Answered step by step

Verified Expert Solution

Question

1 Approved Answer

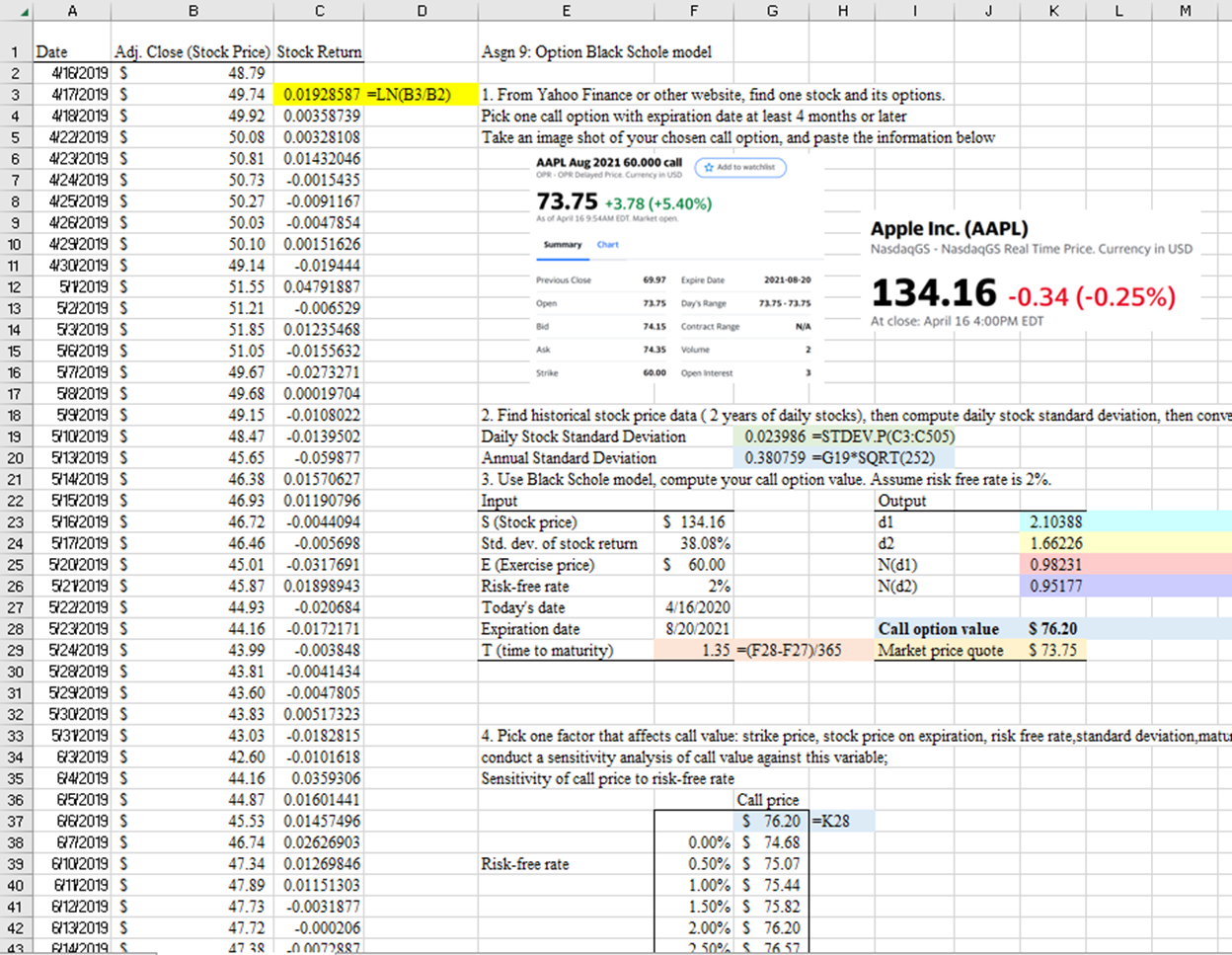

1. From Yahoo Finance or other website, find one stock and its options. Pick one call option with expiration date at least 4 months or

| 1. From Yahoo Finance or other website, find one stock and its options. | |||||||||||||

| Pick one call option with expiration date at least 4 months or later | |||||||||||||

| Take an image shot of your chosen call option, and paste the information below | |||||||||||||

| 2. Find historical stock price data ( 2 years of daily stocks), then compute daily stock standard deviation, then convert it to annual standard deviation | |||||||||||||

| 3. Use Black Schole model, compute your call option value. Assume risk free rate is 2%. | |||||||||||||

| 4. Pick one factor that affects call value: strike price, stock price on expiration, risk free rate,standard deviation,maturity; | |||||||||||||

| conduct a sensitivity analysis of call value against this variable; | |||||||||||||

I attached the example in the pic:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoins Investment

Authors: Paulita Kingrey

1st Edition

979-8353894094