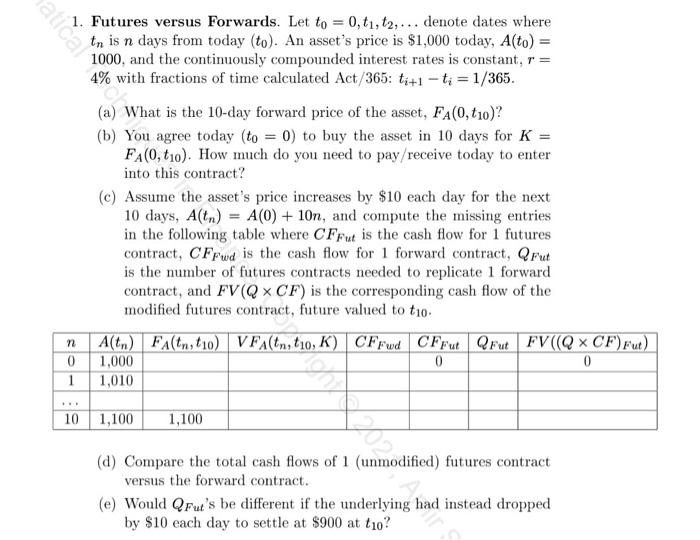

atical 1. Futures versus Forwards. Let to = 0, t1, t2,... denote dates where tn is n days from today (to). An asset's price

atical 1. Futures versus Forwards. Let to = 0, t1, t2,... denote dates where tn is n days from today (to). An asset's price is $1,000 today, A(to) = 1000, and the continuously compounded interest rates is constant, r = 4% with fractions of time calculated Act/365: ti+1-ti = 1/365. (a) What is the 10-day forward price of the asset, FA(0, 10)? (b) You agree today (to = 0) to buy the asset in 10 days for K = FA(0, t10). How much do you need to pay/receive today to enter into this contract? (c) Assume the asset's price increases by $10 each day for the next 10 days, A(tn) A(0) + 10n, and compute the missing entries in the following table where CFFut is the cash flow for 1 futures contract, CFFwd is the cash flow for 1 forward contract, QFut is the number of futures contracts needed to replicate 1 forward contract, and FV (QxCF) is the corresponding cash flow of the modified futures contract, future valued to t10. A(tn) FA(tn,t10) VFA(tn, t10, K) CFFwd CFFut QFut FV ((QCF) Fut) n 0 1,000 1 1,010 10 1,100 1,100 0 0 (d) Compare the total cash flows of 1 (unmodified) futures contract versus the forward contract. (e) Would QFut's be different if the underlying had instead dropped by $10 each day to settle at $900 at tio?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To solve the problem lets address each part systematically a Calculate the 10day forward price ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Navin Kumar

1st Edition

9812876936, 978-9812876935