasury bonds (5.9%) as my risk premium. For beta, I took the average of Nike's betas from 1996 to the present. IV. Putting It All Together After entering all my assumptions into the WACC formula, my estimate of Nike's cost of capital is 8.9%. WACC = K (1 t) * D/D + E) + K XE/(D+E) = 2.7% X 27.0% + 10.5% x 73.0% = 8.4%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Economics For Financial Markets

Authors: Brian Kettell

1st Edition

0750653841, 978-0750653848