Answered step by step

Verified Expert Solution

Question

1 Approved Answer

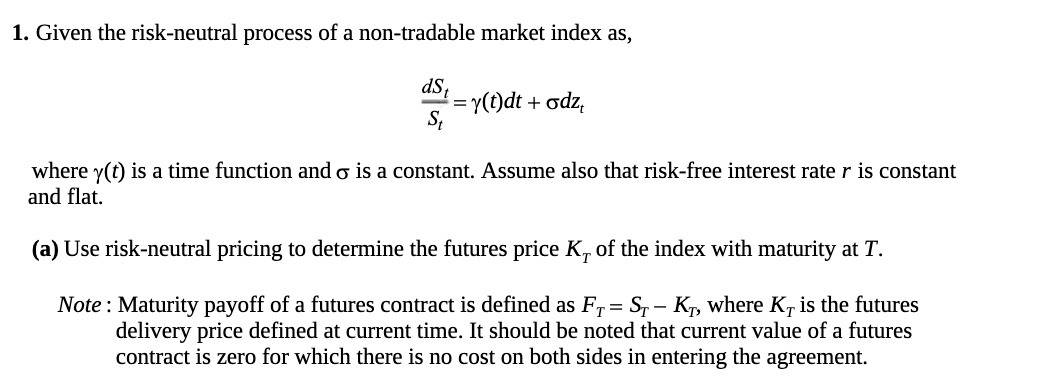

1. Given the risk-neutral process of a non-tradable market index as, ds, St = y(t)dt + odz where y(t) is a time function and

1. Given the risk-neutral process of a non-tradable market index as, ds, St = y(t)dt + odz where y(t) is a time function and is a constant. Assume also that risk-free interest rate r is constant and flat. (a) Use risk-neutral pricing to determine the futures price Kr of the index with maturity at T. Note: Maturity payoff of a futures contract is defined as F = S - K, where K is the futures delivery price defined at current time. It should be noted that current value of a futures contract is zero for which there is no cost on both sides in entering the agreement.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cambridge IGCSE And O Level Additional Mathematics

Authors: Val Hanrahan, Jeanette Powell

1st Edition

1510421645, 978-1510421646