1. Let Ridenote the return on security i in a two-factor model.

(i) Write down the return equation for this two-factor model, defining all

additional notation that you use. [2]

(ii) Describe the three main categories of multifactor models.

2

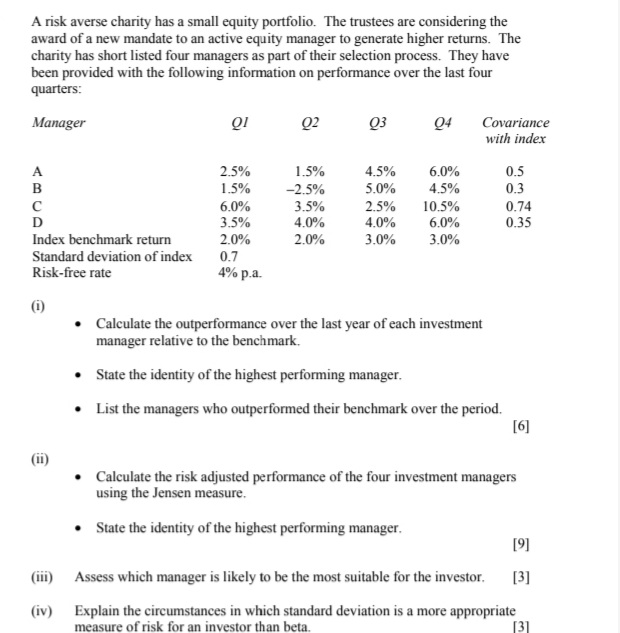

A risk averse charity has a small equity portfolio. The trustees are considering the award of a new mandate to an active equity manager to generate higher returns. The charity has short listed four managers as part of their selection process. They have been provided with the following information on performance over the last four quarters: Manager 02 03 04 Covariance with index 2.5% 1.5% 4.5% 6.0% 0.5 1.5% -2.5% 5.0% 4.5% 0.3 6.0% 3.5% 2.5% 10.5% 0.74 3.5% 4.0% 4.0% 6.0% 0.35 Index benchmark return 2.0% 2.0% 3.0% 3.0% Standard deviation of index 0.7 Risk-free rate 4% p.a. (i) Calculate the outperformance over the last year of each investment manager relative to the benchmark. State the identity of the highest performing manager. . List the managers who outperformed their benchmark over the period. [6] (ii) Calculate the risk adjusted performance of the four investment managers using the Jensen measure. . State the identity of the highest performing manager. [9] (iii) Assess which manager is likely to be the most suitable for the investor. [3] (iv) Explain the circumstances in which standard deviation is a more appropriate measure of risk for an investor than beta. [31(i) Define an increment of a process. [1] The rate of mortality in a certain population at ages over exact age 30 years, h(30+ u), is described by the process: h(30+u) = B(1+y)" u20 where B and y are constants. (ii) Show that the increments of the process log[ h(30 + u)] are stationary. [31A city operates a bicycle rental scheme. Bicycles are stored in racks at locations around the city and may be rented for a fee and ridden from one location and deposited at another, provided there is space in the rack. The rack outside the actuarial profession's headquarters in that city has spaces for four bicycles. The profession would lilte the city to increase the size of the rack. The city has said it will do so if the profession can demonstrate that1 in the long run, the rack is full or empty for more than 35 per cent of the working day. The profession commissions a study to monitor the rack every l minutes during the working day. The study shows that, on average: I there is a probability of [13 that the number, tn. of bicycles in the rack will increase by 1 over a Ill-minute interval {where ll '5 tn *1 4}. I there is a probability of {12 that the number of bicycles in the rack will decrease by l otter a Ill-minute intenral {where I] s m 5 4]. II the probability of more than one increase or decrease per Ill-minute interval can beregardedasil. (i) Give the transition matrix for the number of bicycles in the rack. [2] (ii) Determine whether the city will increase the size of the rack. [15] {iii} Comment on whether an increase in the size of the rack will reduce the proportion of time for which the rack is empty or fall. [2]